Improving Government Support to the SMME Sector

advertisement

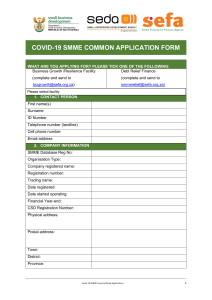

Improving Government Support to the SMME Sector Saul Levin Chief Director Economic Development Department 1 Where does South Africa Stand? South Africa has legislation, a comprehensive policy framework and architecture to support small businesses with financial support, non-finance support (training, advice, mentorship), procurement, international linkages assistance, and technology support. South Africa also has an effective business environment including company regulation, legal system, banking sector, business infrastructure, private sector support services (e.g. accounting, HR, business consulting) etc. Are we making the impact? Questions of Duplication and lack of co-ordination? 2 How do we compare? • Estimate on SMME support (ex procurement) combined National & National agencies: R3 billion; [included is sefa & SEDA combined: +-R715 million allocation p.a. + sefa R2billion for financing] (SA population: 50.5mil) • Northern Ireland: Invest Northern Ireland +-R2billion (pop: 1.7 mil) • UK: Growth Accelerator R2.4billion; Small Business bank R12billion; Business Link R2billion; + mentorship programmes, etc. (pop: 63 million) • USA: SBA R14billion + R160 billion for finance programmes (pop 311 mil) • South Korea: Small and Medium Business Administration R10.5billion + R30 billion for finance programmes (pop: 49.7 mil) 3 Impact • Context of limited resources: • Are we getting the impact for what we spend on Small Businesses? • Advisory Committee established by Minister Patel to make recommendations on the impact of spending on small businesses in South Africa • Deeper understanding of who and how much is being spent 4 What are the challenges? • Gem 2011 report summarises it well: – – – – – – – – – Literacy levels Skills gap Crime (including crime against business) Corruption Health of the workforce Labour market Infrastructure Large firm dominance Low rates of entrepreneurship (given our level of development and GDP) and government run entrepreneurship programmes not making an impact. “South Africa remains one of the more poorly-performing countries with regards to entrepreneurial activity – despite the fact that the country exhibits the factors which are conducive to entrepreneurial ventures, including government policies and programmes aimed at stimulating entrepreneurship.” (GEM 2011) 5 Policy Framework • • • • National Development Plan New Growth Path Industrial Policy Action Plan (IPAP) National Small Business Act 6 National Development Plan • Establishing common ground and a long term vision of where the country needs to go • Identifying objectives and setting actions to achieve those long term objectives • Responds to many of the challenges that inhibit the SME sector: skills, economic infrastructure, costs of doing business, reducing red tape and corruption, labour market reforms, health care, a social safety net, amongst others. “In the short to medium term, most jobs are likely to be created in small, often service-oriented businesses aimed at a market of larger firms and households with income…Public policy can be supportive through lowering barriers to entry, reducing regulatory red tape and providing an entrepreneurial environment for business development. Significantly, these firms are often intensive in mid- and low-skilled employment.” (NDP 2012) 7 New Growth Path (Oct 2010) – summary • The legacy of inequality, access to resources, skills, residential patterns in our country and the challenges that still reflect in our economy: e.g. mining and agriculture shedding jobs; finance not creating jobs • NGP discusses how to respond to these challenges and create the jobs that are so critical for our country. • NGP unpacks the sectors where we see potential to create jobs and where we should concentrate our energies: Infrastructure, Green economy, social economy, productive sectors (agric & agroprocessing; manufacturing; minerals beneficiation); and spatial development (rural and in rest of Africa) • NGP looks at the different drivers that must contribute to job creation; included in these drivers is the importance of state agencies and development finance institutions (and their resources) • The New Growth Path articulates the need for us to achieve a common vision as a society so that all of us – the public sector, the private sector, labour unions and civil society - work together to achieve our goal of creating 5 million jobs by 2020. It is a comprehensive response to the structural crises of poverty, 8 unemployment and inequality in South Africa Industrial Policy Action