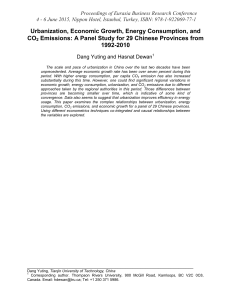

Ecological Economics 70 (2011) 1344–1353 Contents lists available at ScienceDirect Ecological Economics j o u r n a l h o m e p a g e : w w w. e l s ev i e r. c o m / l o c a t e / e c o l e c o n Analysis The impact of urbanization on CO2 emissions: Evidence from developing countries☆ Inmaculada Martínez-Zarzoso a,b,⁎, Antonello Maruotti c,1 a b c Ibero America Institute for Economic Research, Universität Göttingen, Germany Instituto de Economía Internacional, Universitat Jaume I, Spain Dipartimento di Istituzioni Pubbliche, Economia e Società, Università di Roma Tre, Via Gabriello Chiabrera, 199–00145 Roma, Italy a r t i c l e i n f o Article history: Received 18 December 2009 Received in revised form 10 February 2011 Accepted 12 February 2011 Available online 30 March 2011 JEL classification: Q25 Q4 Q54 Keywords: CO2 emissions Developing countries Panel data Semi-parametric mixture model Urbanization a b s t r a c t This paper analyzes the impact of urbanization on CO2 emissions in developing countries from 1975 to 2003. It contributes to the existing literature by examining the effect of urbanization, taking into account dynamics and the presence of heterogeneity in the sample of countries. The results show an inverted-U shaped relationship between urbanization and CO2 emissions. Indeed, the elasticity emission-urbanization is positive for low urbanization levels, which is in accordance with the higher environmental impact observed in less developed regions. Among our contributions is the estimation of a semi-parametric mixture model that allows for unknown distributional shapes and endogenously classifies countries into homogeneous groups. Three groups of countries are identified for which urbanization's impact differs considerably. For two of the groups, a threshold level is identified beyond which the emission-urbanization elasticity is negative and further increases in the urbanization rate do not contribute to higher emissions. However, for the third group only population and affluence, but not urbanization, contribute to explain emissions. The differential impact of urbanization on CO2 emissions should therefore be taken into account in future discussions of climate change policies. © 2011 Elsevier B.V. All rights reserved. 1. Introduction Climate change with the attendant need to stabilize contributing global emissions is one of the most challenging problems of our times, and a matter of great concern among policy makers. Some aspects of the projected impact such as global warming, increasing desertification, rising sea levels and rising average temperatures, might have a disproportionate impact on developing countries, which least contributed to the cause of climate change. The main greenhouse gas in terms of quantity is CO2, which according to IPCC (2007) accounted for about 76.7% of total anthropogenic greenhouse gas emissions in 2004. Although the reduction commitments of CO2 emissions were seen as a task predominantly for developed countries (UNFCCC, 1997), based on the consensus that they are the largest contributors to global CO2 emissions, there have been recent calls for the developing countries to play an active role in global emissions reduction (Winkler et al., 2002). The level of CO2 emissions from developing countries has ☆ I would like to thank the editor and four anonymous referees for their diligent review, excellent comments, and very valuable suggestions. I acknowledge the support and collaboration of Proyecto ECO2010-15863. ⁎ Corresponding author at: Ibero America Institute for Economic Research, Universität Göttingen, Platz der Goetinger Sieben 3, 37077 Göttingen, Germany. Tel.: +49 551399770; fax: +49 551398173. E-mail addresses: martinei@eco.uji.es (I. Martínez-Zarzoso), antonello.maruotti@uniroma3.it (A. Maruotti). 1 Tel.: + 39 06 57335305. 0921-8009/$ – see front matter © 2011 Elsevier B.V. All rights reserved. doi:10.1016/j.ecolecon.2011.02.009 been rapidly exceeding that of the developed countries and in 2003 accounted for almost 50% of the world's CO2 emissions (Fig. 1). This trend is expected to grow if the current path in terms of energy consumption is maintained. Since CO2 is one of the main contributors to global emissions, it is of great interest to determine which policy measures will be more effective in curbing CO2 emissions. While many factors have been adduced for climate change, as affluence grows, energy consumption is singled out as having the most adverse impact on the environment. However, this impact is more severe when accompanied by demographic growth and rural migration into cities, given that population increases and urban development lead to increases in energy consumption and, consequently, to greater atmospheric pollution. Especially in developed regions the process of economic development is accompanied by agricultural intensification, industrialization and urbanization, with large scale movements of labor force from rural to urban settlements. Urban economic activities may influence environmental quality in a distinct way as industrialization does. On the one hand, higher densities may place an excessive burden on absorptive capacities of the local environment. On the other hand, high urban density may also influence patterns of resource use and global environmental quality. Urbanization allows for economies of scale in production but requires transportation. Indeed, urbanization exerts a number of independent influences in energy use. It constantly displaces traditional energy with modern energy, which substantially increases the energy intensity of some activities while decreasing traditional I. Martínez-Zarzoso, A. Maruotti / Ecological Economics 70 (2011) 1344–1353 Fig. 1. Carbon dioxide emissions in 2003. Source: World Development Indicators 2007. energy use. These changes can ultimately result in increasing emissions that may contribute to the global warming effect. However, the process of urbanization also involves concentration of firms in space reducing the cost to enforce environmental legislation, and can also encourage the use of mass transport in place of motor vehicles (Jones, 1991). Since the early 70s a scientific consensus emerged pointing to human induced forces driving global warming. The IPAT2 model in stochastic form, named STIRPAT, has been used by ecologists, sociologists and economists to assess the impact of population, affluence and other factors on carbon dioxide loads (e.g. York et al., 2003; Shi, 2003; Martínez-Zarzoso, Bengochea-Morancho and Morales-Lage, 2007). The model has been used to assess not only the impact of the core components population and affluence on environmental impact, but also to address sociological questions like the impact of modernization on the environment (York et al., 2003). In the last two decades a number of researchers, mainly economists, have investigated the determinants of CO2 emissions within the framework of the Kuznets Curve hypothesis. It suggests an invertedU shaped curve between economic development and environmental impact. However, most of the studies do not reach conclusive evidence in favor of the hypothesis (See Perman and Stern, 2003, for a survey). More recent developments use decomposition analysis and efficient frontier methods taking into account not only affluence but also energy intensity, technical change, and structural change as explanatory variables. In most cases changes in per-capita CO2 emissions are explained by changes in income per capita, energy intensity, and structural change in the economy (assuming implicitly that population has a unitary elasticity with respect to emissions). Relatively little effort has been devoted to investigating the impact of demographic factors on the evolution of CO2 emissions and most of the existing studies assume that this impact is comparable for all countries and constant over time (Jones, 1991; York et al., 2003; Parikh and Shukla, 1995; Cole and Neumayer, 2004). Two exceptions to this general assumption are the studies of Shi (2003), who grouped countries according to income levels, and Martínez-Zarzoso et al. (2007), who studied the impact of population growth for old and new European Union members. Both studies focus specifically on 2 Impact = Population Affluence Technology (IPAT). 