Bank Broker-Dealers / What You Should Know

advertisement

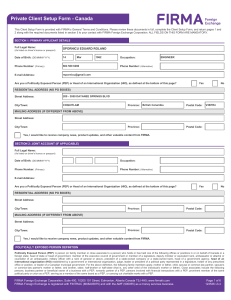

Bank Broker-Dealers / What You Should Know Marilyn Smith Head U.S. Risk Policy & Governance BMO Financial Group/ Harris Bank April 18 2011 Disclaimer ANY PART OF THIS PRESENTATION OR DISCUSSION REPRESENTS VIEWS AND OPINIONS THAT ARE SOLEY MINE AND NOT OF MY COMPANY OR ANY COMPANY YOU MAY PRESUME THAT I REPRESENT. THESE VIEWS ARE SUBJECT TO CHANGE WITHOUT NOTICE. FIRMA 25th Annual Risk Management Conference – April 18 • 2011 1 Bank Broker-Dealers/What You Should Know What is a Broker-Dealer – Quick Review General standards for Broker-Dealers General standards for Bank-Owned BrokerDealers Dodd-Frank Implications Broker Dealers as Fiduciaries FIRMA 25th Annual Risk Management Conference – April 18 • 2011 2 Common Functions of Broker-Dealers Order execution Transaction clearing Custody Research Recommendations Valuations Underwriting Wealth Management FIRMA 25th Annual Risk Management Conference – April 18 • 2011 3 Types of Brokers Principal Buys and sells to their clients’ from own inventory Agent Buys or sells their clients market items Wholesalers/ Distributors Distributes own proprietary products to other firms (no retail clients) Introducing Does not hold their clients’ funds or securities Clearing Receives orders from introducing broker to execute and settle orders; holds funds and securities FIRMA 25th Annual Risk Management Conference – April 18 • 2011 4 Some General Standards For Broker-Dealers Customers Retail/Individuals Institutions Products/Services Trade execution Recommendations Research Custody Securities Lending Compensation Commissions Fee-Based Registration SEC FINRA MSRB, if applicable Or States Disclosures Form BD Advertisements/ marketing materials Primary Regulator SEC FINRA, SRO FIRMA 25th Annual Risk Management Conference – April 18 • 2011 5 Some General Standards For Bank-Owned B-Ds Customers Retail/Individuals Institutions Products/Services Trade execution Recommendations Research Custody Securities Lending Compensation Commissions Fee-Based Registration SEC FINRA MSRB, if applicable Or States Disclosures Form BD Advertisements/marketing materials Primary Regulator SEC FINRA , SRO FIRMA 25th Annual Risk Management Conference – April 18 • 2011 6 Advantages to Bank-Owned BDs Provides customers : ‘One Stop Shopping’ for Financial Services Retention of certain securities positions Access other products and services Different levels of discretion over their assets Provides the BD: Access to less costly funding More sales opportunity Retention of assets FIRMA 25th Annual Risk Management Conference – April 18 • 2011 7 Additional Standards For Bank-Owned B-Ds Heightened Potential Conflicts of Interest Customers Retail/Individuals Institutions Information barriers must be maintained between and among entities Products/Services Trade execution Recommendations Research Custody Securities Lending Services provided by/for affiliates should not receive preferential treatment; apply robust due-diligence to document armslength handling; may need a horizontal view of rationale for differences Compensation Commissions Fee-Based Referral Fees No tying Registrations SEC FINRA MSRB, if applicable Or States Dual employees-roles and responsibilities should be clear and accurate recordkeeping Avoid the danger of ‘parking’ Disclosures Form BD Advertisements May need to be more prominent – more explicit language on Form BD and in marketing materials to clients Primary Regulator FINRA BHC coverage by Fed and expectation of adequate oversight and due-diligence FIRMA 25th Annual Risk Management Conference – April 18 • 2011 8 Dodd-Frank Act , 7/21/2011 Applies to financial institutions Defines ‘financial institution” a depository institution or depository institution holding company, a broker-dealer registered under section 15 of the ‘34 Act a credit union, an investment adviser under the ’40 Act the mortgage agencies (FNMA, FHLM), or any other financial institution that the appropriate Federal regulators, jointly, by rule, determine should be treated as a covered financial institution for these purposes. And for purposes of defining “large” or “significant” it includes the “consolidated” holdings of a financial holding company FIRMA 25th Annual Risk Management Conference – April 18 • 2011 9 Dodd-Frank Act Implications for Broker-Dealers 7/21/2010 Accredited Investor Compensation Derivatives/Swaps Fiduciary Standards [913] Transactions with Affiliates FIRMA 25th Annual Risk Management Conference – April 18 • 2011 10 Definition of Accredited Investor [413] Definition of Accredited Investor changes to EXCLUDE the value of the primary residence: (i) individual net worth (or joint net worth with his or her spouse) in excess of $1 million