to presentation - IFMR Finance Foundation

advertisement

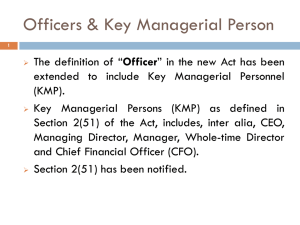

Companies Act 2013 Why a new Companies Act ? • The existing law is over half a century old • New law helps to consolidate and bring related provisions under a single roof • Objective is lesser government approvals, enhanced self regulation and emphasis on corporate democracy • In line with the changed national and international economic environment • Brings about better transparency and stringent regulations Background 2009 2011 2012 2013 2013 • Bill withdrawn due to numerous amendments • Introduced Companies Bill 2011 in December 2011 • Companies Bill passed by Lok Sabha on 18th December 2012 • Passed by Rajya Sabha on 8th August 2013 • Received assent of Hon’ble President on 29th August 2013 Structure of the old and new Act ACT 1956 ACT 2013 13 Parts 29 Chapters 658 Sections 470 Sections 15 Schedules 7 Schedules • 98 Sections have been notified • The Draft rules have been placed for comments from investors on the Ministry of Corporate Affairs website. Highlights of Companies Act 2013 • One Person Company (OPC) • Consolidated financial statements if company has one or more subsidiaries • Key Managerial Personnel • Auditing standards & Secretarial Standards made mandatory • Participation of directors through video conferencing to count for quorum • Definition of a listed company – A company with any of its securities listed on any recognised stock exchange • Uniform Financial year – 1st April to 31st March • Definitions: • ‘Small Company’ • Widening of definition of ‘Officer in Default’ to include KMP Incorporation • Definition of Private Company Object clause of Memorandum of Association • Only single head objects • No segregation into Main Objects, Ancillary/ Incidental objects & Other objects Certificate of Commencement of Business Compliance consequent to name change Companies with Charitable Objects Charges to be registered • All charges on the company’s property, assets or undertaking require registration • No exemption from registration of pledges. • Earlier registration was required only for following: • Securing debenture issue • Uncalled share capital • Immovable property • Book debts • Movable property not being pledge • Floating charge on undertaking • Calls made but not paid • Ship or share in a ship • Goodwill, patent, licence under a patent, trademark or copyright or licence under a copyright Auditors • 5 years tenure for auditors appointed at AGM • Automatic reappointment of existing auditor at AGM where no auditor is appointed/ reappointed • Annual rotation of audit partner and his team where members so resolve. • Listed companies & Prescribed class of companieso An individual as auditor- max 1 term of 5 consecutive years o Audit firm as auditor- max 2 terms of 5 consecutive years • Auditor unless otherwise exempted by the company shall attend any general meeting by himself or through his authorised representative. Auditor not to render foll services Auditor not to render following services to auditee company, its holding company, subsidiary company or associate company • Accounting and book keeping services • Internal audit • Design and implementation of any financial information system • Acturial services • Investment advisory services • Investment banking services • Rendering of outsourced financial services • Management services • Any other kind of consultancy services Accounts ACT 1956 ACT 2013 Consolidation of Accounts not Consolidation of Accounts mandatory mandatory with subsidiaries/ JVs/ associates Financial Year may end on date Financial year can end only on 31st other than 31st March – extension March – no extension permitted at will be granted by ROC present Financial statements to be signed Financial statements can be signed by: by: • 2 directors + CS • Chairperson alone with Board authorization Revision of financial statements Voluntary revision if it appears to director that the financials or Board’s report are not in line with the relevant sections of the Act Requirements • Should be w.r.t 3 preceding financial years. • Approval of Tribunal on an application made by company in prescribed form • File copy of order of Tribunal with ROC Tribunal shall give notice or CG and IT authorities, consider their representations Shall not be prepared/ filed more than once in a FY Reasons for revision to be disclosed in Board’s Report of the year in which revision is made. Further Issue though Private Placement • Can be made to maximum of 50 persons in a financial year excluding QIB • Through a Private Placement Offer letter • Intimate ROC of offer within 30 days of Circulation of Private placement offer letter • Allotment must be made within 60 days of receipt of Application money • If unable to allot, application money to be returned within 15 days of completion of 60 days • If unable to return application money within 15 days, pay the applicant interest @12%p.a. from expiry of 