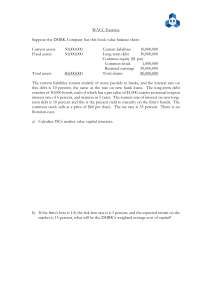

Banking & Regulation Econ 455/555 & MFIN455/55 Prof. Tanju Yorulmazer Lecture: Financial Intermediaries & Risks Financial intermediaries Questions • What do financial intermediaries do? – Intermediate between providers and users of financial capital • What are the risks they get exposed to? – Credit risk – Liquidity risk – Interest rate risk • How do they manage these risks? – Credit analysis – Risk management: Value at Risk, Expected Shortfall, Liquidity management… Financial Intermediary • An economic agent who specializes in intermediating between providers and users of financial capital. • One type of FI is a Commercial Bank (CB). CB granting loans and receiving deposits from the public: – The combination of lending and borrowing is typical of a CB – CBs provide unique services to the general public: – Channel funds from savers to investors – Liabilities act as money, payment and liquidity services Types of FI • FIs are divided into two groups broadly: – Deposit taking institutions: Commercial Banks – Non-depository institutions: – Venture Capitalists, Insurance Companies, Investment Funds, Pension and Mutual Funds, Hedge Funds, Investment Banks • In contrast with non-financial firms – FIs hold relatively large quantities of financial claims (contracts of the indebtedness of their clients) as assets – FIs tend to be more leveraged Types of bank assets Bank Assets Loans Commercial & Industrial Securities Consumer Cash Bank assets • Commercial and Industrial loans (C&I) – Transaction, working capital, term loans… • Consumer loans – Direct loans, credit cards, mortgages • Securities – Commercial paper, government securities... • Cash and reserves Lending • How do banks acquire loans? • Spot market • Originate and keep them on their own books • Purchase loans originated by other intermediaries • Forward market • Loan commitment: Promise to lend in the future Risks Financial Intermediaries Face Financial Intermediation • The balance sheet of a financial intermediary: Assets Liabilities Liquid/safe assets Short-term debt Illiquid/risky assets Long-term debt Equity • Banks hold risky/illiquid assets. • Credit risk: Banks can experience losses from the risky assets. • Capital acts as a buffer and can help prevent costly failures. Financial Intermediation • The balance sheet of a financial intermediary: Assets Liabilities Liquid/safe assets Short-term debt Illiquid/risky assets Long-term debt Equity • Banks hold risky/illiquid assets typically with long maturities. • Liabilities (short-term debt or deposits) usually have short maturity (maturity/liquidity mismatch). • Liquidity risk: When debt holders want to withdraw (or not rollover) bank needs to come up with cash. Costly liquidation. • Can lead to the failure of the bank. Financial Intermediation • The balance sheet of a financial intermediary: Assets Liabilities Liquid/safe assets Short-term debt Illiquid/risky assets Long-term debt Equity • Banks hold assets typically with long maturities. • Liabilities (short-term debt or deposits) usually have short maturity (maturity mismatch). • Interest rate risk: When interest rates change, it can expose the bank to interest rate risk. Risks • Credit Risk • Risk management: Credit analysis, Value-at-Risk (VaR) models • Capital regulation: Basel capital requirements • Liquidity Risk • Liquidity management • Liquidity regulation: Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR) • Interest Rate Risk A Simple Framework • Eisenbach, Keister, McAndrews and Yorulmazer (2014) Assets Liabilities Liquid/safe assets (m) Short-term debt (s) Illiquid/risky assets (y) Long-term debt (l) Equity (e) • Builds on the framework of Diamond & Dybvig (1983) (we will talk in detail) • Credit risk, solvency risk, illiquidity risk. A Simple Framework: Assets • Three dates t=0,1,2. • Assets: • Bank holds cash (m) and risky assets (y). • Risky assets have a random return of θ at t=2. • θ realized at t=1. • If liquidated at t=1, risky asset pays τθ < 1. • Bank holds cash m. • Cash has a gross return r1=1 (for simplicty) between t=0 and t=1. • Cash has a gross return rs between t=1 and t=2. A Simple