or (ii) annual income in excess of $200,000 (or joint annual income with his or her spouse in excess of $300,000) for the past two years and (iii) the reasonable expectation of meeting the same level of income in the current year. Defines “Qualified Purchasers” for participation in certain products or transactions - private placements ( Reg D) - private equity funds - hedge funds FIRMA 25th Annual Risk Management Conference – April 18 • 2011 11 Compensation [956] For publicly traded companies Executive Compensation Say-on-Pay shareholder approval clawback policies following a restatement (3 yr period) Elimination of broker-dealer voting of proxies re exec comp For financial institutions with assets > $1Bil Financial Institution Prohibits ‘incentive-based’ compensation, fees, or benefits that encourages inappropriate risk or that could lead to losses Directs Bank regulators to prohibit it ,and Allows Bank regulators to impose higher capital charges For financial institutions > $50Bil Deferrals of compensation of executives Policy and procedure and disclosures requirements as well FIRMA 25th Annual Risk Management Conference – April 18 • 2011 12 Derivatives/Swaps [Title VII] Definition of a swap dealer and major participant Requires registration by swap dealers and major swap participants with CFTC Defines a major participant as anyone who is not a swap dealer and maintains substantial positions excluding hedging positions for commercial or employee benefit plan risk Defines “significant position” as whatever the CFTC determines to be effective Requires introducing broker to implement conflict-of-interest procedures to ensure independence between research and analysis and trading and clearing. Establish robust procedures for day to day management Allows CFTC to impose limits on amount of positions held of any one person FIRMA 25th Annual Risk Management Conference – April 18 • 2011 13 Affiliate Transaction Restrictions [Title VI] Title VI (amends 23A & 23B) Applies to Banks… eliminates the exception for affiliated transactions in credit exposed derivatives, repos, reverse repos, securities lending and borrowing transactions, and additional categories of ‘covered’ transactions considered to be extensions of credit factored into the Bank’s legal lending limits prohibits use as collateral of low-quality issues of an affiliate FIRMA 25th Annual Risk Management Conference – April 18 • 2011 14 Fiduciary Standard for Broker-Dealers Section 913 SEC study concluded January 2011 regarding proposal … Recommends that the Commission “promulgate a rule that the standard of conduct for all brokers, dealers, and investment advisers, when providing personalized investment advice about securities to retail customers (and such other customers as the Commission may by rule provide), shall be to act in the best interest of the customer without regard to the financial or other interest of the broker, dealer, or investment adviser providing the advice”. aka “…the uniform fiduciary standard FIRMA 25th Annual Risk Management Conference – April 18 • 2011 15 Fiduciary “Standards” For Broker-Dealers Registered Broker-Dealer Registered Investment Adviser Suitability Rules Based Investment Objectives at time of a/c opening at time of transaction Standards Based Investment Objectives at time of a/c opening at time of transaction after the fact Products/Services IPOs Private Placements Hedge Funds Penny stocks Options Structured Products Sophisticated Investor Broker selection Trade Allocation Recommendations Research Wealth Management Custody Prudent Investor Rule full range of services Compensation Commissions Fee-Based Products sold AUM Advisory Fee Performance, limited, explicit permission Must be fair & reasonable and if higher than other advisers, must disclose this Registration SEC FINRA States with clients MSRB, if applicable SEC >15 clients and $25mil AUM* States, where place of business, some >6 clients Disclosures Form BD Advertisements Form ADV Reports/Materials Full Transparency including omissions * $100mil a/o 7/1/2011 FIRMA 25th Annual Risk Management Conference – April 18 • 2011 16 Recommendations for Approaching Implementation Make sure your business assessments/maps are up-to-date Affiliations Dual employees Establish internal ‘rules’ for your business/activity/product scenarios What can happen How will we know when it happens What can we do when it does happen Document, document, document “standards” are presumptive; remember that they will be applied after the fact FIRMA 25th Annual Risk Management Conference – April 18 • 2011 17 Samples Sample Brokerage Applications with Investment Objectives Form BD FIRMA 25th Annual Risk Management Conference – April 18 • 2011 18 QUESTIONS FIRMA 25th Annual Risk Management Conference – April 18 • 2011 19