Reconcilation

advertisement

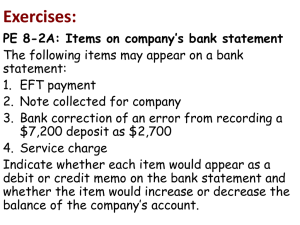

N9G “TOOLBOX” What is the N9G Tool Box? • The N9G tool box provides the field with helpful information on a wide range of subjects. • The tool box provides information to CNIC Regions & Installations; keeping them “audit-ready” at all times. • We have provided each of you with a tool box, just make sure as we provide you a tool monthly, you keep it in your tool box! Topics that will be filling your Tool Box Monthly • • • • • • • Cost of Goods Sold Cash & Cash Handling November December Managers Financial Review January NAF Personnel February Contracts April Reconciliation July Assets Inventory August Reconciliation Account reconciliation is important not just for individuals and households, but also for businesses. MWR, NGIS, CMWR, & NFC Business Offices must reconcile their accounts to check for fraud and to prevent balance sheet errors. Without accurate financial information, REGCOM, Commanding Officers and Managers cannot make well-informed decisions. Reconciliation Balance sheet accounts are used to record assets, liabilities and equity. Balance Sheet Accounts Assets Liabilities Equity The account Balances roll forward from fiscal year to year Income Statement Accounts Revenue accounts Expense Accounts Unlike Income Statement accounts (revenue and expense accounts), Errors made in balance sheet accounts will remain until corrected Reconciliation Balance sheet account reconciliations are a continuous explanation of activities that have occurred in an account. An account is reconciled when all differences have been identified (regardless of age), proper accounting treatment ascertained and corrective action is listed in the reconciliation including when corrections will take place, usually in the following month. Reconciliation Items must not be allowed to remain in a balance sheet account indefinitely In general, one month would be considered an appropriate length of time for an accounts receivable, short term liability or a clearing account transaction. Prepaid amounts and deferred revenue amounts must be cleared to the appropriate general ledger account in the period in which the revenue or expenditure belongs. Reconciling items identified as errors must be cleared as soon as possible, generally, this is expected to be in the month following detection Reconciliation Additional back-up may be required by Financial Reporting or internal and external auditors. • Departments must ensure all backup such as purchase orders, receipts, properly executed contracts or other documentation is retained and readily available when requested. • Account reconciliation is an underappreciated yet critical control to help ensure an organization's financial integrity. • Weaknesses and inefficiencies in the reconciliation process often lead to mistakes on the balance sheet and overall inaccuracies in the financial close. Reconciliation Since the enactment of Sarbanes Oxley (SOX) in 2002 and other rules and regulations that have followed, ensuring the accuracy of account reconciliations has become increasingly important. • In the past, if an external auditor found a material error during review of a company's financial statements, it could still be corrected by the company with an adjusting entry. • In most cases, the controller wouldn't have to issue a restatement, nor would the auditor have to report the error. Reconciliation • With the advent of SOX, the call for compliance has risen to another level. • If the auditor finds a material error, the company may be required to disclose a failure of controls. • If the auditor finds a misstatement while reviewing the quarterly or annual SEC reports that the company cannot prove it would have found on its own, then the error is determined to be a material misstatement and a material weakness that could also require disclosure. Reconciliation • An efficient, accurate, and timely financial close cycle (beginning with the account reconciliation process) can create a foundation for: evaluating business performance supporting organizational decisions satisfying external reporting requirements. • Automation of the account reconciliation process is a critical step on the road to achieving "balance sheet integrity" - and ultimately, a timely and efficient financial close. Software alone will not ensure account reconciliations are accurate Reconciliation Following this best practices list will send you on your way to error-free account reconciliations and a more efficient financial close! Account reconciliations should be complete - no account left behind! Ensure all appropriate accounts are being reconciled Ensure that there is an overall reconciliation policy and that it is adhered to throughout the business office Ensure that each reconciliation includes a title, description of the account, and procedures and/or instructions on how to complete the reconciliation (applicable contacts, reports to run or obtain, etc.) Business Office Managers will be required to create and train accounting personnel on the proper reconciliation processes Documentation supporting the account balance should be included with the reconciliation. Documentation of a reconciliation allows for required auditability of all financial records. Reconciliation – Best Practice Account reconciliations should be accurate The individual preparing and reviewing the account should have a basic understanding of what the account is used for and what should be used to support the balance. For example, cash accounts will most often need the general ledger and a bank statement or appropriate DARs to validate funds received, in order to perform the reconciliation. Ensure that the correct, most updated balances are being reconciled. Ensure that the reconciliation actually supports the balance and is not just a repeat of the general ledger or a roll-forward of the balance. You actually have to validate each entry, not just assume it is accurate. Backup documentation is required to ensure accuracy. Watch for accounts that have unusual balances (such as an accrual with a debit balance or a receivable account with a credit balance). Reconciliation – Best Practice Account reconciliations should be completed and reviewed in a timely manner Create due dates for the reconciliations Have a mechanism to track the status of each reconciliation Make the high-risk account reconciliations due early in the close cycle to identify any potential problems Review the unidentified differences and post the necessary adjustments while the accounting period is still open Reconciliation- Best Practice Account reconciliations should support the appropriate accounting principles Account reconciliations should follow the accounting principles established by CNIC Finance Ensure the reconciliations are: objective that they identify material unidentified differences that they are consistent that the transactions behind the general ledger balance followed the convention of conservatism. Reconciliation The account reconciliation process should be constantly reviewed and improved Review the account reconciliation policy to ensure it accurately reflects FFR Policies and procedures. Review the overall process routinely to identify improvements that help drive quality and timeliness. Review the reconciliation procedures and/or instructions to ensure they answer: What? When? Who? Why? How Much? Good tools and processes provide a framework for ensuring quality, accuracy, and completeness. They provide a means to track assignments, due dates, and work completion. A robust, automated account reconciliation process will focus the right people on the right activities and give management real-time information around the close process. Reconciliation GL Account How to Reconcile a General Ledger Account Good accounting controls means knowing what's in your balance sheet. If you don't reconcile your accounts on a regular basis you can't be sure if your financial statements are correct. Follow these steps to clear and correct financial reporting. Understand the accounting policy for the account you are reconciling. The first step in reconciling your general ledger account is to know what should be in it. You can't verify that the balance is correct unless you know the rules. Read your company accounting policy manual and clarify any issues with your supervisor or manager. Gather supporting documents. These will differ depending on the type of account you are reconciling. They could be copies of invoices, agreements or contracts, statements from outside parties (like bank statements) or copies of supporting reports from other systems - like accounts receivable. Reconciliation How to Reconcile a General Ledger Account Ask yourself the investigative questions about the items in the account - what are they? when were they created? how do they relate to accounting policies? why are they in this account balance? Document your explanations and conclusions clearly and completely. Document for others - not yourself The purpose of the reconciliation is to demonstrate to others that the account balance is correct. Make sure your explanations don't include too much jargon and that they are complete. Reconciliation A listing that just shows the activity in and out of the account is not really a reconciliation The purpose of the reconciliation is to substantiate that the balance is correct! The listing of all activity just shows what the balance is! Reconciliation BLUF – The Balance sheet is required to be an accurate reflection of the financial condition of each MWR, NGIS, CMWR and NFC. No ONE is perfect. The reconciliation process will assist in identifying issues, mistakes and in some cases potential fraud, waste and abuse. It is our responsibility to safeguard the sailor’s money and the reconciliation process is just one vital control in ensuring those safeguards are sufficient.