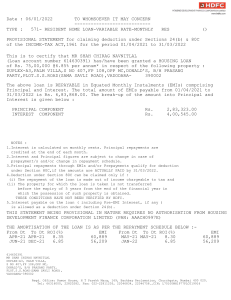

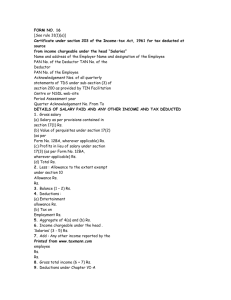

Tax exemptions & deductions for Financial Year 2023-24 (as a comparison to FY 2022-23) Section 10(13A) Component House rent allowance Description Least of the below is exempt for Income Tax: 1. Actual HRA earned by the Assessee for the year 2. Rent paid minus 10% of basic salary 3. 40% of the basic or 50% of the basic (in case of metro cities) Old Regime benefit New Regime benefit Allowed Not allowed Remarks No Change Section Components Description • • 24 Loss from Selfoccupied property • • Interest on borrowed capital is allowed up to INR 2,00,000/- and no other deduction is allowed. After construction or purchase of a residential property is completed, the acquisition or construction of the house should be completed within three years from the end of the financial year in which the loan was sanctioned. However 1/5th of pre-construction interest can be added to the current year’s interest payment. In any case the maximum interest to be claimed in a given year can’t exceed INR 2,00,000/-. If capital is borrowed for repairs/renewal/reconstruction then the maximum amount of deduction is restricted to INR 30,000/-. Old regime New regime Remarks benefit benefit Allowed Not Allowed No change Allowed Not Allowed No change Limited to INR 50,000/- subject to fulfillment of all the required criteria as per IT guidelines. 80EE • Additional tax benefit on home loan • availed in FY 2016-17 • • Value of the house should be INR 50 lakhs or less. The loan taken for the house must be INR 35 lakhs or less. The loan must be sanctioned by a Financial Institution or a Housing Finance Company. The loan must be sanctioned between 1 April 2016 – 31 March 2017. As on the date of the sanction of loan, no other house property must be owned by you. Section Components Additional tax 80EEA benefit on home loan availed in FY 2019-20 Loss from Let Out Property 24 Description Old regime New regime Remarks benefit benefit Limited to INR 1, 50,000/- fulfillment of all the required criteria as per IT guidelines. • Housing loan must be taken from a financial institution or a housing finance company for buying a residential property. • Stamp duty value of the house property should be INR 45 lakhs or less. Allowed • The individual taxpayer should not be eligible to claim benefit under the existing Section 80EE. • The taxpayer should be a first-time home buyer. The taxpayer should not own any residential house property as on the date of sanction of the loan. Not Allowed Interest benefit Capped to a maximum of INR 2,00,000/- only i.e. total amount allowed for a property (Self and let-out both together) is INR 2,00,000/ Allowed *Available under special No Change conditions ONLY Allowed Allowed Standard Deduction on To arrive at the loss from let out property, a standard deduction of 30% is income from rented out allowed from the rental income as municipal taxes. property No Change Changed *Loss from any of the let-out house property can be claimed to the extent of and get adjusted against the income arrived from such property/ies ONLY. Any balance of loss left cannot be claimed under any section or get adjusted against any other head of income. Section Component 80D Medical Insurance Description • • INR 25,000 benefit - In case of Individual, Spouse & Children. Additional benefit of INR 25,000/- in case of parents below 65 years and INR 50,000 in case of parents above 65 years (Senior citizens). spent on treatment of handicapped dependents (spouse, children, Medical treatment for Amount parents, dependent brothers & sisters) 80DD handicapped • Limited to INR 75,000 (<=80% disability) dependent • INR 1.25 lakh (>80% disability) Expenditure must be actually incurred by resident assessee on himself or Medical treatment for dependants (spouse, children, parents, dependent brothers & sisters) for medical 80DDB treatment of specified disease or ailment. The diseases have been specified in specified disease Rule HDD. • 80E Interest on education • loan • Donations to certain 80G funds, charitable institution etc. Interest paid for the first 8 years on loans taken for higher education such as engineering/medical etc. Eligible if loan is availed by the employee for self spouse & children for pursuing higher education. Loans availed from financial institution/bank only, are eligible. The various donations specified in Section 80G are eligible for deduction up to either 100% or 50% with or without restriction as provided in Section 80G. Old regime New regime benefit benefit Allowed Not allowed Allowed Not allowed Allowed Not allowed Allowed Not allowed Allowed Not allowed Remarks No change No change No change No change No change Section 80U Component Permanent physical disability including blindness 80CCD Additional NPS 1B contribution Tax benefit for interest paid on the 80EEB Electric vehicle (EV) loan availed in FY 2019-23 Description • • Limited to INR 75,000 (<=80% disability) INR 1.25 lakh (>80% disability) Amount invested in National Pension Scheme will be considered up to INR 50,000 only if the limit available under Section 80C is exhausted. • • • • Loan must be taken from a financial institution or a non-banking financial company for buying an electric vehicle. Loan should be sanctioned anytime between 1 April 2019 - 31 March 