1345 the differential impact of population growth on emissions – without considering urbanization. As in Jones (1991) and Parikh and Shukla (1995), this paper specifically focuses on the influence of urbanization on global environmental quality, but, as a novelty, it introduces the assumption of differential impacts across countries. Especially given the rapid pace of urban growth in middle and low income countries, there is a need to understand the interactions between urbanization and global environmental change processes. This paper contributes to this literature in two different ways. The first novelty is to focus on the impact of urbanization on CO2 emissions for developing countries, by introducing non-linearities and dynamics in the model and by controlling for affluence and technique effects. Given the revealed persistence of CO2 emissions we use a dynamic specification which allows us to account for the path-dependent nature of the distributional pattern. The resulting endogeneity problem is addressed by using a Least Squares Dummy Variable Corrected (LSDVC) and several instrumental variables and GMM estimators, which are recently-proposed panel data techniques particularly suitable for macro-panels. The second novelty of this paper regards the estimation technique used to address differential impacts for different groups of countries. We estimate a semiparametric mixture model that allows for unknown distributional shapes and endogenously classifies countries into homogeneous groups. To the best of our knowledge this has not been done before. The study focuses on developing countries, because few studies have dealt with this group of countries before (Parikh and Shukla, 1995), and considers the heterogeneity present in the sample in terms of variability of the estimated coefficients across different groups of countries. We specify a model in which CO2 emissions are related to the level of income per capita, the population size, the percent of urban over total population, the industrial structure, and the energy intensity of each country. The study classifies countries into groups following statistical procedures. The results show that not only affluence but also urbanization drives emissions following a Kuznets curve as predicted by the Ecological Modernization Theory (EMT) developed by sociologists. This impact is not homogeneous, so countries are classified into three groups according to the differential impact of the factors influencing emissions. The paper is organized as follows. Section 2 briefly reviews the relevant literature. Section 3 presents the theoretical framework and specifies the model. Section 4 describes the empirical analysis and discusses the main results and Section 5 concludes. 2. Literature Review The first studies that considered demographic factors to explain the sources of air pollution were based on cross-sectional data for only one time period and consider mainly the effects of population growth (Cramer, 1998, 2002; Daily and Ehrlich, 1992; Dietz and Rosa, 1997; Zaba and Clarke, 1994; Cramer and Cheney, 2000). The results from these studies indicate that the elasticity of CO2 emissions and energy use with respect to population are close to unity. Some other studies used panel data and relaxed the assumption of equal impact of population for all countries. In this line, Shi (2003) found a direct relationship between population changes and carbon dioxide emissions in 93 countries over the period from 1975 to 1996 that varies with the levels of affluence. Indeed, he shows that the impact of population on emissions has been more pronounced in lower-income countries than in higher-income countries. Also Martínez-Zarzoso et al. (2007) found a differential impact of population on emissions for old and new EU members. Total population was the only demographic variable considered in both studies. A number of carbon-emissions/energy consumption studies have included not only total population but also additional demographic variables — among them urbanization, population density and age composition. The results from those studies show at best mixed 1346 I. Martínez-Zarzoso, A. Maruotti / Ecological Economics 70 (2011) 1344–1353 results. The first strand of studies (Jones, 1991; Parikh and Shukla, 1995; York et al., 2003) used cross-sectional data for a single year. Jones (1991) focused exclusively on urbanization and the mechanisms by which it alters energy consumption. He conducted a regression analysis of 59 developing countries for 1980 to study the overall impact of urbanization on energy-use. He concluded that a 10% increase in the proportion of the population living in cities would increase modern energy consumption per capita by 4.5–4.8%, holding constant per capita income and industrialization. Parikh and Shukla (1995) also provided an early analysis of the effect of urbanization on energy use and greenhouse gas emissions in developing countries. They estimated two models: a panel data fixed-effects model for energy consumption per capita over the period 1965–87 and a crosssectional model estimated for the year 1986 for four greenhouse gasses in per capita terms. The set of explanatory variables were in both models income per capita, share of agriculture in GDP, population density and urban population rate. Their results for the period 1965–87 indicate that a 10% increase in a country's urban population leads to a 4.7% rise in its per capita total energy consumption. The effect on CO2 emissions is only calculated with 1986 data and it is somewhat lower: a 10% increase in a country's urban population leads to a 0.3% rise in its per capita CO2 emissions. York et al. (2003) tested for a non-linear relationship between emissions and urbanization for a cross-section of 137 countries using 1991 data and found that the squared term was negative but not statistically significant. The main shortcoming of those investigations is that the results may be biased due to unobserved countryheterogeneity stemming from different country regulations or behaviors that affect emissions differently for different countries and are not measurable. A second strand of studies overcome this lacking by estimating the effect of demographic factors using panel data (Cole and Neumayer, 2004; Fan et al., 2006; York, 2007; Liddle and Lung, 2010). In this context Cole and Neumayer (2004) considered 86 countries during the period from 1975 to 1998 and found a positive link between CO2 emissions and a set of explanatory variables including population, urbanization rate and energy intensity, and a negative link with household sizes. With respect to urbanization they found that a 10% increase