")

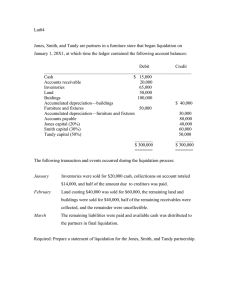

Partnership Liquidation (Lump-Sum) JENNIFER A. LAGDAAN Partnership Liquidation (Lump-Sum) Liquidation Partnership dissolution calling for the winding up of business affairs Partnership Liquidation (Lump-Sum) Liquidation Liquidated completely Partnership terminated or ended assets are sold, partnership creditors are paid, and the remaining assets are distributed as return of investment Partnership Liquidation (Lump-Sum) Liquidation Caused by any of the following: Accomplishment Termination of the purpose of term or period Bankruptcy Mutual agreement Partnership Liquidation (Lump-Sum) Liquidation Accounting problems involved: Determination of profit or loss Closing Correction Liquidation of accounting errors Partnership Liquidation (Lump-Sum) Liquidation Marshaling Right of assets of offset Partnership Liquidation (Lump-Sum) Liquidation Marshaling Order of assets of creditor’s rights against the partnership’s assets and the personal assets of the individual partners Partnership Liquidation (Lump-Sum) Liquidation Marshaling of assets Order of claims against the partnership’s assets: 1. Partnership creditors other than partners 2. Partner’s claims other than capital and profits 3. Partner’s claim to capital or profits Partnership Liquidation (Lump-Sum) Liquidation Marshaling Order of assets of claims against the personal assets: 1. personal creditors 2. partnership creditors Partnership Liquidation (Lump-Sum) Liquidation Right of offset Offsetting a deficit in a partner’s capital against the loan payable to that partner Partnership Liquidation (Lump-Sum) Definition of Terms Dissolution Winding up Termination Liquidation Realization Gain on realization Loss on realization Capital deficiency Deficient partner Right of offset Partner’s interest Partnership Liquidation (Lump-Sum) Types of Liquidation Lump-sum liquidation or liquidation by totals Liquidation liquidation by installment or piece-meal Partnership Liquidation (Lump-Sum) Procedures in Lump-sum Liquidation Sale of non-cash assets and distribution or allocation of gain or loss Distribution of cash to creditors and partners Partnership Liquidation (Lump-Sum) Cash can be distributed to partners before or after the elimination of the deficiency. If after… 1. 2. Capital deficiency is eliminated by a. Making additional cash investment, if solvent b. Charging the deficiency as additional loss, if insolvent Cash available for distribution is then paid to partners to apply first on loan then on capital * Final distribution of cash to partners is made based on partners’ capital balances and not on any ratio Partnership Liquidation (Lump-Sum) Cash can be distributed to partners before or after the elimination of the deficiency. If cash is distributed to partners before eliminating the deficiency: 1. Cash available is paid based on accompanying schedule 2. Deficient partners may (a) if solvent, make additional cash investment (b) if insolvent, shall be absorbed by the other partners Partnership Liquidation (Lump-Sum) Statement of Liquidation Shows the conversion of assets into cash, the allocation of gain or loss on realization, and the distribution of cash to creditors and partners Partnership Liquidation (Lump-Sum) Illustrative Problem The statement of financial position of the partnership of Enteng and Estrel as of December 31, 2020 is shown below. Enteng and estrel Statement of Financial Position December 31, 2020 Assets Liabilities and Equity Cash P40,000 Liabilities Other Assets 400,000 Enteng, Loan 36,000 Estrel, Loan 40,000 Enteng, Capital 80,000 Estrel, Capital 20,000 Total Assets P440,000 Total Liabilities & Equity P264,000 P440,000 Partnership Liquidation (Lump-Sum) Illustrative Problem The other assets were realized for P268,000, and cash was disbursed. Division of profits and losses are: Enteng Estrel Case 1 90% 10% Case 2 70% 30% Case 3 50% 50% Instructions: Prepare the partnership liquidation statement and journal entries to record the liquidation for each case. Partnership Liquidation (Lump-Sum) Illustrative Problem – Case 1 Enteng and Estrel Statement of Liquidation January 1 – 31, 2020 Balances before liquidation Sale of other assets & distribution