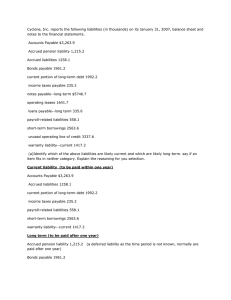

TRADE AND OTHER PAYABLES, ESTIMATED LIABILITIES & CONTINGENT LIABILITIES – Quiz Material 1. Current liabilities are likely to arise from: (a) accrued interest on long-term loans. (b) receipt of advance payment for services to be rendered. (c) purchase of inventory and operating supplies. (d) all of the above. 2. An example of estimated liability is: (a) interest payable on bonds (b) wages payable obligation (c) allowance for uncollectibles (d) product warranties ar stu ed d vi y re aC s o ou urc rs e eH w er as o. co m 3. An example of contingent liability is: (a) unearned subscription revenue (b) bond premium (c) wages payable (d) potential future payment on a pending breach of contract lawsuit 4. A particular warranty obligation is probable and the amount of loss can be reasonably estimated. The particular parties that will make claims under the warranty are not identifiable. An estimated loss contingency should then be: (a) classified as an appropriation of retained earnings (b) neither accrued nor disclosed (c) disclosed but not accrued (d) accrued is 5. Reserves for general contingencies for general or unspecified business risks should: (a) be accrued on the financial statements and disclosed on the notes thereto (b) not be accrued on the financial statements but should be disclosed on the notes thereto (c) not be accrued on the financial statements and need not be disclosed on the notes thereto (d) be accrued on the financial statements but need not be disclosed on the notes thereto sh Th 6. Which is not an essential characteristic of an accounting liability? (a) The liability is the present obligation of a particular enterprise. (b) The liability arises from past transaction or event. (c) The settlement of the liability requires an outflow of resources embodying economic benefits. (d) The liability is payable to a specifically identified payee. 7. The principal classifications of liabilities are: (a) current liabilities and noncurrent liabilities. (b) current liabilities, noncurrent liabilities and deferred revenue. (c) current liabilities and deferred revenue. (d) noncurrent liabilities and deferred revenue. 8. A long-term debt falling due within one year should be reported as noncurrent liability should be reported as noncurrent liability if the following conditions are met (choose the incorrect one): (a) The original term is for a period of more than one year. (b) The enterprise intends to refinance the obligation on a long-term basis. (c) The intent to refinance is supported by an agreement to refinance which is completed before the issuance of the financial statements. This study source was downloaded by 100000821975975 from CourseHero.com on 03-26-2021 01:48:22 GMT -05:00 https://www.coursehero.com/file/36926550/LIABILITIES-Quizdoc/ (d) The intent to refinance is supported by an agreement to refinance which is completed after the issuance of the financial statements. 9. Which will demonstrate an agreement to refinance (choose the incorrect one)? (a) Long-term obligation has in fact been issued before the issuance of the financial statements for the purpose of refinancing. (b) Equity security has in fact been issued before the issuance of the financial statements for the purpose of refinancing. (c) Before the issuance of the financial statements, the enterprise has in fact entered into a financing agreement that clearly permits the enterprise to refinance the currently maturing long-term debt on a long-term basis. (d) Preferred stock has in fact been issued before the issuance of financial statements for the purpose of obtaining working capital. 10.A provision is recognized as liability when (choose the incorrect one): (a) the enterprise has a present obligation as a result of past event. (b) the enterprise has a possible obligation as a result of past event. (c) it is probable that a transfer of economic benefits will be required to settle the obligations. (d) the amount of the obligations can be measured reliably. ar stu ed d vi y re aC s o ou urc rs e eH w er as o. co m 11.An accrued expense can be best described as an amount: (a) paid and currently matched with earnings. (b) not paid and not currently matched with earnings. (c) paid and not currently matched with earnings. (d) not paid and currently matched with earnings. 