in the urbanization rate increases CO2 emissions by 7%. They estimated a model in first differences that included income per capita and energy intensity as additional regressors. The authors assumed that the effect of population and urbanization is equal for all income levels. Fan et al. (2006) and York (2007) both focused exclusively on developed countries. Whereas the former finds a negative relation between urbanization and carbon emissions for their OLS regressions, the latter author reports a positive relationship between urbanization and energy use for 14 EU countries. Finally, Liddle and Lung (2010) focused on the impact of age-structure on carbon emissions and also considered urbanization as an explanatory factor. Their results show a positive and non-significant effect of urbanization on aggregate carbon dioxide emissions for a cross-section of 17 developed countries and 10 periods (panel span 1960–2005 using observations at 5-year intervals). Summarizing, the results with respect to the relationship between urbanization and emissions are not conclusive and the relationship between economic development and urban environmental performance is still not well understood, especially for developing countries. We hypothesize that several reasons could be responsible of this lack of consensus. First, the relationship could be non-linear and second it could differ by groups of countries. A different but related research approach examines the “Environmental Kuznets Curve” (EKC) hypothesis suggesting an inverted U-shape relationship between pollution per capita and economic development. A few studies considered population density as an additional explanatory variable (e.g., Cole et al., 1997; Panayotou et al., 2000; Dinda, 2004). The results obtained within this framework are far from homogeneous and their validity has been questioned in recent surveys of the EKC literature (e.g., Stern, 1998, 2004). Most of the criticisms are related to the econometric techniques and the presence of omitted-variables bias (Perman and Stern, 2003). Borghesi and Vercelli (2003) state that the studies based on local emissions present acceptable results, whereas those concerning global emissions do not offer the expected outcomes, and therefore the EKC hypothesis cannot be generally accepted. A few other researchers considered the existence of an inverted U-shape relationship between pollution per capita and urbanization (Ehrhardt-Martinez et al., 2002; York et al., 2003). The main theoretical justification draws on ecological modernization theory that basically argues that capitalist economies have the ability to promote environmental goals. Ehrhardt-Martinez et al. (2002) and York et al. (2003) argued that urbanization is a good proxy for modernization and therefore environmental impact should decrease with higher shares of urban population. 3. Theoretical Framework and Hypothesis In this paper we have taken the STIRPAT model as the reference theoretical and analytical framework, but also consider the economic theories that predict an EKC with respect to income and the sociological theories that suggest an EKC relative to urbanization, rather than economic development per se. Starting from Ehrlich and Holdren's (1971) basic foundation, Dietz and Rosa (1994, 1997) formulated a stochastic version of the IPAT equation with quantitative variables containing population size (P), affluence per capita (A), and the weight of industry in economic activity as a proxy for the level of environmentally damaging technology (T). These authors designated their model with the term STIRPAT (Stochastic Impacts by Regression on Population, Affluence, and Technology). The model specification for a single year is given by the following equation: β β β Ii = αPi 0 Ai 1 Ti 2 ei ð1Þ where Ii, Pi, Ai, and Ti denote Impact, Population and Technology in country i; α and the β's are parameters to be estimated, and ei is the random error. The STIRPAT model has been widely used to analyze the determinants of a variety of environmental impacts (Dietz and Rosa, 1997; Cramer, 1998; Shi, 2003; York et al., 2003; Cole and Neumayer, 2004; among others). York et al. (2003) refined the STIRPAT model and discussed how it can be expanded to incorporate additional factors, such as quadratic terms or different components of P, A or T. P is measured with total population and with the percentage of urban population. The affluence variable, A, is measured by the gross domestic product per capita and, as a proxy for measuring T, we have considered the percentage of industrial activity with respect to total production and energy efficiency. On the one hand, the inclusion of a quadratic term of affluence (A) is in line with economic theories predicting an inverse U-shaped relationship between economic development and environmental impact (Andreoni and Levinson, 2001). On the other hand, the inclusion of a quadratic term of one component of P, population living in urban areas, is in line with modernization theories (EhrhardtMartinez, 1998). Though urbanization is often associated with greater levels of pollution it may also facilitate some environmental improvements, for example through economies of scale in the provision of sanitation facilities. We hypothesize that CO2 production is based on demographics but can shift once efficiency of living in a city is reached. In particular, urban economic activities may have two separate environmental effects — apart from those related to higher incomes, higher consumption levels and industrialization. First, urbanization accelerates the transition to modern fuels changing the patterns of 10 lco2 5 0 resource use. Second, urban areas provide better opportunities to achieve economies of scale and to use natural resources more efficiently than rural areas. Indeed, compact cities are usually more efficient than disperse ones. Therefore, the way in which cities are designed is an important issue for sustainable development. A higher urbanization rate can also have a positive impact on emissions due to the typically more pollution intensive consumption patterns of individuals in urban areas. Indeed, in developing countries, we would expect those in urban areas to utilize cars, motor cycles and busses to a greater extent than those in rural areas. Similarly, passenger transport in cities is heavily weighted towards fuel-using modes (Jones, 1991). 1347 15 I. Martínez-Zarzoso, A. Maruotti / Ecological Economics 70 (2011) 1344–1353 10 4. Empirical Application 15 20 lp 4.2. Model Specification Following the empirical model formulated by Dietz and Rosa (1997) we have estimated an extended version of the STIRPAT model for an unbalanced panel with 1925 observations. The empirical analysis is also in line with the latest emerging approaches based on extended EKC models described in the introduction. In our view, the factors driving changes in pollution should be analyzed in a single model and under the appropriate quantitative framework, hence allowing for a more flexible model with variable coefficients across groups with different behavior. In order to test whether the evolution of the factors considered in the STIRPAT model influences the level of CO2 emissions through time and across countries, we have derived the empirical model by taking logarithms of Eq. (1) and adding the time dimension as follows: lnIit = δi + β0 lnPit + β1 lnAit + β2 lnTit + ϕt + εit ð2Þ where I, P, A, and T are defined above. The sub-index i refers to countries and t refers to the different years. δi and ϕt capture country 3 Energy efficiency is available for 31 low-income countries, 39 lower-middleincome countries, 25 upper-middle-income countries. 