Chapter 2: The Economic Problem: Scarcity and

advertisement

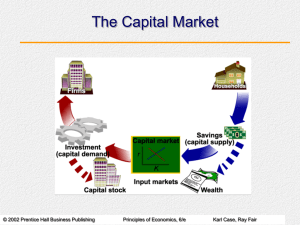

C H A P T E R 2: The Economic Problem: Scarcity and Choice Unit I: Basic Economic Concepts Topic C: The Market System and the Circular Flow © 2004 Prentice Hall Business Publishing Principles of Economics, 7/e Karl Case, Ray Fair 1 of 40 C H A P T E R 2: The Economic Problem: Scarcity and Choice Economic Systems • The economic problem: Given scarce resources, how, exactly, do large, complex societies go about answering the three basic economic questions? © 2004 Prentice Hall Business Publishing Principles of Economics, 7/e Karl Case, Ray Fair 2 of 40 C H A P T E R 2: The Economic Problem: Scarcity and Choice Economic Systems • Economic systems are the basic arrangements made by societies to solve the economic problem. They include: • Command economies • Laissez-faire economies • Mixed systems © 2004 Prentice Hall Business Publishing Principles of Economics, 7/e Karl Case, Ray Fair 3 of 40 C H A P T E R 2: The Economic Problem: Scarcity and Choice Economic Systems • In a command economy, a central government either directly or indirectly sets output targets, incomes, and prices. • In a laissez-faire economy, individuals and firms pursue their own selfinterests without any central direction or regulation. © 2004 Prentice Hall Business Publishing Principles of Economics, 7/e Karl Case, Ray Fair 4 of 40 C H A P T E R 2: The Economic Problem: Scarcity and Choice Economic Systems • The central institution of a laissezfaire economy is the free-market system. • A market is the institution through which buyers and sellers interact and engage in exchange. © 2004 Prentice Hall Business Publishing Principles of Economics, 7/e Karl Case, Ray Fair 5 of 40 C H A P T E R 2: The Economic Problem: Scarcity and Choice Economic Systems • Consumer sovereignty is the idea that consumers ultimately dictate what will be produced (or not produced) by choosing what to purchase (and what not to purchase). © 2004 Prentice Hall Business Publishing Principles of Economics, 7/e Karl Case, Ray Fair 6 of 40 C H A P T E R 2: The Economic Problem: Scarcity and Choice Economic Systems • Free enterprise: under a free market system, individual producers must figure out how to plan, organize, and coordinate the production of products and services. © 2004 Prentice Hall Business Publishing Principles of Economics, 7/e Karl Case, Ray Fair 7 of 40 C H A P T E R 2: The Economic Problem: Scarcity and Choice Economic Systems • In a laissez-faire economy, the distribution of output is also determined in a decentralized way. The amount that any one household gets depends on its income and wealth. © 2004 Prentice Hall Business Publishing Principles of Economics, 7/e Karl Case, Ray Fair 8 of 40 C H A P T E R 2: The Economic Problem: Scarcity and Choice Economic Systems • The basic coordinating mechanism in a free market system is price. Price is the amount that a product sells for per unit. It reflects what society is willing to pay. © 2004 Prentice Hall Business Publishing Principles of Economics, 7/e Karl Case, Ray Fair 9 of 40 C H A P T E R 2: The Economic Problem: Scarcity and Choice Mixed Systems, Markets, and Governments Since markets are not perfect, governments intervene and often play a major role in the economy. Some of the goals of government are to: • Minimize market inefficiencies • Provide public goods • Redistribute income • Stabilize the macroeconomy: • Promote low levels of unemployment • Promote low levels of inflation © 2004 Prentice Hall Business Publishing Principles of Economics, 7/e Karl Case, Ray Fair 10 of 40 C H A P T E R 2: The Economic Problem: Scarcity and Choice Let’s recap Characteristics of a market economy: private property; freedom of enterprise and choice; self-interest; competition; market and prices; technology and capital goods; specialization—division of labor and geographic specialization; use of money; active but limit government. © 2004 Prentice Hall Business Publishing Principles of Economics, 7/e Karl Case, Ray Fair 11 of 40 C H A P T E R 2: The Economic Problem: Scarcity and Choice Adam Smith What is the invisible hand and how do I know it’s there? © 2004 Prentice Hall Business Publishing Principles of Economics, 7/e Karl Case, Ray Fair 12 of 40 C H A P T E R 2: The Economic Problem: Scarcity and Choice Circular Flow Model © 2004 Prentice Hall Business Publishing Principles of Economics, 7/e Karl Case, Ray Fair 13 of 40 C H A P T E R 2: The Economic Problem: Scarcity and Choice Firms and Households: The Basic Decision-Making Units • A firm is an organization that transforms resources (inputs) into products (outputs). Firms are the primary producing units in a market economy. • An entrepreneur is a person who organizes, manages, and assumes the risks of a firm, taking a new idea or a new product and turning it into a successful business. • Households are the consuming units in an economy. © 2004 Prentice Hall Business Publishing Principles of Economics, 7/e Karl Case, Ray Fair 14 of 40 C H A P T E R 2: The Economic Problem: Scarcity and Choice Input Markets and Output Markets: The Circular Flow • The circular flow of economic activity shows how firms and households interact in input and output markets. © 2004 Prentice Hall Business Publishing Principles of Economics, 7/e Karl Case, Ray Fair 15 of 40 C H A P T E R 2: The Economic Problem: Scarcity and Choice Input Markets and Output Markets: The Circular Flow • Product or output markets are the markets in which goods and services are exchanged. • Input markets are the markets in which resources—labor, capital, and land—used to produce products, are exchanged. © 2004 Prentice Hall Business Publishing Principles of Economics, 7/e Karl Case, Ray Fair 16 of 40 C H A P T E R 2: The Economic Problem: Scarcity and Choice Input Markets and Output Markets: The Circular Flow © 2004 Prentice Hall Business Publishing • Goods and services flow clockwise. Firms provide goods and services; households supply labor services. • Payments (usually money) flow in the opposite direction (counterclockwise) as the flow of labor services, goods, and services. Principles of Economics, 7/e Karl Case, Ray Fair 17 of 40 C H A P T E R 2: The Economic Problem: Scarcity and Choice Input Markets and Output Markets: The Circular Flow • Input or factor markets are the markets in which the resources used to produce products are exchanged. They include: • The labor market, in which households supply work for wages to firms that demand labor. © 2004 Prentice Hall Business Publishing Principles of Economics, 7/e Karl Case, Ray Fair 18 of 40 C H A P T E R 2: The Economic Problem: Scarcity and Choice Input Markets and Output Markets: The Circular Flow And. . . • The capital market, in which households supply their savings, for interest or for claims to future profits, to firms that demand funds to buy capital goods. • The land market, in which households supply land or other real property in exchange for rent. © 2004 Prentice Hall Business Publishing Principles of Economics, 7/e Karl Case, Ray Fair 19 of 40 C H A P T E R 2: The Economic Problem: Scarcity and Choice Input Markets and Output Markets: The Circular Flow • Inputs into the production process are also called factors of production. © 2004 Prentice Hall Business Publishing Principles of Economics, 7/e Karl Case, Ray Fair 20 of 40