12.Which of the following statements is true concerning contingent liabilities? (a) Such liabilities should include obligations of known existence but of unknown amount. (b) If the definite amount is involved, it is not a contingent liability. (c) Such liabilities are generally reported and totaled with other liabilities to make up the liability section of most balance sheets. (d) Such liabilities should include obligations known in amount but unknown in existence. Th is 13.An item that is not a contingent liability is: (a) premium offer to customers for labels or box tops. (b) accommodation endorsement on customer note. (c) additional compensation that may be payable on a dispute now being arbitrated. (d) note receivable discounted. sh 14.On September 1, 2001, a company borrowed cash and signed a two-year interest bearing note on which both the principal and interest are payable on September 1, 2003. How many months of accrued interest would be included in the liability for accrued interest at December 31, 2001 and December 31, 2002? December 31, 2001 December 31, 2002 (a) 4 months 16 months (b) 4 months 4 months (c) 12 months 24 months (d) 20 months 8 months 15.On September 1, 2001, a company borrowed cash and signed a one-year interest bearing on which both the principal and interest are payable on September 1, 2002. How will the note payable and the accrued interest be classified In December 31, 2001 balance sheet? Note payable Accrued interest (a) Current liability Noncurrent liability (b) Noncurrent liability Current liability (c) Current liability Current liability (d) Noncurrent liability No entry. This study source was downloaded by 100000821975975 from CourseHero.com on 03-26-2021 01:48:22 GMT -05:00 https://www.coursehero.com/file/36926550/LIABILITIES-Quizdoc/ 16.Grip Company started a new promotional campaign program. For every 10 box tops returned to Grip, customers receive a ballpen. Grip estimates that only 40% of the box tops reaching the market will not be redeemed. Additional information is as follows: Units Amount Sales of product 100,000 30,000,000 Ballpens purchased5,500 4,125,000 Ballpens distributed 4,000 What is the amount of year-end estimated liability associated with this promotion? (a) 4,125,000 (b) 1,500,000 (c) 3,000,000 (d) 4,500,000 17.On April 1, 2002, Art Corporation began offering a new product for sale under a one-year warranty. Of the 50,000 units in inventory at April 1, 2002, 30,000 had been sold by June 30, 2002. Based on its experience with similar products, Art estimated that the average warranty cost per unit sold would be P80. Actual warranty costs incurred from April 1 through June 30, 2002 were P700,000. At June 30, 2002, what amount should Art report as warranty expense? (a) 700,000 (b) 900,000 (c) 1,700,000 (d) 2,400,000 ar stu ed d vi y re aC s o ou urc rs e eH w er as o. co m 18.Right Store sells gift certificates, redeemable for store merchandise, that expire one year after their issuance. Right has the following information pertaining to its gift certificate sales and redemptions: Unredeemed at 12/31/2002 750,000 2003 sales 2,500,000 2003 redemptions of prior year sales 250,000 2003 redemptions of current year sales 1,750,000 Right’s experience indicates that 10% of gift certificates sold will not be redeemed. In its December 31, 2003 income statement, what amount should Right report as revenue? (a) 2,500,000 (b) 2,000,000 (c) 1,250,000 (d) 500,000 Th is 19.Kite Company sells magazine subscriptions of one to three-year periods. Cash receipts from subscribers are credited magazine subscriptions collected in advance, and this account had a balance of P2,400,000 at December 31, 2002 before year-end adjustment. Outstanding subscriptions at December 31, 2002 expire as follows: During 2003 600,000 During 2004 900,000 During 2005 400,000 In its December 31, 2002 balance sheet, what amount should Kite report as the balance for magazine subscriptions collected in advance? (a) 500,000 (b) 1,200,000 (c) 1,900,000 (d) 2,400,000 sh 20.Jar Company must determine the December 31, 2002 year-end accruals for advertising and