10 5 0 Our dataset include all developing nations for which data on all variables are available. This covers 88 countries over the period 1975 to 2003. The sample of countries is considerably reduced when energy efficiency is included as an explanatory variable since data for this variable is not available for many developing countries.3 There are also some countries for which income data is missing and transition economies only report data since the early 1990s when their economies began to open up. With illustrative purposes, the countries under analysis are classified into income groups according to data from the World Development Indicators (WDI) 2007. Low-income economies are those in which 2005 GNI per capita was $875 US or less (54 countries). Lower-middle-income economies are those in which 2005 GNI per capita was between $876 and $3466 (58 countries), upper-middle-income economies are those in which 2005 GNI per capita was between $3466 and $10,725 (40 countries). Countries considered in each group are listed in Table A.1 in the Appendix A (WDI, World Bank, 2007). A summary of the data, as well as the simple correlation coefficients between the variables in the model, is shown in Table A.2 in the Appendix A. In addition, Fig. 2 reports two scatter plots. The first one shows a clear positive linear relationship between population and emissions, whereas the second shows a positive relationship between urbanization and emissions for low urbanization levels and a negative one for higher levels. We proceed now with a more sophisticated analysis to investigate this relationship in depth. 15 4.1. Data and Variables 0 20 40 60 80 100 --urban population (% of total)-lco2 Fitted values Fig. 2. Scatter plot: CO2 and population and CO2 and urbanization. Note: lp denotes population in natural logs, pupc is the percentage of urban population over total population and lco2 denotes logged CO2 emissions. and time fixed effects respectively, and εit is the error term. Since the model is specified in natural logarithms the coefficients of the explanatory variables can be directly interpreted as elasticities. The time effects, ϕt, can be considered as a proxy for all the variables that are common across countries but vary over time. These effects are sometimes interpreted as the effects of emissions-specific technical progress over time (Stern, 2002), but they could account for other effects related to globalization. Model 2 is augmented with urbanization measured as the percentage of population living in cities. In addition, we look at the age composition of population by adding two variables — namely the percentage of population that is above 65 and the percentage of population that is between 14 and 64 years old. The inclusion of population density (pdit) instead of population as a regressor is also considered. Finally, we adopt a less restrictive functional form that introduces squared terms for affluence and urbanization. In this way we are able to test for the EKC hypothesis and the modernization theory. In addition, we consider a dynamic specification that takes into account the effect of past CO2 emissions on the current levels. The augmented model is given by 2 lco2it = δi + ϕt + λlco2i;t−1 + γ0 lyhit + γ1 lyhit + γ2 lpit + γ3 lpupit + γ4 lpup2it + γ5 lp1564it + γ6 lp65it + ð3Þ + γ7 leiit + γ8 liait + εit where l denotes natural logarithms, co2 are the CO2 emissions in tons, yh is the gross domestic product per capita expressed in constant PPP (purchasing parity prices) (2000 US$), p is the total population, pup is 1348 I. Martínez-Zarzoso, A. Maruotti / Ecological Economics 70 (2011) 1344–1353 Table 1 Panel-unit root test results. (1975–2003) Exogenous variables: individual effects Method Levin, Lin & Chu test (LLC) Var levels Statistic Prob.*** Cross-sections Obs Statistic Prob.*** Cross-sections Obs lco2 lpop lyh lei1 lpup −7.26 −13.40 −15.95 −15.55 −12.14 0.00 0.00 0.00 0.00 0.00 145 148 132 88 148 3892 3641 3101 1996 3854 430.82 1239.35 689.59 473.01 1770.02 0.00 0.00 0.00 0.00 0.00 145 148 132 88 148 3995 4106 3220 2034 4106 145 148 132 88 148 3894 3958 3075 1980 3858 426.48 563.76 334.62 197.97 2429.85 0.00 0.00 0.00 0.12 0.00ns 145 148 132 88 148 3995 4106 3220 2034 4106 PP–Fisher Chi-square Exogenous variables: individual effects, individual linear trends lco2 −7.50 0.00 lpop −25.75 0.00 lyh −7.63 0.00 lei1 −6.34 0.00 lpup −5.11 0.00 Notes: Newey–West bandwidth selection using Bartlett kernel. Automatic selection of lags based on SIC. LLC Null: Unit root (assumes common unit root process). PP Null: Unit root (assumes individual unit root process).*** denotes rejection of the null hypothesis at the 1% level and ns denotes not statistically significant. the percentage of total population living in urban areas, p1564 denotes the percentage of population between 15 and 64 years old, p65 denotes the percentage of population older than 64, ei denotes energy efficiency measured as GDP at constant PPP prices divided by energy use, where energy use refers to apparent consumption (production + imports − exports), and finally ia is the percentage of the industrial activity with respect to the total production measured by the GDP. Eq. (3) is estimated for the full sample of countries using paneldata estimation techniques that are appropriate for dynamic models: LSDVC, fixed-effects instrumental variable and GMM methods. Such a model specification may however fail to fit the data due to a misspecification of the model (due to e.g. omitted covariates) or due to the possible correlation among country observations. We also adopt a more flexible estimation procedure that overcome these two Table 2 Regression results for all countries in the sample (1975–2003). lco2(− 1) lyh Lyh2 lp lpup lpup2 M1 M2 M3 M4 M5 M6 FE CLSDV FE_IV_1 FE_IV_2 FE_IV_3 Diff-GMM 0.726*** 18.587 0.675*** 2.737 −0.02 −1.378 0.246** 2.255 0.506* 1.791 −0.089* −1.945 0.790*** 51.104 0.282*** 8.006 0.680*** 9.725 0.424*** 4.636 0.678*** 9.657 0.429*** 4.652 0.674*** 9.384 0.412*** 4.807 0.521*** 3.173 0.715*** 4.464 0.198** 2.005 0.586** 2.312 −0.101*** −2.644 0.319** 2.453 0.755*** 2.902 −0.121*** −3.064 0.311** 2.431 0.861*** 2.899 −0.136*** −3.063 0.357 0.795 1.329* 1.961 −0.209* −1.853 −0.658*** −4.975 0.112 1.623 Yes lpd 0.741*** 2.89 −0.120*** −3.068 0.336** 2.561 lp1564 −0.283*** −4.277 0.125*** 4.143 Yes −0.283*** −4.273 0.124*** 4.089 Yes 0.255 1.335 0.055 0.698 −0.276*** −4.409 0.125*** 4.121 Yes 0.821 1831 0.162 784.731 1.272 0.259 0.449 0.503 0.821 1831 0.161 785.798 1.255 0.263 0.833 1831 0.161 786.606 1.156 0.282 lp65 lei lia Time dummies Within R2 Adjusted R2 Nobs RMSE Log lik Hansen test prob. Endog. test prob. Ar(1) prob. Ar (2) prob. −0.244*** −4.636 0.108*** 2.918 Yes 0.85 −0.167*** −5.33 0.108*** 3.184 Yes 1925 0.163 773.738 1925 1833 N° Instr = 60 1.002 0.988 0.015 0.725 Note: All the variables are in natural logs. GDPpc denotes per capita income. t-statistics are below each estimated coefficient. *, **, *** denote significance at the 10, 5, and 1% level, respectively. FE denotes fixed effects. IV denotes instrumental variables estimator. Bootstrapped standard errors in brackets (bias correction initialized by Arellano-Bond estimator). Diff-GMM denotes difference Generalized Method of Moments. The Hansen test results indicate that the instruments