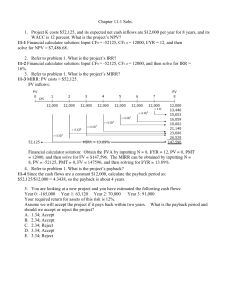

Accounting 403 – Capital Budgeting Name ____________________________________________ 1. Capital budgeting is concerned with a. Decisions affecting only capital-intensive Industries. b. Analysis of short-range decisions c. Analysis of long-range decisions d. Scheduling of office personnel in office buildings 2. Which of the following factors should be considered when evaluating a proposed capital investment? a. Amount of investment c. Cost of capital b. Annual returns d. All of the above 3. In computing the amount of initial investment for decision-making, taxes would be relevant for all of the following, except: a. Avoidable repairs of old asset b. Profit on sale of old asset replaced by a new one c. Loss on write-off of other assets disposed because of new capital Investment d. Increase in working capital required to support new capital investment 4. ABC Company is considering the sale of a machine with a book value of P 80,000 and 3 years remaining in its useful life. Straight-line depredation of P 25,000 annually is available. The machine has a current market value of P 100,000. What Is the cash flow from selling the machine if the tax rate is 40%? a. P 25,000 c. P 92,000 b. P 80,000 d. P 100,000 5. Old equipment with a book value of P 15,000 will be replaced by new equipment with a purchase price of P50,000, exclusive of freight charges of P 2,000. The market value of the old equipment is P 11,000. Repair costs of P 2;000 can be avoided if the new equipment is acquired, Assume a tax rate of 35%. What is the initial (net) investment of the project? a. P 33,800 c. P 39,700 b. P 38,300 d. P 52,000 6. The most convenient way to handle proceeds from the disposal of an old asset is to a. Treat it as a cash. flow c. Offset the amount against the cash outlay b. Treat it as a reduction in salvage value d. Add to the Investment 7. To approximate annual cash inflow, depredation Is a. Added back to net income because it is an inflow of cash b. Subtracted from net income because it is an outflow of cash c. Subtracted from net Income because it is an expense d. Added back to net income because it is not an outflow of cash 8. Annual cash inflows from the capital projects are measured in terms of a. Net income before depreciation and taxes b. Net income after depredation and taxes c. Net income before depredation and after taxes d. Net income after depredation and before taxes 9. A project costing P180,000 will produce the following annual cash benefits and salvage value: OLD Equipment NEW Equipment Revenue P150,000 P180,000 Cash operating costs 70,000 60,000 Annual depredation 30,000 50,000 Income tax, 46% What is the incremental annual cash income after taxes? a. P 30,000 c. P 40,000 b. P 30,800 d. P 38,000 10. DEF Inc.'s depreciation deduction last year was P 50,000 and its tax rate was 30%. The company's tax savings from the depredation tax shield for the year was a. P 15,000 c. P 50,000 b. P 35,000 d. P 30,000 11. Which statement describes the relevance of depredation In calculating cash flows? a. Depreciation Is relevant only when income taxes exist b. Depredation is always relevant c. Depredation is never relevant d. Depreciation is relevant only with discounted cash flow methods 12. XYZ Company is analyzing a capital investment proposal for a new machinery to produce a new product over the next 10 years. At the end of ten years, the machinery must be disposed of with a zero net book value but with a scrap salvage value of P 20,000. It will require some P 30,000 to remove the machinery. The applicable tax rate is 35%. The approximate “end-of-life” cash flow based on the foregoing information is: a. Inflow of P 30,000 c. Outflow of P 10,000 b. Outflow of P 6,500 d. Outflow of P 17,000 13. Cost of capital is a. The amount the company must pay for its plant assets b. The dividends a company must pay on its equity securities. c. The cost the company must incur to obtain its capital resources. d. The cost the company is charged by investment bankers who handle the issuance of equity or long-term debt securities. 