60th day • On allotment, file with ROC a return of allotment. Corporate Social Responsibility (CSR) • Every company having o A net worth of Rs. 500 crore or more OR o A turnover of Rs. 1000 crore or more OR o A net profit of Rs. 5 crore or more shall constitute a CSR Committee consisting of 3 or more directors, out of whom one is independent director. • shall formulate and recommend CSR Policy which shall indicate the activities to be undertaken as specified in schedule VII and shall also recommend the amount of expenditure to be incurred on the CSR activities. • At least 2 % of the average net profits of the company in the 3 immediately preceding financial years is spent every year on CSR activities • Board’s report disclosures o Composition of committee o Reasons for failure to provide or spend such amount NFRA to be constituted under the Act The existing National Advisory committee on Accounting and Auditing Standards (NACAAS) renamed as National Financial Reporting Authority (NFRA) It shall have the same powers vested in a Civil Court while trying a suit. Purpose: • Make recommendation to the CG on formulation and laying down of accounting and auditing policies and standards • Monitoring and compliance of accounting and auditing standards • Oversee the quality of service of professionals associated with compliance Constitution: • Chairperson – a person having expertise in accounts, auditing, finance or law – appointed by the CG • Maximum 15 other members- full time and/ or part time. DIRECTORS Key Highlights • Minimum no of directors retained • Max no of directors increased to 15 (against the earlier 12) • No of directorships – increased to 20 (earlier 15 public ltd companies) • Every company to have at least one director who has stayed in India for at least 182 days in the previous calendar year • CEO/ CFO defined • Prescribed class of companies to compulsorily have at least one woman director • Independent director defined and specific related provisions laid down • Prescribed class of companies to compulsorily have CEO/ CFO and CS Key Managerial Personnel • Key managerial personnel means: - CEO/ MD/ Manager - CS - WTD - CFO - such other person to be prescribed • Included in the definition for an Officer who is in default • Related party includes relative of key managerial personnel • Section 21 interestingly provides that any document/ contract requiring authentication by Company can be signed by KMP/ person authorised by the Board Key Managerial Personnel (contd…) • Annual Return to contain information about KMP and changes if any thereof and their remuneration • Relatives of KMP to not be appointed as auditors • Register of KMP along with securities held by them in the company to be maintained & particulars of change in KMP to be filed with ROC • Section 194 prohibits forward dealings in securities of companies – punishable with imprisonment and fine • Whole-time KMP to be appointed by the Board. If the position becomes vacant the same shall be filled within six months of such vacancy Officer who is in Default Earlier Now - MD/ WTD/ Manager/Person in - WTD/KMP/ Directors specified by the accordance with whose directions the Board – in the absence of such Board is accustomed to act specification, all Directors - No provision to impose liability on all - Where there is no specific directors authorisation by the Board all - External parties not counted in the directors would be held liable. Most definition for Officer in Default importantly, every director who is AWARE of such contravention by virtue of receipt of any proceedings or PARTICIPATION in such proceedings without objecting to the same would be held liable - Share transfer agents, Registrar to an Issue and Merchant Bankers to Issue to be held liable in the event of default in respect of issue or transfer of shares of a company (shares used and not securities) Duties of Director • For the first time duties of directors have been laid down – includes independent directors • Must act in good faith, to exercise duties with care, skill and judgment and shall act in the best interest of the company, employees, community and environment. Contravention of this provision entails fine under the Act. Insider Trading • Directors/ KMP shall not enter into insider trading • Insider trading defined – act of subscribing, buying, selling, dealing or agreeing to subscribe to the securities of the company by any director if he/ she has access to non-public sensitive information OR an act of counseling about procuring or communicating non-public price-sensitive information to any person • Price sensitive information – any information which published could materially affect the price of the securities of the company • Loose ends – not defining ‘non-public’/ ‘materially affect the price of the securities’ MEETINGS Board Meetings – Key Highlights • Gap between two BMs to not exceed 120 days • Board Meetings to have at least seven days’ notice – shorter notice