used are valid instruments. Ar(1) and Ar(2) tests for autocorrelation of first and second order respectively, since the model is estimated in first differences we expect to have autocorrelation of first order but not of second order, which is what the probabilities associated to the tests indicate. RMSE denote Root Mean Squared Error. I. Martínez-Zarzoso, A. Maruotti / Ecological Economics 70 (2011) 1344–1353 inconveniences and, in addition allow us to account for the possibility that some of the parameters of the model may differ across unobserved subgroups. A simple way to do so is through latent class (LC) models (Vermunt and Magidson, 2002), also known as finite mixture models. Because of their flexibility, LC are being increasingly exploited as a convenient, semi-parametric way in which to model unknown distributional shapes (Alfò et al., 2008). This is in addition to their obvious applications where there is group-structure in the data or where the aim is to explore the data for such structure (Wedel and DeSarbo, 1995). Following this path we assume that the amount of CO2 emissions, co2it, can be clustered into K groups. Formally, we introduce a latent variable Z that takes K discrete values, say z1,…zK, with distribution P(Z = zk) = πk, 0 ≤ πk, ≤ 1, k = 1,…K, and Σk πk = 1. The probability density function is then given by 2 f ðco2it Þ = Σk πk; f k lco2it jβk ; σk ð4Þ where fk(.) denotes the conditional distribution of Iit within the k-th latent class and πk represents the prior probability of component k. In our application f(.) is a univariate Gaussian density, with componentspecific parameter vector given by θk = (βkX,σ 2k) and complete parameters vector equal to ψ = (π1…,πK, θ1,…,θK); in which Eq. (4) describes a mixture of standard linear regression models (DeSarbo and Cron, 1988). In this framework, parameter estimation can be carried out through an Expectation–Maximization (EM) algorithm (Dempster et al., 1977) in a maximum likelihood context. Thus, we define the loglikelihood function as 2 log L = Σi Σt logΣk πk; f k lco2it jβk ; σk ð5Þ which can usually not be maximized directly. The EM algorithm maximize Eq. (5) with respect to ψ via an iterative procedure that first estimates the posterior class probabilities for each observation h i 2 2 wik = πk; Πt f k lco2it jβk ; σk Σk πk; Πt f k lco2it jβk ; σk = ð6Þ It then derives the prior class probabilities as πk = Σi wik = N ð7Þ by maximizing the log likelihood for each component separately using the posterior probabilities as weights 2 2 max Σi Σt wik log f k lco2it jβk ; σk ; w:r:t βk ; σk ð8Þ They are weighted sums of equations for an ordinary linear regression model. These steps are alternated repeatedly until the log likelihood changes by an arbitrarily small amount. For fixed K we retained the model with the best maximized log likelihood value. Once the algorithm has reached its end for a given K, we can proceed assuming K = K + 1 and proceed to parameter estimates for this value of the number of components. After that, a formal comparison could be done using penalized likelihood criteria (such as AIC or BIC) or by employing a formal likelihood ratio test. The proposed approach allows classification of countries on the basis of the posterior probabilities estimates wik, which represent a potentially useful by-product of the adopted approach. According to a simple maximum a posteriori rule, the i-th country can in fact be classified in the k-th component if wik = max(wi1,…wiK). It is worth noting that each component is characterized by homoge- 1349 neous values of estimated latent effects; i.e., conditional on the observed covariates countries from that group show a similar structure, at least in the steady state. The latent variables should capture the effect of missing covariates such as those related to institutions. Further, by defining a dynamic model we are able to provide an adequate association structure distinguishing between true and apparent association (Aitkin and Alfò, 1998). In the former case actual and future observations are directly influenced by past values, which cause a substantial change over time in the corresponding distribution. The latter case arises when observations are drawn from heterogeneous populations (as in LC models). A final remark on this point concerns that the static LC model may produce a misleading finding, since the unobserved but persistent heterogeneity can be interpreted as due to a strong serial dependence. 4.3. Main Results Before estimating the econometric models, we test whether the datasets are stationary. If this condition is not met, results could be showing spurious relationships. Two different panel-based unit root tests are used: the Levin–Lin-Chu ADF (Levin et al., 2002) and the PPFisher (Maddala and Wu, 1999; Choi, 2001) tests. Both examine the null of a unit root, but the former examines the null of a common unit root for all cross-sectional units, whereas the later examines the null of individual unit roots. The results of both unit root tests are reported in Table 1 and indicate rejection of the null hypothesis. Hence, since all the variables are stationary in levels we proceed with the panel analysis. Eq. (3) was first estimated for the whole set of countries under analysis. Table 2 shows the main results obtained by using different estimation methods. The model was first estimated using a dynamic model4 with fixed effects and clustered standard errors5 (Model 1). The results indicate that almost all the variables included are statistically significant and show, in general, the expected signs. The exception is the quadratic term of income per capita. The coefficient is non-significant indicating that we cannot confirm the EKC hypothesis for developing countries. By introducing dynamics into the model specification we are able to calculate short and long run elasticities. The main problem that we have to correct for the endogeneity bias affecting the lagged dependent variable remains. Although this bias can be low for panels with a large time dimension (it is of order 1/T, T being the number of time periods), it is still important to correct the estimates for the bias especially when the interest lies in the estimation of long run elaticities. The recent econometric literature has suggested two ways to correct for this bias. A way is to use the bias-corrected least squares dummy variable estimator (LSDV) proposed by Kiviet (1995) and extended by Bun and Kiviet (2003) and Bruno (2005) for unbalanced panels. This corrected estimator works remarkably well in terms of bias reduction while maintaining the high degree of efficiency of the uncorrected LSDV estimator. The results are reported in Model 2 (Table 2) and are in line with those obtained in the first column. Alternative dynamic panel data estimators are instrumental variables 4 A dynamic model is used as a means of dealing with autocorrelation, which was present when a static model was initially estimated. We would like to thank a referee making this suggestion. 5 The result of the Hausman test indicates that the country effects are correlated with the residuals and therefore the random-effect estimates are inconsistent, only the within-fixed-effects estimates are consistent. Since the country and time-specific effects are statistically significant (as indicated by the respective LM tests) the OLS estimates with a common intercept are biases and therefore not reported. To account for the presence of heteroskedasticity, the error structure is assumed to be heteroskedastic between the groups (panels) and it is estimated using clustered standard errors, sometimes called panel corrected standard errors. 