2023. Limited to INR 1,50,000 An electric vehicle is one that runs solely on an electric motor whose traction energy is provided by a battery that is installed inside the vehicle. It also has an electric regenerative braking system that, when applied, transforms the kinetic energy of the vehicle into electrical energy. in pension funds is eligible for tax deduction from your income. The tax Policy - Investment exemption available under 80CCC is limited to the overall allowed amount under 80C i.e., 80CCC Pension 80CCC INR 1,50,000 Old regime New regime Remarks benefit benefit Allowed Not allowed No change Allowed Not allowed No change Allowed Not allowed No change Allowed Not allowed No change Section Component Description • Provident Fund (PF) is deducted from your salary. Both employee & employer contribute to it. While employer’s contribution is exempt from tax, your contribution (i.e., employee’s contribution) is considered under section 80C. Old Regime New Regime benefit benefit Allowed Not allowed No change Allowed Not allowed No change Allowed Not allowed No change Remarks 80C Provident Fund (PF) • 80C Voluntary Provident Employees who have opted for VPF can claim this amount under 80C within the limit of INR 1,50,000. Fund (VPF) 80C Life Insurance Corpoartion of India (LIC) 80C Public Provident Fund (PPF) Amount invested in PPF for self, spouse, children's in current FY can be claimed under section 80C Allowed Not allowed No change 80C National Savings Certificate (NSC) Amount invested in NSC in current FY is eligible for Section 80C deduction. The interest accrued every year is liable to tax (i.e., to be included in your taxable income) but the interest is also deemed to be reinvested and thus eligible for Section 80C deduction. Allowed Not allowed No change • • Life Insurance premiums paid for self, spouse, children in current FY can also be included in Section 80C deduction. Premium paid by you for your parents (father/mother/both) or your in-laws is not eligible. Section Component Description Old Regime New Regime benefit benefit Allowed Not allowed No change Allowed Not allowed No change Remarks • 80C Infrastructure Bonds (I-Bonds) 80C Tution Fees (TF) Tuition Fees paid for up to two children is eligible for deduction u/s 80C. 80C There are some mutual fund schemes specially created for offering you tax savings, and these are called Equity Linked Savings Scheme, or ELSS. The Mutual Fund (MF) investments that you make in ELSS are eligible for deduction under Section 80C. Allowed Not allowed No change 80C Equity Linked Savings Scheme/ Mutual Funds (ELSS/ MF) Allowed Not allowed No change • These bonds are issued by infrastructure companies, and not the government. The amount that you invest in these bonds can also be included in Section 80C deductions. Amount invested in current FY offering tax benefits under Section 80C. Section Component Description Old regime New regime benefit benefit Remarks 80C Unit Linked Insurance Plan ULIP should be taken on your own, spouse or any child's life in current FY. (ULIP) Allowed Not allowed No change 80C Sukanya Samriddhi Scheme An individual can open Sukanya Samriddhi Scheme account in his/ her daughter's name. One can get the benefit u/s 80C. Allowed Not allowed No change 80C 5-year bank Fixed Deposits (FDs) Tax-saving fixed deposits (FDs) of scheduled banks with tenure of 5 years are also entitled for Section 80C benefit. Allowed Not allowed No change 80C Senior Citizen Savings Amount invested in Senior Citizen Savings Scheme 2004 (SCSS) is eligible under Scheme 2004 (SCSS) section 80C. Interest income is taxable. Allowed Not allowed No change 80C 5-year Post Office invested in the five-year POTD only qualifies for tax saving under Section Time Deposit (POTD) Amount 80C. The interest is entirely taxable. scheme Allowed Not allowed No change 80C NABARD rural bonds Amount invested in NABARD Rural Bonds only qualify under Section 80C. Allowed Not allowed No change Section Component Description Old regime New regime benefit benefit Remarks 80C Interest on NSC NSC interest is taxable under the head “Other Income”. Allowed Not allowed No change 80C Stamp duty & registration charges on house property The amount you pay as stamp duty when you buy a house, and the amount you pay for the registration of the documents of the house can be claimed as deduction under Section 80C in the year of purchase of the house. Allowed Not allowed No change 80C Home loan principal repayment The principal component of the EMI qualifies for deduction under Section 80C. The interest component can save you significant income tax under Section 24 of the Income Tax Act. Allowed Not allowed No change 80TTA Interest amount earned on savings bank account held with a banking institution/ Interest from savings post office can ONLY be claimed as a tax deduction upto maximum of INR 10, 000. Interest from fixed/time/recurring deposits is not allowed under account this section. Allowed Not allowed No change 80TTB Interest from deposit accounts (Senior citizens only) Individuals aged 60 years and above can claim interest amount earned on any kind of deposit account held with a banking institution/ post office ONLY, as a tax deduction upto maximum of INR 50, 000. Benefit under section 80TTA does not apply to such individuals. Allowed Not allowed No change