of loss Cash Other Assets P 40,000 P 400,000 268,000 Balances P 308,000 Payment of liabilities (264,000) Balances P 44,000 Offset of loan against debit balance in the capital of Enteng Balances Liabilities P 264,000 Loans_______ Estrel Enteng P 36,000 P 40,000 Capital______ Enteng (90%) Estrel (10%) P 80,000 (400,000) (118,800) P 264,000 Additional loss to Estrel for the deficiency of Enteng Balances P 44,000 Payment to partners ( 44,000) ( 13,200) P 36,000 P 40,000 (P 38,800) P 6,800 P 36,000 P 40,000 (P 38,800) P 6,800 (264,000) ( 36,000) P 44,000 P 20,000 36,000 P 40,000 (P 2,800) 2,800 P 40,000 ( 40,000) P 6,800 ( 2,800) P 4,000 ( 4,000) Partnership Liquidation (Lump-Sum) Illustrative Problem – Case 1 1. Cash 268,000 Enteng, Capital 118,800 Estrel, Capital Liabilities Estrel, Capital Enteng, Capital 264,000 5. 264,000 Estrel, Loan Estrel, Capital Cash Enteng, Loan Enteng, Capital 2,800 400,000 Cash 3. 2,800 13,200 Other Assets 2. 4. 36,000 36,000 40,000 4,000 44,000 Partnership Liquidation (Lump-Sum) Illustrative Problem – Case 2 (70%, 30%) Balances before liquidation Sale of other assets and distribution of loss Cash Other Assets Liabilities P 40,000 P 400,000 P 264,000 268,000 Balances P 308,000 Payment of liabilities (264,000) Balances P 44,000 Offset of loan against debit balance in capital account Balances Payment to partners Enteng P 36,000 P 40,000 P 20,000 ( 92,400) ( 39,600) P 36,000 P 40,000 (P 12,400) (P 19,600) P 36,000 P 40,000 (P 12,400) (P 19,600) (400,000) P 264,000 ( 44,000) Capital______ Estrel P 80,000 ( 264,000) (12,400) P 44,000 Loans_______ Estrel Enteng ( 19,600) P 23,600 P 20,400 ( 23,600) ( 20,400) 12,400 19,600 Partnership Liquidation (Lump-Sum) Illustrative Problem – Case 2 (70%, 30%) 1. Cash 268,000 Enteng, Capital 92,400 Estrel, Capital 39,600 Other Assets 2. Liabilities Cash 3. 400,000 264,000 4. 264,000 Enteng, Loan 12,400 Estrel, Loan 19,600 Enteng, Capital 12,400 Estrel, Capital 19,600 Enteng, Loan 23,600 Estrel, Loan 20,400 Cash 44,000 Partnership Liquidation (Lump-Sum) Illustrative Problem – Case 3 (50%, 50%) Cash Balances before liquidation Sale of other assets & distribution of loss P 40,000 268,000 Balances P 308,000 Payment of liabilities (264,000) Balances Offset of loan against debit balance in the capital of Estrel Balances Other Assets P 400,000 Liabilities P 264,000 Enteng P 36,000 Loans_______ Estrel Enteng P 40,000 (400,000) P 264,000 P 80,000 Payment to partners P 20,000 ( 66,000) ( 66,000) P 36,000 P 40,000 P 14,000 (P 46,000) P 44,000 P 36,000 P 40,000 P 14,000 (P 46,000) P 44,000 P 36,000 P 14,000 40,000 P ( 6,000) ( 264,000) (40,000) Additional loss to Enteng for the deficiency of Estrel Balances Capital______ Estrel ( 6,000) P 44,000 ( 44,000) P 36,000 ( 36,000) P 8,000 ( 8,000) 6,000 Partnership Liquidation (Lump-Sum) Illustrative Problem – Case 3 (50%, 50%) 1. Cash 268,000 Enteng, Capital 66,000 Estrel, Capital 66,000 Other Assets 2. Liabilities 4, Enteng, Capital Estrel, Capital 264,000 5. 264,000 Enteng, Loan Enteng, Capital Cash Estrel, Loan Estrel, Capital 6,000 400,000 Cash 3. 6,000 40,000 40,000 36,000 8,000 44,000 Partnership Liquidation (Lump-Sum) Illustrative Problem Distribution of Cash to Partners Esguerra, Esteban, Estrada and Eugenio are partners with capitals of P11,000, P10,300, P13,700, and P9,000 respectively. Esguera has a loan balance of P2,000. Profits are shared in the ratio of 4:3:2:1 by Esguerra, Esteban, Estrada, and Eugenio respectively. Assets are sold, liabilities are paid and cash of P12,000 remains. Instructions: Show how the cash of P12,000 be distributed. Partnership Liquidation (Lump-Sum) Illustrative Problem Distribution of Cash to Partners (4:3:2:1) Esguerra Capital balances before liquidation P 11,000 Loan from partners Esteban P 13,700 P 9,000 P 13,700 P 9,000 2,000 P 13,000 P 10,300 Loss on realization (P46,000 – P12,000) ( 13,600) ( 10,200) Balances (P P Balances 600) 600 -------- Additional loss to partners Distribution of cash to partners Eugenio P 10,300 Total partners’ interest Additional loss to partners Estrada --------- 100 ( 300) (P ( 6,800) P 6,900 P 5,600 200) ( 100) 200) P 6,700 P 5,500 200 ( ( --------- ( ( 3,400) 133) P 6,567 67) P 5,433