Session 4: Talking Points, Cont`d Economic Systems 3.

advertisement

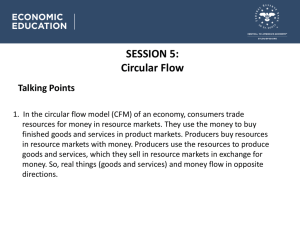

SESSION 4: ECONOMIC SYSTEMS, ECONOMIC INSTITUTIONS & INCENTIVES, AND MONEY & EXCHANGES Talking Points Economic Systems 1. Following from points discussed in earlier sessions, the next step in addressing society’s fundamental economic problem is to identify the criteria to be used to evaluate alternatives (Step 3 of the PACED model). Criteria are the important things to consider when making a choice. 2. While there are several broad social goals that may be used to evaluate society’s alternatives, economics focuses primarily on efficiency. Session 4: Talking Points, Cont’d Economic Systems 3. Efficiency in general means “getting the most out of something” (for example, a fuel-efficient car is one that gets the best mileage from a gallon of gas). 4. Productive efficiency means getting the most output from a society’s scarce resources (all points along the PPC are productively efficient). 5. Allocative efficiency means getting the most value from a society’s scarce resources (only one point along the PPC is allocatively efficient, and selecting that point depends on what society wants or values). 6. Choosing a point along the PPC can be done in markets or by central planners. Session 4: Talking Points, Cont’d Economic Systems 7. Economic systems differ in three significant ways: a. who owns and controls the resources, b. who makes the decisions, and c. what the underlying motivation is. 8. Central planners generally do not have the information necessary to find the allocatively efficient combination of goods and services. Session 4: Talking Points, Cont’d Economic Institutions & Incentives 1. In a command (planned) economy, it is very difficult to match output specifications to the desires of consumers because producers are reacting to government incentives rather than the wishes of their consumers. 2. In a command economy, adjustments to “the plan” require direct intervention by the central authority and can be very difficult. 3. In a traditional economy, goods and services are produced according to the customs of society. 4. In market economies, producers respond to the desires of their consumers in order to earn profits. In a market economy, adjustments occur automatically through price changes, which change incentives. Session 4: Talking Points, Cont’d Money & Exchange 1. The fundamental trade that occurs in a market economy consists of people trading the productive resources they own for the goods and services they want. 2. Because direct exchange is difficult (i.e., Cheerios for an economics lecture), money was developed to facilitate trade. 3. In the circular flow model (CFM) of an economy, consumers trade resources for money in resource markets. They use the money to buy produced goods and services in product markets. Producers buy resources in resource markets with money. Producers use the resources to produce goods and services, which they sell in resource markets in exchange for money. So, real things (goods and services) and money flow in opposite directions. Session 4: Talking Points, Cont’d Money & Exchange 4. Consumers are sellers in resource markets and buyers in product markets, while producers are buyers in resource markets and sellers in product markets. 5. Consumers and producers have different names for the same flows in the CFM: a. Consumers sell resources; producers buy inputs. b. Consumers are paid income; producers incur costs. c. Consumers buy goods and services; producers sell their outputs. d. Consumers make expenditures; producers receive revenue. Visual 4A: Broad Social Goals/Criteria Efficiency: Getting the most out of something Productive Efficiency Getting the most output (goods and services) from a given amount of resources (i.e., producing in the least-costly way possible—not wasting resources). Allocative Efficiency Getting the most value (satisfaction) from a given amount of resources (i.e., producing the mix of goods and services thatsociety most highly values). Visual 4A: Broad Social Goals/Criteria, Cont’d Equity: Making sure that things are “fair” Looking through a “veil of ignorance” (i.e., not knowing if people are rich or poor, black or white, young or old, an employer or employee), individuals are to be treated equally in terms of income/wealth distribution, opportunity, and/or economic outcomes. Economic Freedom: Allowing individual choice Freedom for individuals to choose where and when to work, open or close a business, spend or save their income, invest in what they want, and make other economic decisions. Economic Security: Protection from economic risks Providing individuals with income or a job if they are unemployed and/or disabled, health care if they are sick, food if they are hungry, energy if they are cold, and so on. Lesson 4.1, Visual 1: Team Earnings Visual 4B: Goods and Services Markets