14. For a certain project, the return that investors demand for investing in a firm is known as: a. DCF rate of return c. Payback b. Net present value d. Cost of capital 15. In an investment in plant asset, the return that should keep the market price of the firm stock unchanged is a. Net present value c. Adjusted rate of return b. Cost of capital d. Unadjusted return 16. All of the following refer to the discount rate used by a firm in capital budgeting except: a. Cost of capital c. Opportunity costs b. Required rate of return d. Hurdle rate 17. UVW Company has 5% preferred stock with a par value of P 100. Selling price is P 123.50 per share and flotation costs are P 0.50 per share. The company's tax rate is 20%. What is the cost of preferred stock? a. 4.03% c. 4.7% b. 4.07% d. 5% 18. DEF Company is attempting to compute the cost of Internal and external equity. The company's common stock is currently selling at P 62.50 per share with flotation cost of P5 per share. The next dividend per share is P 5.42, Earnings and dividends are expected to grow at a constant rate of 5%. What is the cost of new common stock and retained earnings? a. C/S: 13.67%; R/E: 13.67% c. C/S: 13.67%; R/E: 14.43% . b. C/S: 14.43%; R/E: 13.67% d. C/S: 14.43%; R/E:14.43% 19. The market value of GHI Company's common stock (book value: P 65M) is estimated at P 60 M and the market value of its interest bearing debt (book value: P35M) is estimated at P40M. The average before tax yield on these liabilities is 15% per year. Income taxes are 40%. The company is expected to pay dividend of P 10 per share and the stock Is selling at a price of P 100 per share. The growth rate of dividend is projected to be 2.5% per year. What is the weighted average cost of capital (WACC) of the company as a whole? a. 9% b. 21.5% b. 11.1% c. 25% 20. The weighted average cost of capital approach to decision making is not directly affected by the a. Value of common stock b. Current budget for expansion c. Cost of debt outstanding d. Proposed mix of debt, equity, and existing funds used to Implement the project 21. A company with cost of capital of 15% plans to finance an investment with debt that bears 10% interest. The rate it should use to discount the cash flows is a. 10% c. 25% b. 15% d. Some other rate. 22. Which of the following methods measures the recovery period of a proposed investment? a. Payback c. PV payback b. Bail-out payback d. All of given 23. The technique that does not use cash flow for capital investment decisions. a. Payback c. ARR b. NPV d. IRR 24. Which of the following cash flow methods of evaluating capital investment ignores the time value of money? a. IRR c. Discounted payback. b. NPV d. Payback reciprocal 25. ABC Company is considering a certain project with the following projected cash income after taxes for 4 years, the life of the project: End of year 1, P 11,000; year 2, P 9,000; year 3, P 8,000; year 4, P 7,000. If the project requires an investment of P 25,000 with a salvage value of P 5,000, what is the payback period? a. 2.265 years c. 2.526 years b. 2.562 years d. 2.625 years 26. Which of the following is necessary in order to calculate the payback period for a project? a. Useful life c. Net present value b. Cost of capital d. Annual cash flow 27. An advantage of using the payback method is that the method is: a. Precise in estimates of profitability b. Simple to compute c. Not based on cash flow data d. Insensitive to the life of the project being evaluated 28. HIJ Inc. recently acquired a machine at a cost of P 64,000. It will be depreciated on a straight-line basis over years, with no estimated salvage value. HIJ estimates that this machine will produce a P 18,000 annual net cash flow before income tax. Assuming an income tax rate of 50%, ,the appropriate payback period on this investment is: a. 3.6 years c. 7.1 years b. 4.9 years d. 12.8 years 29. A company is investigating the possibility of acquiring a machine that will cost P 12,000 and will have annual depreciation for tax purposes of P 2,400 for 5 years. The machine is expected to result in cash savings from operations of P 4,000 per year. If the tax rate is 50%, what is the payback period for the new machine? a. 3 years c. 5 years b. 3.75 years d. 6 years 30. KLM Company is planning to purchase a new machine. The payback period is estimated to be 6 years. The project's after tax cash flow is estimated to be P 2,000 yearly for the first three years and P 3,000 yearly for the next three years of the payback period. Annual depredation of P 1,300 will be charged to income for each of the 6 years of the payback period. The machine will cost: a. P 15,000 c. P 9,000 b. P 12,000 d. P 6,000 31. ABC Company is planning to purchase a new machine for P 30,000. The payback period is expected to be five years. The new machine is expected to produce cash flows from operations, net of income taxes, of P7,000 a