is allowed with the presence of at least one independent director. If held without an independent director, then the transaction is not approved until ratified by at least one independent director • BMs are permitted through video conferencing – capable of being recorded and stored Board Meeting Minutes • In addition to other matters – directors present at the Meeting, names of dissenting directors to be mentioned • “All appointments made at Board Meetings” shall be recorded – unclear • Secretarial standards with regard to BM – to be followed AGMs and EGMs • Provisions of earlier Act retained to a large extent (gap between two AGMs, extension of time for holding AGM, notice of AGM) • Secretarial Standards for AGM also to be made mandatory • Provisions relating to persons who may call for an EGM, persons who may give consent for shorter notice, ordinary & special businesses • Notice of AGM to also be given to directors of the company (in addition to the members and auditors) AGM Notice • Where any business to be transacted affects any other company, where the extent of shareholding every promoter, director, manager, KMP is not less than two per cent of the paid up share capital of that company shall be set out in the explanatory statement to the notice. • Quorum – five (public co), 15 (1000-5000), 30 (>5000) personally present, two (private co) • Secretarial standards with regard to AGM to be followed Disclosures in Annual Return – Section 92 (i) registered office, principal business activities, particulars of its holding, subsidiary and associate companies; (ii) shares, debentures and other securities and shareholding pattern; (iii) indebtedness; (iv) members and debenture-holders along with changes therein since the close of the previous financial year; (v) promoters, directors, key managerial personnel along with changes therein since the close of the last financial year; (vi) meetings of members or a class thereof, Board and its various committees along with attendance details; (vii) remuneration of directors and key managerial personnel; (viii) penalties imposed on the company, its directors or officers and details of compounding of offences; (ix) matters related to certification of compliances, disclosures as may be prescribed; (x) details in respect of shares held by foreign institutional investors; Signing of Annual Return : (i) A director and the Company Secretary, or where there is no Company Secretary, by a Company Secretary in whole-time practice. (ii) in addition to the above, the annual return, filed by a listed company or by a company having such paid-up capital and turnover as may be prescribed, shall be certified by a company secretary in practice that the annual return discloses the facts correctly and adequately and that the Company has complied with all the provisions of the Act. Loan to Directors – Section 185 No Company shall directly or indirectly advance any loan including book debt or give guarantee or provide security to its directors or to any other person in whom the director is interested. ‘any other person in whom the Directors is interested’: 1. any director of the lending Company or its holding co or any partner or relative of any such director 2. any firm in which such director or relative is a partner 3. Any private co of which any such director is a director or member 4. Any body corporate at a GM of which not less than 25% of total voting power is exercised/controlled by any such director, or by two or more 5. Any body corporate, the Board, MD or manager, whereof is accustomed to act in accordance with the directions or instruction of the Board, or of any director or directors, of the lending company. Exception: The said section does not apply to:a. Loan to MD/WTD •As a part of contract of services extended to all its employees; or •Pursuant to scheme approved by members by special resolution b. A Company which in the ordinary course of its business provides loans or gives guarantees or securities for the due repayment of any loan and in respect of such loans an interest is charged at a rate not less than the bank rate declared by RBI Loans & Investments by Company- Sec 186 • List of exemptions taken off (Private Ltd & Subsidiary Companies) • Scope no longer limited to inter-corporate loans & investments, but expanded to include loans to persons. • Rate of interest on loans to be linked to government securities instead of prevailing bank rate. • The full particulars of the loan given, investment made or guarantee given or security provided and the purpose to be disclosed in the financial statement. Investment Limits: Loan Limits not requiring Shareholder Not more than two layers of investment Approval: companies Not exceeding 60% of paid up This shall not affect: capital + free reserves -A company can acquire any other company incorporated in a country outside India, with + securities premium OR subsidiaries beyond 2 layers as per the laws of 100% of free reserves