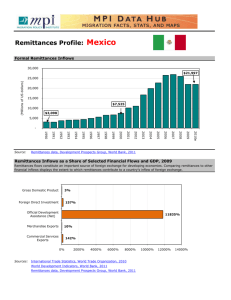

The role of loans and remittances in

Consumption and Investment

decisions in Urban Ethiopia

Abbi Kedir

University of Leicester, UK

&

Gamal Ibrahim, UNECA

October, 2011

Outline of the talk

•

•

•

•

•

•

•

Purpose

Motivation

Related literature

Theory

Data

Methodolgy

Results and discussion

Purpose

• Do remittances and loans lead to higher/lower

household asset accumulation, food and nonfood consumption?

• Do remittances and loans increase the

likelihood

of

self-employment

or

entrepreneurship?

Motivation I

• Finance and growth (macro level ‘link broken’)

• Informal financial transfers are fundamental

anchors of welfare and employment

• Most micro level literature focuses on what

determines access to credit and the motives

for private transfers such remittances (Alvi and

Dender, 2009).

• Often credit and remittances are studied

separately (Christensen and Pan, 2010).

Motivation II

• There is a dearth of evidence on how access to

credit and remittances affect household

investment and consumption decisions in SSA

( an attempt to trace the mechanism)

• Labour market – one mechanism to link

growth and poverty (Kedir et al 2011).

• Provide relevant policy recommendations

Literature(only micro) I

• Alvi and Dender, 2009 : what factors significantly

affect household loans and private transfers in

Ethiopia.

• Liverpool and Winter-Nelson (2010) no

relationship b/n participation in microfinance

programs and the use of technologies or

consumption growth among the poorest

households (Ethiopia).

• For other households, microfinance has positive

effects on both consumption and asset growth as

well as on the use of improved technology.

Literature II

• Adams (1998)- effect of remittances on asset

accumulation in Pakistan. Household are

impatient (high discount rate) and do not

sacrifice present consumption for the sake of

asset accumulation.

Theory I

• Remittance flows over long distances (severe

asymmetric information problem).

• Credit need to be repaid and often provided

by informal lenders (less serious asymmetric

information problem)

• Propensity to consume(invest) in the former

(latter) is stronger than to invest(consume).

Theory II

• We test the following propositions:

C / R 0; E / R 0; C / L or 0;

&

A / R 0 ; E / L 0

Data and Econometric framework

• Panel data from urban Ethi0pia (1994,1995,

1997, 2000, 2004 on 1500 households)

• Fixed effects of consumption and asset

accumulation equations (Hausman test)

• Random effect Probit of self-employment

(stability of quadrature points)

Key Results

• Remittances are positively associated with

food consumption, non-food consumption

and asset (unproductive) accumulation.

• Remittances are negatively associated with

self-employment and entrepreneurship while

the opposite is true for credit

Policy I

• The need for credit access to households to

create employment is obvious.

• Self-employment in the data is characterised

by low-tech and low return small/micro firm

activities.

• Hence for meaningful development volume of

capital provided must be much larger than

what households can get via informal

networks

Policy II

• Small/micro firms are unlikely to grow large.

They simply provide subsistence for millions of

unskilled workers.

• About 800,000 urban informal sector firms

(mfg, trade, services) with 1 million people

employ.ed (Soderbom, 2010)

Future work and econometric issues

• Distinguish between domestic and external

remittances

• Remittances and labour supply to explore why

remittances lead to lower self-employment.

• Endogeneity (IV) and parameter heterogeniety

(quantile regression).

0

0