rent expense. A P50,000 advertising bill was received January 7, 2003 comprising costs of P35,000 for advertisements in December 2002 issues, and P15,000 advertisements in January 2003 issues of the newspaper. A store lease, effective December 16, 2001, calls for fixed rent of P120,000 per month, payable one month from the effective date and monthly thereafter. In addition, rent equal to 5% of net sales over P6,000,000 per calendar year is payable on January 31 of the following year. Net sales for 2003 were P9,000,000. In its December 31, 2002 balance sheet, Jar should report accrued liabilities of: (a) 260,000 (b) 185,000 (c) 210,000 (d) 245,000 21.On March 1, 2002, Fine Company borrowed P1,000,000 and signed a 2-year note bearing interest at 12% per annum compounded annually. Interest is payable in full at maturity on February 28, 2004. What amount should Fine report as a liability for accrued interest at December 31, 2003? This study source was downloaded by 100000821975975 from CourseHero.com on 03-26-2021 01:48:22 GMT -05:00 https://www.coursehero.com/file/36926550/LIABILITIES-Quizdoc/ (a) 112,000 (b) 120,000 (c) 232,000 (d) 0 For items 22 and 23: On December 31, 2001, the bookkeeper of Glory Corporation provided the following information: Accounts payable, including deposits and advances from customers of P25,000 P125,000 Notes payable, including note payable to bank on December 31, 2003 of P50,000 150,000 Acceptances payable 10,000 Liabilities under trust receipts 80,000 Stock dividends payable 200,000 Credit balances in customers’ accounts 20,000 Serial bonds payable in semiannual installment of P50,000 500,000 Accrued interest on bonds payable 15,000 Dividends in arrears on preferred stock 70,000 Contested BIR assessment 30,000 Unearned rent income 5,000 22.The amount of current liabilities on December 31, 2001 is: (a) P455,000 (b) P480,000 (c) P450,000 P485,000 23.The amount of noncurrent liabilities on December 31, 2001 is: (a) P455,000 (b) P480,000 (c) P450,000 (d) P485,000 ar stu ed d vi y re aC s o ou urc rs e eH w er as o. co m (d) 24.Anette Video Company sells 1-and 2-year subscriptions for its video-of-the-month business. Subscriptions are collected in advance and credited to sales. An analysis of the recorded sales activity revealed the following: 1997 1998 Sales P420,000 P500,000 Less: Cancelations 20,000 30,000 Net sales P400,000 P470.000 Subscription expirations: 1997 1998 1999 2000 Th is P120,000 155,000 P130,000 125,000 200,000 ________ 140,000 P400,000 P470,000 In Anette’s December 31, 1998 balance sheet, the balance for unearned subscriptions revenue should be: (a) P495,000 (b) P470,000 (c) P465,000 (d) P340,000 sh 25.Felly Company operates a retail grocery store that is required by law to collect refundable deposits of P5 on soda cans. Information for 2001 follows: Liability for refundable deposits – 12/31/2000 P150,000 Cans of soda sold in 2001 100,000 Soda cans returned in 2001 110,000 On February 1, 2001, Felly subleased space and received a P25,000 deposit to be applied against rent at the expiration of the lease in 2005. In Felly’s December 31, 2001 balance sheet, the current and noncurrent liabilities for deposits were: Current Noncurrent (a) P125,000 P 0 (b) 100,000 25,000 (c) 100,000 0 (d) 25,000 100,000 26.In an effort to increase sales, Mills Company inaugurated a sales promotional campaign on June 30, 1998. Mills placed a coupon redeemable for a premium in each package of cereal sold. Each premium cost Mills P20 and a customer to receive a premium must present five coupons. Mills estimated that only 60% of This study source was downloaded by 100000821975975 from CourseHero.com on 03-26-2021 01:48:22 GMT -05:00 https://www.coursehero.com/file/36926550/LIABILITIES-Quizdoc/ the coupons issued will must be redeemed. For the 6 months ended December 31, 1998, the following information is available: Packages of cereal sold Premiums purchased Coupons redeemed 160,000 12,000 40,000 What is the estimated liability for premium claims outstanding at December 31, 1998? (a) P160,000 (b) P224,000 (c) P288,000 (d) P384,000 B 27.During 1998, Day Company sold 500,000 boxes of cake mix under a new sales promotional program. Each box contains one coupon, which