Framework: Liabilities • Three dates t=0,1,2. • Liabilities: • Bank has short-term debt (s), long-term debt (l) and equity (e). • Long-term debt matures at t=2 and promises rl. • Short-term debt has the same promised return as cash (for simplicity). • Promises r1=1 between t=0 and t=1 and rs between t=1 and t=2. • Matures at t=1 and needs to be rolled over after observing θ. A Simple Framework: Solvency • Solvency: • If the bank can meet its debt obligations any remaining funds at t=2 are paid out to equity holders. • If the bank cannot meet its obligations, it enters bankruptcy. – A fraction φ of assets is lost to bankruptcy costs (lawyer fees). – Remaining assets distributed to debtholders on a pro-rata basis. – Bankruptcy costs are high so that a short-term debt holder will rollover if and only if the bank is solvent (very important!!!). A Simple Framework: Returns • Assume: rs < rl < 1/τ. • Long-term debt has a higher promised return than short-term debt. • Liquidating the risky asset is very costly. • Neither form of finance dominates the other. • Assume: τθ < 1. • Risky asset does not dominate cash in terms of returns. A Simple Framework: Solvency • Solvency: • The bank is solvent if it can meet all its contractual obligations in both periods. • A fraction α of short-term creditors do not rollover. • Solvency depends on: • Return from assets θ (credit risk) • Fraction α of short-term creditors that do not rollover (liquidity risk). Solvency at t=1 and t=2 • Note that if the value of the assets at t=2 is negative, the bank is already insolvent at t=1. • In this case, the debt holders who withdraw at t=1 receive a pro-rata share share of the liquidation value in expectation. • Debt holders who do not withdraw receive nothing. • If the value of the assets at t=2 is positive, debt holders who withdraw at t=1 receive full payment. • In that case, the bank is solvent at t=2 if the value of the assets at t=2 is enough to pay the remaining debt. A Simple Framework • A fraction α of short-term creditors do not rollover. • Bank needs αs units of cash to pay short-term creditors at t=1. • Use cash first (αs<m) • Liquidate the risky asset only when cash is not enough (αs>m). • Liquidating the risky asset decreases bank value and can force the bank into insolvency. A Simple Framework: Value at t=2 • Case I: Bank has enough cash for withdrawals at t=1 • For αs ≤ m, the bank uses cash for payments at t=1. • The value of the assets at t=2 is given as: θy + rs (m − αs ) • Bank is solvent if: θy + rs (m − αs ) ≥ (1 − α )srs + lrl A Simple Framework: Solvency at t=2 • For αs ≤ m, the bank is solvent at t=2 if: θ≥ srs + lrl − mrs =θ y • Solvency threshold is independent of α. A Simple Framework: Value at t=2 • Case II: Bank does not have enough cash for withdrawals at t=1 • For αs > m, the bank needs to liquidate some of the risky asset: αs − m τθ • The value of the assets at t=2 is given as: θ y − αs − m τθ • The bank is solvent if: θ y − αs − m ≥ (1 − α )srs + lrl τθ A Simple Framework: Solvency at t=2 • For αs > m, the bank is solvent at t=2 if: θ y − αs − m ≥ (1 − α )srs + lrl τθ • Note that the solvency threshold θ* is increasing in α. Why? A Simple Framework: Solvency at t=2 • For α=1, we obtain: θ (1) = s + τlrl − m =θ τy • For θ ≥ θ the bank is always solvent (independent of α). A Simple Framework: Solvency at t=2 • For θ ≥ θ the bank is fundamentally solvent (independent of α). • For θ ≤ θ the bank is fundamentally insolvent (independent of α). • For θ ≤ θ < θ solvency depends on α: * • For θ (α ) ≥ θ (α ) the bank is conditionally solvent. • For θ (α ) < θ * (α ) the bank is conditionally insolvent. A Simple Framework • Insolvency, illiquidity θ Fundamentally solvent 𝜃̅ Conditionally solvent 𝜃∗ Conditionally insolvent 𝜃 Fundamentally insolvent 𝑚 𝑠 1 α Determinants of stability • Leverage/capital (e). • Liquidation value (τ). • Maturity structure of debt (s versus l). • Liquidity holdings (m). A Simple Framework • Liquidation values (effect of τ) θ 𝜃̅ 𝜃 ∗ (𝛼|𝜏low ) 𝜃̅(𝜏) 𝜃 ∗ (𝛼|𝜏) 𝜃 𝑚 𝑠 𝜃 ∗ (𝛼|𝜏max ) 1 α Going forward • Risk management (θ). • Liquidity management (m,s,τ,α). • Regulation: • Capital (e) • Liquidity (m,s,τ)