1350 I. Martínez-Zarzoso, A. Maruotti / Ecological Economics 70 (2011) 1344–1353 Table 3 Estimation results by country group (1975–2003). Estimate Std. Error Table 4 Country grouping. z Long run elasticities Comp.1 Lco2(− 1) lyh lp lpup lpup2 lei lia Turning point urb. 0.963 0.031 0.040 0.445 −0.062 −0.020 −0.015 36% 0.009 0.013 0.009 0.056 0.010 0.013 0.021 106.761*** 2.297** 4.352*** 7.923*** −6.280*** −1.478 −0.734 0.818 1.080 11.900 −1.663 −0.523 −0.405 Comp.2 Lco2(− 1) lyh lp lpup lpup2 lei lia 0.966 0.061 0.039 0.037 −0.008 0.002 0.036 0.010 0.014 0.013 0.197 0.028 0.012 0.019 96.779*** 4.394*** 3.041*** 0.190 −0.294 0.175 1.918* 1.793 1.096 1.139 −0.244 0.063 1.049 Comp.3 Lco2(− 1) lyh lp lpup lpup2 lei lia Turning point urb. 0.760 0.419 0.268 0.801 −0.108 −0.247 0.116 41% 0.029 0.071 0.042 0.276 0.044 0.084 0.050 26.446*** 5.862*** 6.354*** 2.902*** −2.452** −2.931*** 2.307** 1.747 1.117 3.342 −0.450 −1.028 0.482 K 2 3 4 5 6 logLik 1279.904 1424.36 1500.952 1549.978 1605.462 AIC BIC ICL −2413.81 −2628.72 −2707.9 −2731.96 −2768.93 −2008.73 −2018.32 −1892.19 −1710.92 −1542.58 −2007.58 −2014 −1889.57 −1708.07 −1540.29 Note: K denotes the number of country groups evaluated. AIC, BIC and ICL denote respectively Akaike Information Criterion, Bayesian Information Criterion and Integrated Completed Likelihood. *, **, *** denote significance at the 10, 5, and 1% level, respectively. and GMM estimators. An advantage is that in this setting we can also test for the endogeneity of other variables such as income or urbanization and correct for heteroskedasticity. In cases with small T and large N, the GMM estimators are less biased than the LSDV although relatively inefficient. For moderate T and N it is recommendable to restrict the number of instruments used. Models 3 to 5 present the results of a GMM estimator with the variables in levels and country fixed effects, using as instruments for the lagged dependent variable its own second and third lag. The final model presents the differenced-GMM estimator of Arellano and Bond (1991). The GMM-system proposed by Blundell and Bond (1998) was also estimated but did not pass the specification tests. The results obtained using alternative methods are relatively robust indicating that all the variables included are statistically significant and show, in general, the expected signs. The significance of additional demographic variables is tested in Models 4 and 5. In Model 4 we include population density instead of population as a regressor and the results concerning urbanization are robust to the inclusion of this variable. Moreover, in Model 5 we additionally look at the age composition of population. We add two variables, namely the percentage of population that is between 14 and 64 and the percentage of population that is over 65 years old. Adding the age composition hardly affects the urbanization elasticity. Neither the affluence nor the technology variables are much affected in this or consecutive estimations and are therefore not discussed further. A higher percentage of the age group between 14 and 64 years old has a positive impact on emissions that is not significant at the 5% level. A higher share of elderly people also has a positive but smaller impact on emissions that is also N Group 1 Group 2 Group 3 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 Argentina Bangladesh Belarus Brazil China Colombia Croatia Czech Republic Egypt, Arab Rep. El Salvador Hungary India Jamaica Macedonia Morocco Nicaragua Pakistan Peru Poland Russian Federation Slovak Republic South Africa Syrian Arab Republic Thailand Tunisia Turkey Uzbekistan Armenia Azerbaijan Bolivia Botswana Bulgaria Chile Congo, Dem. Rep. Costa Rica Dominican Republic Estonia Ghana Guatemala Honduras Indonesia Iran Jordan Kazakhstan Kenya Latvia Lebanon Lithuania Malaysia Mexico Moldova Mozambique Nigeria Oman Panama Paraguay Philippines Romania Senegal Sri Lanka Sudan Tanzania Trinidad & Tobago Turkmenistan Ukraine Uruguay Venezuela Vietnam Yemen Zambia Zimbabwe Albania Algeria Angola Benin Cameroon Congo, Rep. Cote d'Ivoire Ecuador Ethiopia Gabon Georgia Haiti Kyrgyz Republic Namibia Nepal Tajikistan Togo not significant at the 5% level. Model 4 is the preferred model in terms of root mean squared error. Considering that the performance of Models 3 and 4 is very similar in terms of RMSE and R2, we have chosen instead to interpret the results obtained in Model 3. In this way we can compare our results with those obtained previously in the literature which considers population instead of population density. In the short run the population elasticity is lower than one and lower than the income elasticity, indicating that in the short term income growth contributes more to increase emissions than population growth. We find a non-linear relationship between urbanization and CO2 emissions that is in accordance with the modernization theory. Similarly, we have tested for non-linear relationships of the income variable, but have not found evidence confirming the Kuznets-curvehypothesis. An increase in energy efficiency decreases emissions almost proportionally. Finally, the effect of the percentage of industrial activity is positive and small, and the time effects show a negative sign and an increasing magnitude over time; this could be indicative of global technical progress over time that is reducing emissions. As an additional robustness check we control for endogeneity of the urbanization variable to consider the possibility of an inverse relationship between urbanization and pollution. We estimate the model using two stage least squares6 and use as instruments for the 6 The STATA command xtivreg2 and xtabond2 were used for the estimation. I. Martínez-Zarzoso, A. Maruotti / Ecological Economics 70 (2011) 1344–1353 Comp 1_UM Com 2_MUL Comp 3_ML 30 20 10 0 1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 -10 -20 -30 -40 Note: Estimation based on the results shown in Table 3. Fig. 3. Time effects for different groups. urbanization variable the first two lagged values of it in levels (Model 3 in Table 2). We also test for endogeneity by using a Hausman-type endogeneity test, which under the null hypothesis of exogeneity is distributed as a χ2 with degrees of freedom equal to the number of regressors tested. The results of the test and the associated probabilities shown in the last row of Table 2 (Model 3) indicate acceptance of the null hypothesis. Hence, urbanization can be treated as exogenous in the estimated model. To explore further the possibility of heterogeneous effects and the changing role of the variables explaining emissions across countries, a finite mixture model is estimated. As already mentioned in the previous section, this model overcomes the problems due to omitted variables and the possible correlation among country observations. Additionally it provides us with an endogenous classification of countries into homogeneous groups. The obtained posterior probabilities allow us to divide our sample into three groups of countries. We do this according to two model selection criteria: the Bayesian Information Criterion (BIC) and the Integrated Completed Likelihood (ICL).7 The first group contains 27 countries, the second 44 and the third 17 (Table 4). Countries in the first group are mainly upper-middle