year in each of the next three years and P 5,500 In the fourth year. Depreciation of P 5,000 a year will be charged to income for each of the five years of the payback period. What is the amount of cash flow from operations, net of income taxes, that the new machine is expected to produce In the last (fifth) year of the payback period? a. P 1,000 c. P 5,000 b. P 3,500 d. P 8,500 32. As a capital budgeting technique, the pay back period considers depreciation expense (DE) and time value of money (TMV) as follows: a. DE, relevant and TVM, relevant c. DE, irrelevant. and TVM, relevant b. DE, irrelevant and TVM, Irrelevant d. DE, relevant and TVM, irrelevant 33. The payback method assumes that all cash inflows are reinvested to yield a return equal to a. The discount rate c. The internal rate of return b. The hurdle rate d. Zero 34. A project costing P180,000 will produce the following annual cash benefits and salvage value: End of year Cash benefits Salvage value 1 P50,000 P70,000 2 50,000 60,000 3 50,000 50,000 What is the bailout payback? a. 3 years c. 2.4 years b. 2.6 years d. 2 years 35. VWX Company purchased a new machine on January 1 of this year for P 90,000, with an estimated useful life of 5 years and a salvage value of P 10,000. The machine will be depreciated using the straight-line method. The machine is expected to produce cash flow from operations, net of tax, of P 36,000 a year in each of the next 5 years. The new machine's salvage value is P 20,000 in years 1 and 2, and P 15,000 in years 3 and 4. What will be the bailout period for this machine? a. 1.4 years c. 1.9 years b. 2.2 years d. 3.4 years 36. Investment A has a payback period of 5.4 years; investment B, 6.7 years. From this, we can conclude a. That investment A has a higher NPV than B b. That investment A has a higher IRR than B c. That investment A's book rate of return is higher than B's d. None of the above 37. When computing for the accounting rate of return (ARR), which of the following is used? a. Income before depreciation and taxes c. Income before depreciation but not taxes b. Income after depreciation and taxes d. Income after depreciation but before taxes 38. PQR Company is considering the acquisition of a personal computer that costs P 120,000 with an economic life of 12 years and a terminal salvage value of P 12,000. It is estimated that the increase in net income before taxes as a result from this investment wilt amount to P 7,000 annually. Income taxes are 35%. The company uses the straight-line method of depreciation. What is the accounting rate of return on the average cost of investment? a. 3.79% c. 6.89% b. 5.83% d. 6.98% 39. QQQ, Inc., a calendar year company, purchased a new machine for P 28,000 on January 1, 2006. The machine has an estimated useful life of eight years with no salvage value and is being depreciated on the straight-line basis. The accounting (book value) rate of return is expected to be 15% on the initial increase in required investment. On the assumption of a uniform cash flow, this investment is expected to provide annual cash flow from operations, net of income taxes, of: a. P 3,500 c. P4,200 b. P 4,025 d. P7,700 40. The time-value of money means that a. A peso today is worth more than a peso in the future. b. The longer one waits for a peso, the more uncertain the receipt is c. Both of these d. None of these 41. Which of the following rate of return methods considers the time value of money? a. IRR c. Payback reciprocal b. ARR d. None of the given 42. Which of the following methods is a discounted cash flow method for evaluating capital Investment? a. Payback c. Internal rate of return b. Ball-out payback d. Payback reciprocal 43. Net present value (NPV) is a. The sum of discounted cash inflows b. The sum of discounted cash outflows c. The sum of discounted cash inflows less the sum of the discounted cash outflows d. The sum of discounted cash inflows plus discounted cash outflows 44. The discount rate that equates the present value of expected cash flows with the cost of investments is the a. Net present value c. Accounting rate of return b. Internal rate of return d. Payback period 45. Which one of the following is a project ranking method rather than a project screening method? a. Net present value c. Profitability index b. Simple rate of return d. Sophisticated rate of return 46. A project that has a positive NPV discounted at a rate of 15% would have a discounted rate of return of a. 0% c. More than 15% b. 15% d. less than 