Plan 3 2012/13 – 2014/15 • IPAP updated to remain relevant and alignment with NGP • Supports the growth of value adding sectors (the move away from commodities) and industrialisation of the economy – employment intensive industrialisation • Interventions and sector support based on data and economic analysis • Alignment with SOEs including IDC for industrial development finance • Supports the alignment of trade and competition policy with industrial policy • Identifies key sectors and value chains for support, including through localisation “IPAP has a particular role to play in dynamising employment and growth in the economy through its focus on value-adding sectors that embody a combination of relatively high employment and growth multipliers” (IPAP3: 2012) 9 Policy framework for support to SMME sector The Integrated Strategy on the Promotion of Entrepreneurship and Small Enterprises identifies three pillars … Strategic Pillar 1: Strategic Pillar 2: Increase supply for financial and non-financial support services Creating demand for small enterprise products and services Collaborative approaches; Streamline resources from the public sector and crowd-in private sector resources New Policy Directives; •Public sector procurement strategy as a lever for increased demand • BBBEE codes of good practice as a lever for increased demand Strategic Pillar 3: Reduce small enterprise regulatory constraints Establish a regulatory impact assessment framework and Business Environment monitoring mechanism Strategy identifies need for clarity, focus, coordination 10 Pillar 1: Finance and Non-Finance Support • Finance: (1) Loans: SEFA, provincial and local agencies, Banks & FIs; (2) 30 day payment campaign; (3) credit information sharing initiative • Non-Finance: Training, capacity building, INCUBATORS & business premises, information, entrepreneurship support • GAPS: • Not enough resources and funding • Co-ordination across government • Poor focus by size / sector / stage – creates bottlenecks & who gets serviced • Need for innovative finance products 11 Pillar 2: Demand for goods and services • Opportunities: government procurement, local content, private sector & value chains (national government alone procures an estimated R3.3 billion from SMMEs) • Gap: – Missed opportunities with set-asides / 10 product requirement not implemented 12 Pillar 3: Regulatory Constraints • Constraints at both National and Local level • National: Costs of compliance & time: RIA requirements and review of legislation • Local: By-laws: work done by dti & SALGA, individual municipalities • Gaps: – Ongoing bottleneck that holds back businesses and entrepreneurship – Regulatory constraints not systematically addressed 13 Recommendations from the dti SMME Review • • • • • • • • Better co-ordination across government Data gathering Make it easier to access support from government More business incubators – co-ordinated, appropriately run and properly resourced with sector focus Specific support to the manufacturing sector A unified national mentorship programme Improve the workings of the small claims court Stimulate the ‘angel investor’ market and other venture capital type investors 14 Recommendations, cont • Establish a national credit register • Improve SMME finance agencies and direct lending • Improve government payment (30 days) and encourage private sector to do the same • More information on the availability of finance for SMMEs in SA • Improved demand for SME goods and services • Red tape reduction 15 A period of consolidation • At national: Merger of Khula and samaf to create SEFA • At provincial level: Limpopo, North West, Western Cape: consolidation of provincial agencies (or into national) underway • Others … 16 Merged small business financing entity SEFA • President announced work on merger of SMME lenders in Feb 2011 SONA and decision taken to merge Khula, samaf and the IDC small business financing into a single entity • Entity established and launched on 23 April 2012: the Small Enterprise Finance Agency (SEFA) • Falls under the IDC and is recapitalised – R2billion over 3 years • Focus is on direct lending but will continue with wholesale loans to Financial Intermediaries and with Credit Guarantees. • Establishing national presence through regional, branch and satellite offices • SEFA Helpline 086 00 54852 or helpline@sefa.org.za 17 17 Conclusion • Policies are robust • Strong, well managed and properly resourced institutions (finance and non-finance) • Interventions that are focused (incubation; a gazelle’s strategy?) • Link into supply chains and procurement (public and private sector) • 30 day payment is critical 18