and middle-low income countries according to the World Bank classification and are characterized by showing a more than proportional long run elasticity of population with respect to emissions and lower income elasticity. In those countries urbanization is inversely (Ushaped) related with CO2 emissions, whereas energy efficiency and the percentage of industrial activity play no role in explaining the response variable. The second group is the most numerous and contains countries in all stages of development that are characterized as having a very high 7 The BIC picks the candidate model with the highest probability given the data. It is similar to the AIC but with a more severe penalty for complexity and it is consistent for the number of components (Keribin, 1998). It is known that BIC does not underestimate the number of components asymptotically (Leroux, 1992), indeed BIC may overestimate the number of components when components are not well separated. For this reason, we also considered ICL as an alternative. Furthermore, in a range of applications of finite mixture models, model choice based on BIC has given good results. We also reported the AIC values in Table 3. AIC is not strongly consistent, though it is efficient (Claeskens and Hjort, 2008). Unfortunately, in this particular application AIC does not provide any evidence of a specific mixture. The values decrease for increasing number of components and, hence, in view of the interpretability of the results, the BIC and the ICL are considered as model selection criteria. 1351 long run elasticity with respect to income (1.79) and an almost proportional impact of population growth on emissions. Also the percentage of industrial activity contributes to increase emissions, but urbanization and energy efficient are not statistically significant. Finally, countries in the third group are middle-low and low income countries8 for which all explanatory factors considered play a role — especially income and population but also energy efficiency, the percentage of industrial activity and urbanization. Similar as for group 1, urbanization presents an inverse U-shaped relationship with co2. Emissions increase up to a turning point which for this group is 41% of urbanization. To summarize, we confirm the modernization theory for countries in groups 1 and 3, but not for countries in the second group. With respect to the EKC hypothesis we also considered the inclusion of a squared income term as an explanatory variable. It was negatively signed, but not statistically significant. It was therefore excluded from the model. Fig. 3 presents the time effects of the three groups of countries. We observe an overall slightly decreasing trend in the magnitude of the estimated coefficients for the three groups over the whole period. For the first and third component however, most of the year dummies are not statistically significant. Assuming that these effects can represent specific technical progress over time common to all countries, the results indicate that technical progress has contributed to the decrease in CO2 emissions, especially in developing countries in the second group. To sum up, the environmental impact caused by population, urbanization, and affluence variables (scale effect) seems to be heterogeneous across countries and this heterogeneity does not correspond to different categories of income. Other factors are responsible for the different CO2 emissions paths followed by different countries and should be a matter of further research. The differential impact that we have found in this paper should be taken into account in future climate change negotiations and to design appropriate mitigation policies. 5. Conclusions In this paper a multivariate analysis of the determinants of carbon dioxide emissions in developing countries during the period 1975 to 2003 has been conducted. We have taken the STIRPAT formulation, the EKC hypothesis and the modernization theories as our theoretical framework. In the first model population is introduced as a predictor together with affluence per capita and the level of environmentally damaging technology (proxied for by the weight of the industrial sector in the GDP and with energy intensity). Affluence is measured by the GDP per capita in PPP. We have added urbanization as a predictor and used several estimation methods in a dynamic paneldata framework. The results show different patterns for three groups of countries. For the first and third sets of countries the elasticity emissionurbanization is positive for low and negative for high urbanization levels. In the second group urbanization is not statistically significant. This result has a very important policy implication: for some countries once urbanization reaches a certain level, the effect on emissions turns out to be negative, contributing to reduced environmental damage. We obtained some evidence confirming the ecological modernization theory, developed by sociologists, predicting that environmental impacts may follow a Kuznets curve relative to urbanization. However, we did not find robust evidence of an EKC with respect to income per capita, rejecting therefore the EKC hypothesis for developing countries. 8 According to the World Bank classification (Table A.1 in the Appendix A). 1352 I. Martínez-Zarzoso, A. Maruotti / Ecological Economics 70 (2011) 1344–1353 Appendix A Table A.1 Lists of countries classified by income group. Source: World Development Indicators 2007. Nobs denotes de number of observations per country. Low-income Nobs Lower-middle-income Nobs Upper-middle-income Nobs Bangladesh Benin Congo, Dem. Rep. Cote d'Ivoire Ethiopia Ghana Haiti India Kenya Kyrgyz Republic Mozambique Nepal Nigeria Pakistan Senegal Sudan Tajikistan Tanzania Togo Uzbekistan Vietnam Yemen, Rep. Zambia Zimbabwe 24 29 29 29 23 29 10 29 29 12 24 29 29 29 29 21 12 14 29 12 19 14 29 29 Albania Algeria Angola Armenia Azerbaijan Belarus Bolivia Brazil Bulgaria Cameroon China Colombia Congo, Rep. Ecuador Egypt, Arab Rep. El Salvador Georgia Guatemala Honduras Indonesia Iran, Islamic Rep. Jamaica Jordan Kazakhstan Macedonia, FYR Moldova Morocco Namibia Nicaragua Paraguay Peru Philippines Sri Lanka Syrian Arab Republic Thailand Tunisia Turkmenistan Ukraine Ukraine 24 29 19 14 14 12 29 29 24 28 29 29 29 29 29 14 12 29 29 29 29 11 29 12 12 12 29 13 10 29 23 29 29 19 29 29 24 12 13 Argentina Botswana Chile Costa Rica Croatia Czech Republic Dominican Rep Estonia Gabon Hungary Latvia Lebanon Lithuania Malaysia Mexico Oman Panama Poland Romania Russian Federation Slovak Republic South Africa Trinidad and Tobago Turkey Uruguay Venezuela, RB 29 23 29 29 12 14 29 12 29 24 12 10 12 29 29 29 24 14 16 12 19 29 20 29 21 29 Table A.2 Summary statistics and correlations. Variable Obs Mean Std. dev. Min Max lco2 lyh lp lp1564 lp65 lpd pup lpup lei lia 4142 3353 4258 4080 4080 4200 4254 4254 2122 3293 8.411 7.673 15.358 4.028 16.998 3.737 41.626 3.578 14.966 3.255 2.573 0.875 1.982 0.103 1.887 1.335 20.330 0.600 0.609 0.461 1.298 5.393 9.888 3.834 12.348 −0.079 3.200 1.163 12.981 0.632 15.237 9.777 20.977 4.259 22.967 6.956 92.480 4.527 16.315 4.488 Correlations lco2 lyh lp lp1564 lp65 lpd lpup lei1 lia lco2 lyh lp lp1564 lp65 lpd lpup lei lia 1 0.421 0.686 0.514 0.778 0.239 0.312 −0.032 0.435 1 −0.189 0.658 0.001 −0.048 0.677 0.502 0.447 1 0.103 0.945 0.356 −0.183 −0.046 −0.027 1 0.373 0.340 0.380 0.191 0.294 1 0.419 −0.045 −0.024 0.046 1 −0.274 0.071 −0.223 1 0.333 0.408 1 −0.017 1 I. Martínez-Zarzoso, A. Maruotti / Ecological Economics 70 (2011) 1344–1353 References Aitkin, M., Alfò, M., 1998. Regression models for binary longitudinal responses. Statistics and Computing. 