such country. - A subsidiary company having any investment subsidiary to meet the requirement under law. + Securities premium whichever is MORE Related Party Transactions- Section 188 New Provisions: Combines sections 297 and 314 –both the sections dealt with 2 different scenarios Definition of related party widened Purview of related party transaction widened – sale, purchase, leasing of property included Arms length transaction defined CG approval replaced with prior approval of shareholders for prescribed class of companies Related party contracts to be explained in the Board’s report along with justification for the contract No Company shall enter into any contract or arrangement, except with the consent of the Board, with a related party with respect to: sale, purchase or supply of any goods or materials; Selling or otherwise disposing of, or buying, property of any kind; Leasing of property of any kind; Availing or rendering of any services; Appointment of any agent for purchase or sale of goods, materials, services or property; Such related party’s appointment to any office or place of profit in the company, its subsidiary company or associate company and Underwriting the subscription of any securities or derivatives thereof, Exemption - Transactions in the ordinary course of business except those not entered into on arm’s length basis Related Party means: •A Director or his relative; •A Key Managerial Person or his relative; •A Firm, in which director, manager or his relative is a partner •A Private Company, in which director, manager is a director or member; •A Public Company, in which director or manager is a director or holds along with his relatives more than 2% of paid-up capital; •Any body corporate whose Board of Directors, Managing Director or Manager is accustomed to act in accordance with the advice, directions or instructions of a director or manager; •Any person on whose advice, directions or instructions a director or manager is accustomed to act; •Any company which is a holding, subsidiary or an associate company of such company or a subsidiary of a holding company to which it is also a subsidiary. Board Committees1. Audit Committee: Section 177 -Applicable in case of Listed Companies and such other class of Companies as may be prescribed -Minimum of 3 directors with independent directors forming a majority -Majority of members including its Chairperson shall be persons with ability to read and understand the financial statement. -The Company to establish a vigil mechanism for Directors and Employees to report genuine concerns. 2. Nomination and Remuneration Committee -Section 178 -Mandatory in the case of listed companies and such other class or classes of companies as may be prescribed. -The Committee shall formulate the criteria for determining qualifications, positive attributes and independence of a director and recommend to the Board a policy, relating to the remuneration for the directors, key managerial personnel and other employees -It shall consist of three or more non-executive director(s) out of which not less than one half shall be independent directors. 3. Stakeholders Relationship Committee: Where the combined membership of the shareholders, debenture holders, deposit holders and any other security holders is more than one thousand at any time during the financial year, the company shall constitute a Stakeholders Relationship Committee. It shall consider and resolve the grievances of security holders of the company. **The chairperson of each of the committees or, in his absence, any other member of the committee authorised by him shall attend the general meetings of the company. Winding Up- Section 271 Companies Act, 1956 Criteria provided for winding-up of company such as:• If the company has, by special resolution, resolve that the company be wound up • If the company is unable to pay its debt • If a company does not commence its business within 1 year from its incorporation or suspends its business for a whole year • If the minimum no. of members is reduced below 2 in case of private and 7 in case of public company. Companies Act, 2013 Certain criteria for winding-up deleted like minimum number of members falling below prescribed limit, non commencement of business for 1 year etc. Additional ground providing for winding-up:On an application made by the Registrar or any other person authorized by CG by notification under this Act, the tribunal is of the opinion that: The affairs of the company have been conducted in a fraudulent manner or Company was formed for fraudulent and unlawful purpose or The persons concerned in the formation or management of its affairs have been guilty of fraud, misfeasance or misconduct in connection therewith. Dormant Company – Section 455 Where a company is formed and registered under this Act: -for a future project or to hold an asset or intellectual property and -has no significant accounting transaction may make an application