cases 3

advertisement

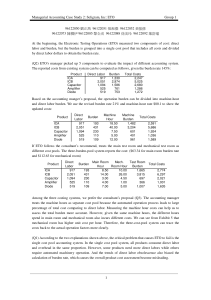

Seligram, Inc.: Electronic Testing Operations Danwei Zhang Jingyi Liu Siyun Zhang Yuxuan Xiao 2. Calculate the costs of the five components described in Exhibit 6 as reported by: a) The existing system; b) The system proposed by the accounting manager; c) The system proposed by the consultant. 4. Would you recommend any changes to the system you prefer? Why? System preferred We prefer the cost system proposed by consultant for the following reasons: Firstly, there is a trend of decline in the direct labor hours and test lots. Also, the test procedure shifts from simple inspection services to broader-based test Technology. Besides, more high-technology components have been introduced. These factors make the cost become more related to machine time instead of labor hour. At the same time, burden will increase with the additional depreciation and engineering costs associated with the new equipment. This will result in a large increase in the burden rate per direct labor hour and the cost will be enormously higher than that of other competitors. Therefore, we don’t choose traditional costing system to keep our cost advantage. Secondly, according to question 2, the main test room overhead rate is 64.4% and Mech. Room Overhead rate is 112.6%. This means there are huge differences between these two rates, and if we simply combine the machine hours and burden costs to calculate the machine hour rate, the result will not be accurate. Therefore, we choose cost system c instead of cost system b and a. Changes and why Cost from new test equipment, such as depreciation and engineering costs, should be removed from total Engineering & Administrative Burden. The original allocation causes a relative high burden rate per direct labor dollar, which does not accurately reflect the actual cost pattern. Depreciation and engineering cost of new equipment have no correlation with labor hour fluctuation. Therefore, those costs related to new machine should be taken away from E&A burden. 5. Would you treat the new machine as a separate cost center or as part of the main test room? Explain. I would treat the new machine as a separate cost center of the main test room. As shown in the table above, if the new machine is integrated into Main test room, machine hour rates in the following eight years will be higher than Main test machine-hour rate(63.3). Then the total cost of the products will increase as well as the selling price. The case also told us the new equipment would only be needed to service the requirements of one or two customers in the foreseeable future. The increasing machine hour rate will result in an increase in charges to other customers and drive them away. Therefore, it would be better to treat the new machine as a separate cost center due to the cost consideration.