8 (4), 289–307. Alfò, M., Trovato, G., Waldmann, R., 2008. Testing for country heterogeneity in growth models using a finite mixture approach. Journal of Applied Econometrics 23, 487–514. Andreoni, J., Levinson, A., 2001. The simple analytics of the environmental Kuznets curve. Journal of Public Economics 80 (2), 269–286. Arellano, M., Bond, S., 1991. Some tests of specification for panel data: Monte Carlo evidence and application to employment equations. Review of Economic Studies 58, 227–297. Blundell, R.W., Bond, S.R., 1998. Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics 87, 115–143. Borghesi, S., Vercelli, A., 2003. Sustainable globalisation. Ecological Economics 44, 77–89. Bruno, G.S.F., 2005. Approximating the bias of the LSDV estimator for dynamic unbalanced panel data models. Economics Letters 87, 361–366. Bun, M.J.G., Kiviet, J.F., 2003. On the diminishing returns of higher order terms in asymptotic expansions of bias. Economics Letters 79, 145–152. Choi, I., 2001. Unit root tests for panel data. Journal of International Money and Finance 20, 249–272. Claeskens, G., Hjort, N.L., 2008. Model Selection and Model Averaging. Cambridge University Press, Cambridge, U.K. Cole, M.A., Neumayer, E., 2004. Examining the impact of demographic factors on air pollution. Population and Development Review 2 (1), 5–21. Cole, M.A., Rayner, A.J., Bates, J.M., 1997. The Environmental Kuznets Curve: an empirical analysis. Environmental and Development Economics 2 (4), 401–416. Cramer, C.J., 1998. Population growth and air quality in California. Demography 35 (1), 45–56. Cramer, C.J., 2002. Population growth and local air pollution: methods, models and results. In: Lutz, W., Prkawetz, A., Sanderson, W.C. (Eds.), Population and Environment. : Supplement to Population and Development Review, 28. Population Council, New York, pp. 53–88. Cramer, C.J., Cheney, R.P., 2000. Lost in the ozone: population growth and ozone in California. Population and Environment 21 (3), 315–337. Daily, G.C., Ehrlich, P.R., 1992. Population, sustainability and earth's carrying capacity. Biosciences 42, 761–771. Dempster, A., Laird, N., Rubin, D., 1977. Maximum likelihood from incomplete data via the EM-algorithm. Journal of the Royal Statistical Society, B 39, 1–38. DeSarbo, W.S., Cron, W.L., 1988. A maximum likelihood methodology for clusterwise linear regression. Journal of Classification 5, 249–282. Dietz, T., Rosa, E.A., 1994. Rethinking the environmental impact of population, affluence and technology. Human Ecology Review 1, 277–300. Dietz, T., Rosa, E.A., 1997. Effects of population and affluence on CO2 emissions. Proceedings of the National Academy of Sciences USA 94 (1), 175–179. Dinda, S., 2004. Environmental Kuznets curve hypothesis: a survey. Ecological Economics 49, 431–455. Ehrhardt-Martinez, K., 1998. Social Determinants of Deforestation in Developing Countries: A Cross-National Study. Social Forces 77 (2), 567–586. Ehrhardt-Martinez, K., Crenshaw, E.M., Craig Jenkins, J., 2002. Deforestation and the environmental Kuznets Curve: a cross-national investigation of intervening mechanisms. Social Science Quarterly 83 (1), 226–243. Ehrlich, P.R., Holdren, J.P., 1971. Impact of population growth. Science 171, 1212–1217. Fan, Y., Lui, L.-C., Wu, G., Wie, Y.-M., 2006. Analyzing impact factors of CO2 emissions using the STIRPAT model. Environmental Impact Assessment Review 26 (4), 377–395. Intergovernmental Panel on Climate Change, 2007. Working Group III Report: Mitigation of Climate Change. http://www.ipcc.ch/ipccreports/Ar4-Wg3 2007. 1353 Jones, D.W., 1991. How urbanization affects energy-use in developing countries. Energy Policy 19 (7), 621–630. Keribin, C., 1998. Consistent estimate of the order of mixture models. Comptes Rendues de l'Academie des Sciences, Serie I-Mathematiques 326, 243–248. Kiviet, J.F., 1995. On bias, inconsistency and efficiency of various estimators in dynamic panel data models. Journal of Econometrics 68, 53–78. Leroux, B., 1992. Consistent estimation of a mixing distribution. The Annals of Statistics 20, 1350–1360. Levin, A., Lin, C.F., Chu, C., 2002. Unit root tests in panel data: asymptotic and finitesample properties. Journal of Econometrics 108, 1–24. Liddle, B., Lung, S., 2010. Age-structure, urbanization, and climate change in developing countries: revisiting STIRPAT for disaggregated population and consumptionrelated environmental impacts. Population Environment 31, 317–343. Maddala, G.S., Wu, S., 1999. A comparative study of unit root tests with panel data and a new simple test. Oxford Bulletin of Economics and Statistics 61, 631–652. Martínez-Zarzoso, I., Bengochea-Morancho, A., Morales-Lage, R., 2007. The impact of population on CO2 emissions: evidence from European countries. Environmental and Resource Economics 38, 497–512. Panayotou, T., Peterson, A., Sachs, J., 2000. Is the Environmental Kuznets Curve driven by structural change? What extended time series may imply for developing countries? CAER II Discussion Paper 80. Parikh, J., Shukla, V., 1995. Urbanization, energy use and greenhouse effects in economic development: results from a cross-national study of developing countries. Global Environmental Change 5 (2), 87–103. Perman, R., Stern, D.I., 2003. Evidence from panel unit root and cointegration tests that the Environmental Kuznets Curve does not exist. Australian Journal Agricultural and Resource Economics 47, 325–347. Shi, A., 2003. The impact of population pressure on global carbon dioxide emissions, 1975–1996: evidence from pooled cross-country data. Ecological Economics 44, 29–42. Stern, D.I., 1998. Progress on the environmental Kuznets Curve? Environment and Development Economics 3, 173–196. Stern, D.I., 2002. Explaining changes in global sulphur emissions: an econometric decomposition approach. Ecological Economics 42, 201–220. Stern, D.I., 2004. The rise and fall of the Environmental Kuznets Curve. World Development 32 (8), 1419–1439. UNFCCC, 1997. Kyoto Protocol to the United Nations Framework Convention on Climate Change (UNFCCC). FCCC/CP/1997/L.7/Add.1, Bonn. Vermunt, J.K., Magidson, J., 2002. Latent class cluster analysis. In: Hagenaars, J.A., McCutcheon, A.L. (Eds.), Applied Latent Class Analysis. Cambridge University Press, Cambridge, pp. 89–106. Wedel, M., DeSarbo, W.S., 1995. A mixture likelihood approach for generalized linear models. Journal of Classification 12, 21–55. Winkler, H., Spalding-Fecher, R., Mwakasonda, S., Davidson, O., 2002. Sustainable development policies and measures: starting from development to tackle climate change. In: Baumert, K., Blanchard, O., Llosa, S., Perkaus, J. (Eds.), Building a Climate of Trust: The Kyoto Protocol and Beyond. World Resources Institute, Washington D.C., pp. 61–87. World Bank, 2007. World Development Indicators 2001 CD-ROM, Washington, DC. York, R., 2007. Demographic trends and energy consumption in European Union Nations, 1960–2025. Social Science Research 36, 855–872. York, R., Rosa, E.A., Dietz, T., 2003. STIRPAT, IPAT and ImPACT: analytic tools for unpacking the driving forces of environmental impacts. Ecological Economics 46 (3), 351–365. Zaba, B., Clarke, J.I., 1994. Introduction: current directions in population–environment research. In: Zaba, B., Clarke, J.I. (Eds.), Environment and Population Change. Derouaux Ordina Editions, Liège.