15% 47. In computing the PV of future cash inflows that are uniform, reference will be made to a table that shows a. Amount of P1 c. Present value of annuity of P1 b. PV of P 1 d. Future value of annuity of P 1 48. The present value of P 50,000 due in five years would be highest if discounted at a rate of a. 0% c. 15% b. 10% d. 20% 49. A project requires an investment of P 40,000 and has a net present value of P 10,000. The project's profitability Index would be: a. 0.80 c. 4.0 b. 1.25 d. 1.0 50. Which of the following methods measures cash flows and outflows of a project as if they occurred at a single point in time? a. Payback and bail-out payback period c. Net present value and internal rate of return b. Accounting and internal rate of return d. Return on original and average investment 51. The present value and discounted cash flow rate of return methods of evaluating capital expenditure proposals are superior to the payback method in that they: a. Are easier to implement b. Consider the time value of money c. d. Requires less input Reflects the effects of depreciation and income tax 52. A company purchased Machine 123 on March 5, 2005, for P 5,000 cash. The estimated salvage value was P 200 and the estimated life was 11 years. On March 5, 2006, the company learned that It could purchase a different machine for P 8,000 cash. The new machine would save the company an estimated P 250 per year, compared to machine 123. The new machine would have no estimated salvage value and an estimated life of 10 years. The company could get P 3,000 from selling Machine 123 on March 5, 2006. Ignoring income tax, the calculation that would best assist the company in deciding whether to purchase new machine is: a. Present value of P 250 for each of the next 10 years + P 3,000 - P 8,000 b. Present value of P 250 for each of the next 10 years - P 8,000 c. Present value of P 250 for each of the next 10 years + P 3,000 - P 8,000 - P 5,000 d. Present value of P 250 for each of the next 10 years + P 3,000 - P 8,000 - P 4,000 53. The effectiveness of the present value method has been appropriately questioned as a capital expenditure evaluation technique because: a. Predicting future cash flows is often difficult and often associated with uncertainties b. The average return on Investment method Is more accurate and useful c. The payback method is theoretically more reliable d. The computation Involves difficult mathematical applications most accountants cannot perform 54. You have been consulted to advise MNO Corp. on the projected acquisition of another production costing P1 million. The line has an expected useful life of five (5) years without any salvage value. The following additional information was made available: Year Estimated Annual Cash Inflow Present Value of P1 1 P600,000 0.91 2 300,000 0.76 3 200,000 0.63 4 200,000 0.53 5 200,000 0.44 TOTAL P1,500,000 3.27 Assuming that the cash flow is generated evenly during the year, your advice is a. To invest due to net present value of P521,280 b. To invest due to net present value of P94,000 c. To invest due to net advantage of P500,000 d. To invest due to net present value of P635,000 55. Assume the same data in No. 54, only that the annual cash inflow was uniform through the years, how much is the net present value? a. P94,000 c. P91,000 b. (P19,000) d. Cannot be determined from information 56. What capital budgeting methods assumes that the funds are reinvested at the company’s cost of capital? a. Payback c. Net present value b. Accounting rate of return d. Time adjusted rate of return 57. UVW, Inc. acquired a turning machine that has a useful life of 10 years with no salvage value. The incremental annual net income before taxes is P8,500. Income taxes are 25% each year. The PV of an annuity of p1 for 10 years at 18% (the company’s cost of capital) is 4.494. Annual depreciation is P5,000. The NPV is positive P1,119.25. How much is the amount of investment? a. P30,000 c. P50,000 b. P40,000 d. P60,000 58. A project costing P28,715 will produce the following cash benefits after taxes: End of year After-tax cash benefits 1 P11,000 2 15,000 3 18,000 The company’s cost of capital is 16%. The PV of P1 for one year at 16% is 0.862; for two years is 0.743; for three years is 0.641. What is the discounted (PV) payback period? a. 1.7 years c. 2.3 years b. 2 years d. 2.7 years 59. Consider an investment with the following cash inflows: Year Cash flows PV of P1 at 14% 0 (P31,000) 1.000 1 10,000 0.877 2 20,000 0.770 3 