to the registrar for obtaining the status of Dormant company. The Registrar will issue a certificate to that effect. To retain the status the Company shall have such minimum number of directors, file such documents and pay such annual fee as may be prescribed to the Registrar. On an application it may become an active company. In case of failure to comply with the requirements, the Registrar may strike off the name from the register of dormant companies Grounds of Strike Off – Section 248 A company may be struck off by ROC for below reasons:• Company has failed to commence its business within 1 year of its incorporation • Subscribers to the memorandum have not paid the subscription money within 180 days from the date of incorporation • Company is not carrying on any business or operation for a period of 2 immediately preceding financial years and has not made any application within such period for obtaining the status of a dormant company. National Company Law Tribunal- 408 & 410 The act proposes to go away with the jurisdiction of the High Court and Company Law Board and replace the same with a single forum called the National Company Law Tribunal (NCLT- yet to be set up), appeals from which will lie with the National Company Law Appellate Tribunal. Constitution: Bench of Judicial and Technical Members Special Courts (Section 435 & 436) •Will be established for the speedy trial of offences. • All offences under this Act shall be triable by the Special Court Mediation and Conciliation Panel (Section 442) A panel of experts for mediation between the parties during the pendency of any proceedings before the Central Government or the Tribunal or the Appellate Tribunal under this Act. Thank you IFMR Rural Channels and Services Private Limited IITM Research Park | A1 | 10th Floor | Kanagam Village | Taramani | Chennai – 600 113 | Tamil Nadu | India http://ruralchannels.ifmr.co.in/ Small Company Small company means a company other than a public company i. paid-up share capital of which does not exceed Fifty Lakh or such higher amount as may be prescribed not exceeding Five Crore; or i. turnover of which as per its last profit and loss account does not exceed Two Crore or such higher amount as may be prescribed not exceeding Twenty Crore. Exemptions: • Holding company or subsidiary company • Company registered under section 8 • Company or body corporate governed under Special Act Private Company Definition: A company having minimum paid-up share capital of one lakh rupees or such higher number as maybe prescribed and which by its articles; • Restricts the right to transfer its shares; • Except in case of One Person Company, limits the number of its members to two hundred; • Prohibits any invitation to public to subscribe for any securities of the company • Silent about acceptance of deposits Deposits – Who can accept? Only the following companies may invite, accept or renew deposits from the public: • • • • Banking companies NBFCs Notified companies Public company having prescribed net worth or turnover A company not covered above may invite, accept or renew deposits from MEMBERS subject to: • • • Passing resolution at general meeting Compliance with RBI rules Terms of security and repayment of deposit and interest agreed upon between company and members Fulfilment of following conditions: • • Circular to members with financial position of company, credit rating obtained, amount due towards deposits previously accepted, other prescribed matters Filing a copy of circular with the statements with Registrar within 30 days before issue of circular Commencement of Business PARTICULARS ACT 1956 ACT 2013 APPLICABILITY Only to PUBLIC companies To all Companies having SHARE CAPITAL Applicable companies not to commence business until: • A declaration is filed by a director that every subscriber has paid the value of shares subscribed by him • The paid up capital of the private company is not less than Rs. 100,000 • Company has filed a verification of registered office address Compliances consequent to name change If the name change happened in the preceding 2 years, the former name along with the new name must be: • Painted or affixed outside every office or place of business • Printed on business letters , bill heads, letter papers, notices and other official publications. • Displayed along with telephone numbers, e-mail IDs and website addresses. Impact Change of name of IFMR Rural Channels and Services (IRCS) w.e.f. 28.11.2011. (within the last 2 years) Companies with Charitable Objects etc. PARTICULARS O B J E C T S ACT 1956 ACT 2013 Can be incorporated for the following objectives: • • • • • Art Science Religion Charity Any other useful object Additionally for the following • • • • • Sports Education Research Social welfare Environment Protection If license is revoked • Company maybe wound up OR • Amalgamated with another Clause 8 company with similar objects Impact: Pudhuaaru Kshetriya Gramin Financial Services