entitle the customer to a baking pan upon remittance of P4.00. Day pays P5.00 per pan and P0.50 for handling and shipping. Day estimates that 80% of the coupons will be redeemed, even though only 300,000 coupons had been processed during 1998. What amount should Day report as a liability for unredeemed coupons at December 31, 1998? (a) P100,000 (b) P150,000 (c) P300,000 (d) P500,000 B ar stu ed d vi y re aC s o ou urc rs e eH w er as o. co m 28.Mill Company sells washing machines that carry a three-year warranty against manufacturer’s defects. Based on company experience, warranty costs are estimated at P30 per machine. During 1998, Mill sold 24,000 washing machines and paid warranty costs of P170,000. In its income statement for the year ended December 31, 1998, Mill should report warranty expense of: (a) P170,000 (b) P240,000 (c) P550,000 (d) P720,000 D 29.Bold Company estimates its annual warranty expense at 2% of annual net sales. The following data are available: Net sales P4,000,000 Warranty liability: December 31, 1997 P60,000 credit Warranty payments during 1998 P50,000 debit After recording the 1998 estimated warranty expense, the warranty liability account would show a December 31, 1998 balance of: (a) P10,000 (b) P70,000 (c) P80,000 (d) P90,000 D is 30.At December 31, 1998, Raft Boutique had 1,000 gift certificates outstanding, which had been sold to customers during 1998 for P70 each. Raft operates on a gross margin of 60% of its sales. What amount of revenue pertaining to the 1,000 outstanding gift certificates should be deferred at December 31, 1998? (a) P 0 (b) P28,000 (c) P42,000 (d) P70,000 D sh Th 31.Ryan Company sells major appliance service contracts for cash. The service contracts are for a one-year, two-year, or three-year period. Cash receipts from contracts are credited to unearned service contract revenue. This account had a balance of P720,000 at December 31, 1998 before year-end adjustment. Service contract costs are charged as incurred to the service contract expense account, which had a balance of P180,000 at December 31, 1998. Outstanding service contracts at December 31, 1998 expire as follows: During 1999 P150,000 During 2000 225,000 During 2001 100,000 What amount should be reported as unearned service contract revenue in Ryan’s December 31, 1998 balance sheet? (a) P540,000 (b) P475,000 (c) P295,000 (d) P245,000 B 32.Kent Company, a division of National Realty Corporation, maintains escrow accounts and pays real estate taxes for National’s mortgage customers. Escrow funds are kept in interest-bearing accounts. Interest, less a 10% service fee, is credited to the mortgagee’s account and used to reduce future escrow payments. Additional information follows: Escrow accounts liability, 1/1/2000 P 700,000 Escrow payments received during 2000 1,580,000 This study source was downloaded by 100000821975975 from CourseHero.com on 03-26-2021 01:48:22 GMT -05:00 https://www.coursehero.com/file/36926550/LIABILITIES-Quizdoc/ Real estate taxes paid during 2000 Interest on escrow funds during 2000 1,720,000 50,000 What amount should Kent report as escrow accounts liability in its December 31, 2000 balance sheet? (a) P510,000 (b) P515,000 (c) P605,000 (d) P610,000 C 33.Dix Company operates a retail store and must determine the proper December 31 200 year-end accrual for the following expenses: (a) The store lease calls for fixed rent P12,000 per month, payable at the beginning of the month, and additional rent equal to 6% of net sales over P2,500,000 per calendar year, payable on January 31 of the following year. Net sales for 2000 are P4,500,000. (b) An electric bill of P8,500 covering the period December 31, 2000 through January 15,2002 was received January 22, 2001. (c) A P4,000 telephone bill was received January 7, 2001 covering: Service in advance for December 2001 P1,500 Local and toll calls for December 2000 2,500 In its December 31, 200 balance sheet, Dix should report accrued liabilities of: (a) P150,750 (b) P131,000 (c) P128,250 (d) P126,750 D ar stu ed d vi y re aC s o ou urc rs e eH w er as o. co m 34.On September 1, 2000, Pine Company issued a note payable to National Bank in the amount of P1,800,0000, bearing interest at 12% and