10,000 0.675 4 10,000 0.592 What is the profitability index? a. 1.824 c. 1.482 b. 1.284 d. 1.842 60. Ignoring income taxes, how are the following used in the calculation of the net present value of a proposed project? Depreciation expense Salvage value a. Include Include b. Include Exclude c. Exclude Include d. Exclude Exclude 61. If an Investment has a positive NPV a. Its IRR is greater than the company's cost of capital b. Cost of capital exceeds the cutoff rate of return c. Its IRR is less than the company's cutoff rate of return d. the cutoff rate of return exceeds cost of capital 62. DEF Company purchased a machine, which will be depreciated on the straight-line basis over an estimated useful life of seven years and no salvage value. The machine is expected to generate cash flows from operations, net of income taxes of P 80,000 in each of the seven years. DEF's expected rate of return is 12%. Information on present value factors is as follows: Present value of Plat 12% for seven periods: 0.452 Present value of an ordinary annuity of Plat 12% for 7 periods: 4.564 Assuming a positive net present value of P 12,720, what is the cost of the machine? a. P 240,400 c. P 352,400 b. P 253,120 d. P 377,840 63. On January 1, a company invested in an asset with a useful life of 3 years. The company's expected rate of return is 10%. The cash flow and present and future value factors for tile 3 years are as follows: Year Cash inflows Present value of P 1 @ 10% Future value of P 1 @ 10% 1 P8,000 0.91 1.10 2 P 9,000 0.83 1.21 3 P 10,000 0.75 1.33 All cash inflows are assumed to occur at year-end. If the asset generates a positive net present value of P2,000, what was the amount of the original investment? a. P 20,250 c. P 30,991 b. P 22,250 d. P 33,991 64. An investment in a new piece of equipment costing P 50,000 is expected to yield the following over its 5-year useful life: Revenues (cash), P 40,000; operating costs (cash), P 18,000; depreciation, P 10,000. The present value of P 1 received annually for 5 years and discounted at the company's cost of capital is 4.10 assuming that all cash flows occur at year-end. The benefit cost ratio (profitability Index) for this piece of equipment, ignoring tax effect, is a. 0.984 c. 1.804 b. 1.200 d. 2.200 65. The internal rate of return (IRR) is the a. Hurdle rate b. Rate of return for which the net present value is greater than 1.0 c. Rate of return generated from the operational cash flows d. Rate of return for which the net present value is equal to zero 66. STU, Inc. is planning to invest P 120,000 in a 10-year project. STU estimates that the annual cash inflow, net of income taxes, from this project will be P 20,000. STU’s desired rate for return on investments of this type is 10%. Information on present value factors is as follows: @ 10% @ 12% Present value of P 1 for 10 periods 0.386 6.145 Present value of an annuity of P 1 for 10 periods 0.322 5.650 STU's expected rate of return on this investment is a. Less than 10%, but more than 0% c. Less than 12%, but more than 10% b. 10% d. 12% 67. Which of the following is a basic difference between IRR and ARR criteria for evaluating investments? a. IRR emphasizes expenses; ARR emphasizes expenditures b. IRR emphasizes revenues; ARR emphasizes receipts c. IRR is used for internal investments; ARR Is used for external investments d. IRR concentrates on receipts and payments; ARR concentrates on revenues and expenses. 68. Qualitative issues could increase the acceptability of a project under which of the following conditions? a. The IRR is more than the company's cutoff rate b. The projected has a positive NPV c. The payback period is shorter than the. industry standards for payback d. All of the above 69. A company is considering a capital investment for which the Initial cash outlay is P 20,000. Net cash flows from operations, net of income taxes, are predicted to be P 4,000 for 10 years. Assume a cost of capital of 12%. present value of an annuity of P 1 for 10 years at various rates are as follows: Discount Rate PV Factor 14$ 5.216 15% 5.018 16% 4.833 17% 4.658 What is the company's internal rate of return? (Choose the best answer) a. 15.1% c. 15.3% b. 15.2% d. 15.4% 70. A planned factory expansion project has an estimated initial cost of P 800,000. Using a 20% discount rate/ the present value of future cost savings from the expansion is P 843,000. To yield exactly a 20% time adjusted rate of return, the actual investment cost cannot exceed the P 800,000 estimate