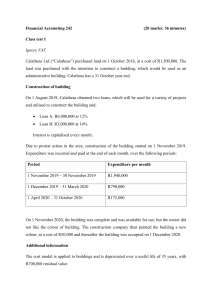

Actividad 4: Cap. 10 Propiedad, planta y equipo E10.2 (LO1, 2) (Acquisition Costs of Realty) Pollachek Co. purchased land as a factory site for $450,000. The process of tearing down two old buildings on the site and constructing the factory required 6 months. The company paid $42,000 to raze the old buildings and sold salvaged lumber and brick for $6,300. Legal fees of $1,850 were paid for title investigation and drawing the purchase contract. Pollachek paid $2,200 to an engineering firm for a land survey, and $65,000 for drawing the factory plans. The land survey had to be made before definitive plans could be drawn. Title insurance on the property cost $1,500, and a liability insurance premium paid during construction was $900. The contractor's charge for construction was $2,740,000. The company paid the contractor in two installments: $1,200,000 at the end of 3 months and $1,540,000 upon completion. Interest costs of $170,000 were incurred to finance the construction. Instructions Determine the cost of the land and the cost of the building as they should be recorded on the books of Pollachek Co. Assume that the land survey was for the building. TERRENO $450,000 $42,000 -$6,300 $1,850 $1,500 Total = $489,050 EDIFICIO $2,200 $65,000 $900 $2,740,000 $170,000 Total = $2,978,100 Cap. 11. Depreciación, deterioro y agotamiento. E11.5 (LO1, 2) (Depreciation Computations—Four Methods) Maserati SpA purchased a new machine for its assembly process on August 1, 2019. The cost of this machine was €150,000. The company estimated that the machine would have a residual value of €24,000 at the end of its service life. Its life is estimated at 5 years, and its working hours are estimated at 21,000 hours. Year-end is December 31. Instructions Compute the depreciation expense under the following methods. Each of the following should be considered unrelated. a. Straight-line depreciation for 2019. = (€150,000 - €24,000) * 100% / 5 años = €25,200 * 5/12 = €10,500 b. Activity method for 2020, assuming that machine usage was 800 hours. (€150,000 − €24,000) = €6 𝑝𝑜𝑟 ℎ𝑜𝑟𝑎 21,000 800 horas * €6 = €4,800 c. Sum-of-the-years'-digits for 2020. = 5∗(5+1) = 15 2 Años de uso 1 2 Proporción 5/15 * 4/15 * €126,000 = €126,000 = €42,000 €33,600 €150,000 = €90,000 = €60,000 €36,000 2020 7/12 * €42,000 = €24,500 5/12 * €33,600 = €14,000 TOTAL = €38,500 d. Double-declining-balance for 2020. 𝐷𝑜𝑏𝑙𝑒 % = 100% ∗ 2 = 40% 5 𝑎ñ𝑜𝑠 Años de uso 1 2 2020 Proporción 40% * 40% * 7/12 * €60,000 = €35,000 5/12 * €36,000 = €15,000 TOTAL = €50,000 E11.20 (LO3) (Impairment) The management of Sprague Inc. was discussing whether certain equipment should be written off as a charge to current operations because of obsolescence. This equipment has a cost of $900,000 with depreciation to date of $400,000 as of December 31, 2019. On December 31, 2019, management projected the present value of future net cash flows from this equipment to be $300,000 and its fair value less cost of disposal to be $280,000. The company intends to use this equipment in the future. The remaining useful life of the equipment is 4 years. Instructions a. Prepare the journal entry (if any) to record the impairment at December 31, 2019. 2019 Dr. Pérdida por deterioro Cr. $200,000 Deterioro acumulado $200,000 b. Where should the gain or loss (if any) on the write-down be reported in the income statement? Otros gastos y pérdidas c. At December 31, 2020, the equipment's recoverable amount is $270,000. Prepare the journal entry (if any). 2020 Dr. Cr. Deterioro acumulado Ganancia x recuperación de deterioro $45,000 $45,000 Cost $900,000 Accumulated depreciation $400,000 Value-in-use $300,000 Fair value less cost of disposal $280,000 Costo $900,000 (-) Depr. Acum. $400,000 (=) Valor Neto $500,000 Deterioro $500,000 - $300,000 = $200,000 Equipo $900,000 (-) Depr. Acum. $400,000 (-) Deterioro $200,000 (=) Valor Neto $300,000 Dep. = ($300,000 - $0) / 4 años = $75,000 annual Equipo $900,000 (-) Depr. $475,000 (-) Deterioro $200,000 (=) Valor Neto $225,000 Valor recuperable = $270,000 Recuperación de deterioro = $270,000 - $225,000 = $45,000 Equipo $900,000 (-) Depr. $475,000 (-) Deterioro $155,000 (=) Valor Neto $270,000