payable in three equal annual principal payments of P600,000. On this date, the bank’s prime rate was 11%. The first interest and principal payment was made on September 1, 2001. At December 31, 2001, Pine should record accrued interest payable of: (a) P44,000 (b) P48,000 (c) P66,000 (d) P72,000 B 35.Mann Corporation’s liability account balances at June 30,2001, included a 10% note payable in the amount of P3,600,000. The note is dated October 1, 2000, and is payable in three equal annual payments of P1,200,000 plus interest. The first interest and principal payments were made on October 1, 2001. In its June 30, 2002 balance sheet, what amount should Mann report as accrued interest payable for this note? (a) P270,000 (b) P180,000 (c) P90,000 (d) P60,000 A 36.On January 1, 2000, Pares Company borrowed P3,600,000 from a major customer evidenced by a non-interest bearing note due in three years. Pares agreed to supply the customer’s inventory needs for the loan period at lower than market price. At the 12% imputed interest rate for this type of loan, the present value of the note is P2,550,000 at January 1, 2000. What amount of interest expanse should be included in Pares’ 2000 income statement? (a) P432,000 (b) P350,000 (c) P306,000 (d) P0 C sh Th is 37.Able, Inc. had the following amounts of long-term debt outstanding at December 31, 2000: 14% term note, 2001 P 3,000 11% term note, due 2004 107,000 8% note, due in 11 equal annual principal payments, plus interest beginning December 31, 2001 110,000 7% guaranteed debentures, due 2005 100,000 Total P320,000 Able’s annual sinking fund requirement on the guaranteed debentures is P4,000 per year. What amount should Able report as current maturities of long-term debt in its December 31, 2000 balance sheet? (a) P4,000 (b) P7,000 (c) P10,000 (d) P13,000 D 38.Eliot Corporation’s liabilities at December 31, 2000 were as follows: Accounts payable and accrued interest P200,000 12% note payable issued November 1, 2000 maturing July 1,2001 60,000 10% debentures payable, next annual principal installment of P100,000 due February 1, 2001 700,000 On March 1, 2001, Eliot consummated a noncancelable agreement with the lender to refianace the 12% note payable on a long-ter basis, on readily determinable terms that have not yet been implemented. Both parties are This study source was downloaded by 100000821975975 from CourseHero.com on 03-26-2021 01:48:22 GMT -05:00 https://www.coursehero.com/file/36926550/LIABILITIES-Quizdoc/ fianacially capable of honoring the agreement’s provisions. Eliot’s December 31, 2000 financial statement were issued on March 31, 2001. In its December 31, 2000 balance sheet, Eliot should report current liabilities at: (a) P200,000 (b) P260,000 (c) P300,000 (d) P360,000C 39.On February 5, 2001, an employee filed a P2,000,000 lawsuit against Steel Company for damages suffered when one of Steel’s plants exploded on December 29,2000. Steel’s legal counsel expects the company will lose the lawsuit and estimates the loss to be between P500,000 and P1,000,000. The employee has offered to settle the lawsuit out of court for P900,000, but Steel will not agree to the settlement. In its December 31, 2000 balance sheet, what amount should Steel report as liability from lawsuit? (a) P2,000,000 (b) P1,000,000 (c) P900,000 (d) P500,000D sh Th is ar stu ed d vi y re aC s o ou urc rs e eH w er as o. co m 40.Sony Corporation sells color TV sets with a three-year repairs warranty. The sales price for each set is P10,000. The average expense of repairing a set is P500. Research has shown that 3% of all sets sold are repaired in the first year, 6% in the second year, and 11% in the third year. The number of sets sold were as follows: 2000 500 units 2001 1,000 units 2002 2,000 units Total payments for repairs associated with the warranties were: 2000, P20,000; 2001, P70,000; and 2002, P150,000. Under the accrual approach, how much is the estimated liability for warranties on December 31, 2002? (a) P350,000 (b) P240,000 (c) P50,000 (d) P110,000D This study source was downloaded by 100000821975975 from CourseHero.com on 03-26-2021 01:48:22 GMT -05:00 https://www.coursehero.com/file/36926550/LIABILITIES-Quizdoc/ Powered by TCPDF (www.tcpdf.org)