by more than: a. P 160,000 c. P 43,000 b. P 20,000 d. P 1,705 71. FGH Corporation is planning to invest P 80,000 in a three-year project FGH's expected rate of return is 10%. The present value of P1 at 10% for 1 year is 0.909, for two years is 0.826 and for the three years is 0.751. The cash flows, net of income taxes, will be P 30,000 for the first year (present value: P 27,270) and P 36/000 for the second year (present value: P 29,736). Assuming the rate of return is exactly 10%, what will be the net cash flow, net of income taxes, for the third year? c. P 17,260 c. P 22,904 d. P 22,000 d. P 30,618 72. All of the, following are methods that aid management in analyzing the expected results of capital budgeting decisions, except a. Accrual accounting rate of return c. Discounted cash flow rate of return b. Payback method d. Future value of cash flow 73. The reason for using probabilities in capital budgeting decision is: a. Risk and uncertainty c. Time value of money b. Cost of capital d. Projects with unequal lives 74. If applied in capital budgeting evaluation, sensitivity analysis a. Is used extensively when cash flows are known with certainty. b. Is a "what if” technique that asks how a given outcome will change if the original estimate's of the capital budgeting model are changed. c. Measures the amount of time it will take for a project to recover its initial capital outflow. d. Is a technique used to rank various capital projects. 75. Which of the following combinations is possible? Profitability Index NPV IRR a. Greater than 1 Positive Equals cost of capital b. Greater than 1 Negative Less than cost of capital c. Less than 1 Negative Less than cost of capital d. Less than 1 Positive Less than cost of capital 76. JKL Co. uses a 12% hurdle rate for ali capital expenditures. It has lined up four projects: In Thousand Pesos Initial cash outflow Project 1 Project 2 Project 3 Project 4 Annual net cash inflows 400 596 496 544 Year 1 130 200 160 190 Year 2 140 270 190 250 Year 3 160 180 180 180 Year 4 80 130 160 160 Net present value (7,596) 8,552 28,128 29,324 Profitability Index (%) 98% 101% 106% 105% Internal rate of return 11% 13% 14% 15% If the company has no budgetary limitations, which projects should be pursued? a. Projects 3 and 4 c. Projects 2, 3 and 4 b. Project 4 d. All the four projects 77. LMNO Corporation is contemplating four projects, L, M, N, and O. The capital costs for the initiation of each project and its estimated after-tax, net cash flows are listed below. The company's desired after-tax opportunity costs is 12%. It has P 900,000 capital budget for the year. Idle funds cannot be reinvested at greater than 12%. In thousand pesos Initial cash outflow L M N O Annual net cash inflows 400 470 380 420 Year 1 113 180 90 80 Year 2 113 170 110 100 Year 3 113 150 130 120 Year 4 113 110 140 130 Year 5 113 100 150 150 Net present value P7,540 P59,654 P54,666 (P15,708) Profitability index 1.02 1.13 1.14 0.96 Internal rate of return 12.7% 17.6% 17.2% 10.6% The company will choose: a. Projects, M, N, and 0 b. Projects M and N c. Projects Land N d. Projects Land M 78. A company's marginal cost of new capital is 10% up to P 600,000. It increases 0.5% for the next P 400,000 and another 0.5% thereafter. Several propose capital project are under consideration, with projected cost and internal rates of return as follows: Project Cost IRR A P 100,000 10.5% B P 300,000 14.0% C P 450,000 10.8% D P 350,000 13:5% E P 400, 000 12.0% What should the company's capital budget be? a. P 650,000 b. P 1,050,000 c. P 1,500,000 d. P 1,600,000 79. For P 450,000, BCD Corp. purchased a new machine with an estimated useful life of five years with no salvage value. The machine is expected to produce cash flow from operations, net of 40% income taxes, as follows: First year P 160,000 Second year 140,000 Third year 180,000 Fourth year 120,000 Fifth year 100,000 BCD Corp. will use the sum-of-years-digits' method to depreciate the new machine: First year P 150,000 Second year 120,000 Third year 90,000 Fourth year P 60,000 Fifth year 30,000 The present value of P 1 for 5 periods at 12% is 3.60478. The present values of P1at 12% at end of each period are: Period PV factor 1 0.89280 2 0.79719 3 0.71178 4 0.63552 5 0.56743 Had BCD used the straight-line method of depreciation, what is the difference in net present value provided by the machine at a discount rate of 12%? a. Increase of P 9,750 c. Decrease of P 24,376 b. Decrease of P 9,750 d. Increase of P 24,376