Ernst & Young

Infrastructure Advisors, LLC

PPPs and Inland Rivers, Ports and

Terminals

30 April 2014

Growing market for public private partnerships

►

►

►

►

US examples include:

►

Port of Miami Tunnel (closed)

►

I-595 Corridor Improvements and Express Lanes (closed)

►

RTD Denver P3 Eagle (closed)

►

Long Beach Courthouse (closed)

►

Goethals Bridge (closed)

►

Port of Baltimore Seagirt Marine Terminal (closed)

►

Numerous other toll projects and facilities

Considerable interest for transit as well as social infrastructure

(courthouses, schools, etc.)

Being applied to toll facilities with toll revenues accruing to the public

owner – e.g., I-595, Goethals, I-4

Many closed examples internationally (Canada, UK, etc.)

Page 2

PPP Example- Seagirt Marine Terminal

►

Public-Private Partnership between Maryland Port

Administration and Ports America Chesapeake

►

50-year concession signed in 2010

►

About $105 million of immediate improvements required

under concession, plus future maintenance

►

Shipping companies pay concessionaire for use of

terminal

Page 3

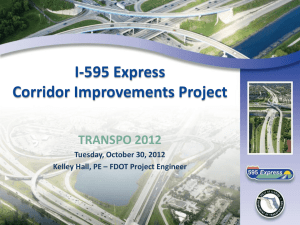

PPP Example- Port of Miami Tunnel

►

Public-Private Partnership between Florida Department of

Transportation (FDOT) and Miami Access Tunnel (MAT)

►

35-year concession agreement signed 2009

►

MAT bears construction risk

►

FDOT pays milestone payments to MAT during

construction, then availability payments

►

FDOT collects any tolls on tunnel

Page 4

Presentation title

Methods of project delivery

►

Design-Bid-Build (DBB)

►

Design-Build (DB)

►

Design-Build-Finance (DBF)

►

Design-Build-Operate-Maintain (DBOM)

►

Design-Build-Finance-Operate-Maintain (DBFOM)

Page 5

Design-Bid-Build

(DBB)

Project roles – Conventional project delivery

Page 6

Government

Designer

Tax-exempt

public debt

Operator or government

Contractor(s)

Public-Private

Partnership

(DBFOM)

Design-Build (DB)

Project roles – Alternative project delivery

Page 7

Government

DB contractor

Tax-exempt

public debt

Operator or government

Government

Equity investors

Concessionaire

DB contractor

Operator

Lenders

PPP – More than just financing

►

►

►

►

►

Who bears the risks of construction overruns, delays, operational

underperformance, revenue shortfalls, higher than expected lifecycle

costs, and/or unexpected or more frequent major maintenance?

A PPP can permit the public sector to adjust the timing of its

payments.

A project must be sufficiently defined and sufficiently large to attract

bidders.

Public trust is compromised if the performance and cost assumptions

used to justify spending and dedicated taxes or other commitments

are not achieved.

Whether or not a PPP is ultimately warranted, considering a full range

of delivery options fosters communication among disciplines and can

lead to better outcomes and understanding of risks.

Page 8

DBB

Comparing public expenditure profiles

35

Year of expenditure

(real dollars)

DBFOM

$250

$200

Availability Payments

$150

$100

$50

35

$0

1

2

3

4

5

6

7

8

9

10

(Note: these are very general approximations and conventional chart assumes major maintenance expenditures are smoothed as

contributions to reserves)

Page 9

Understanding equity

►

►

►

Cannot borrow 100% of an expected revenue stream

Need a cushion or “coverage” – risk capital that absorbs financial

impact of poor performance

The coverage revenue is equity’s return – or risk

Simplified example for illustration purposes: 1.2x debt service coverage

Equity Return

Expenses

Debt Service

Revenues

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30

Years

Page 10

Understanding debt

►

The public sector does not face the same credit risk in a

PPP that equity and lenders face.

►

Low-cost debt can facilitate a PPP.

►

►

►

Page 11

Conduit issuers, tax exempt debt and private activity bonds all have

roles.

TIFIA is an important lender for US transportation PPPs, but has

limitations on repayment from federal funds.

WRDA and WIFIA could play a similar role to TIFIA, but any

limitations on the source of repayment will need to be considered.

Structuring a PPP

►

►

►

►

Defining the business model – how will the concessionaire earn

revenue and over what period?

Begin with the project’s specific characteristics and public goals

►

Seek efficiencies

►

Optimize risk allocation – construction risk, traffic or volume risk

Develop performance specifications

Be sure that the business model align interests: private partner should

maximize profit by meeting public goals

Page 12

Contact Information

Matthew Hobby

Senior Vice President

Ernst & Young Infrastructure Advisors, LLC

Tel. (212) 773-5615

matthew.hobby@ey.com

Mike Parker

Senior Managing Director

Ernst & Young Infrastructure Advisors, LLC

Tel. (215) 448-3391

mike.parker@ey.com

Page 13

EY | Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transaction and advisory services. The

insights and quality services we deliver help build trust and confidence in the

capital markets and in economies the world over. We develop outstanding leaders

who team to deliver on our promises to all of our stakeholders. In so doing, we

play a critical role in building a better working world for our people, for our

clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member

firms of Ernst & Young Global Limited, each of which is a separate legal entity.

Ernst & Young Global Limited, a UK company limited by guarantee, does not

provide services to clients. For more information about our organization, please

visit ey.com.

Ernst & Young LLP is an EY member firm operating in the US. Ernst & Young

Infrastructure Advisory, LLC is an affiliate thereof and a registered municipal

advisor.

© 2014 Ernst & Young LLP.

All Rights Reserved.

1402-1208926_NY

ED None

This material has been prepared for general informational purposes only and is not intended to

be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for

specific advice.

ey.com