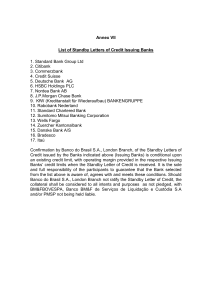

The Peruvian Experience with Financial Liberalization, 1990-1999

advertisement