FAQ for New Accounting Arrangements (For Government Schools Only)

advertisement

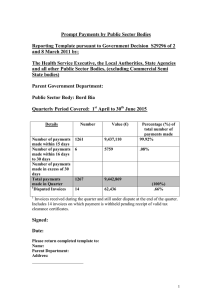

")

URGENT 教育局 Education Bureau FAX Date : 18 March 2016 Number of Pages : 4 (including this page) FROM: Life-wide Learning and Library Section CDI, Education Bureau Rm 1324, Wu Chung House 213 Queen’s Road East Wanchai, Hong Kong TO : Teacher-in-charge of the Hong Kong Jockey Club Life-wide Learning Fund & other relevant staff C.C. : Principal Fax. No. : 2892 6428 Dear Teacher-in-charge, Allocation of Fund for the Hong Kong Jockey Club Life-wide Learning Fund (2015/16 s.y.) & FAQ for New Accounting Arrangements With regard to the allocation of fund for the Hong Kong Jockey Club Life-wide Learning Fund (2015/16 s.y.) (the Fund), most schools have already been refunded by the Bureau Accounts Section (BA) while some will be refunded in due course. Schools are assured that the allocation of fund can be used to continue to support financially needy students for life-wide learning activities in this school year (2015/16) i.e. till 31 August 2016. For teachers’ easy reference, the FAQ for the new accounting arrangements for the Fund issued on 2 March 2016 by BA is enclosed here. Teachers may also find the document on the website of the Fund (http://www.edb.gov.hk/tc/curriculum-development/major-level-of-edu/life-wide-learning/jc -fund/index.html). For enquiries related to the accounting and payment issues, please contact Ms Peggy LEUNG of BA at 2892 6244. The Life-wide Learning and Library Section 1 FAQ – Questions in respect of the Jockey Club Life Wide Learning Fund (JCLWLF) from schools upon the introduction of Financial Circular (FC) No.2/2016 (issued by the Bureau Accounts Section on 2 March 2016) Question 1: Can the JCLWLF be used with other funding/grants? Answer: Subject officers should be in the position to determine the ambit of JCLWLF as well as the regulations/limitations of other funding. If schools wish to have mixed use of JCLWLF with other funding for the same activity/programme, subject officers should consider whether it is appropriate for schools to do so. Question 2: Can the schools settle payments by the end of the school year in one go? Answer: Schools may settle payments for several invoices in one go for their operational consideration. However, schools are reminded to observe the following guidelines/regulations so that settlement of payments should be made in a prompt way as far as practicable: a) According to SAI 1220, where a payment is required to be paid by a specified date, such as under the terms of a contract, school heads must ensure that the payment due date is observed. A copy of SAI is attached below for reference. SAI_Chapter_IV.doc b) According to paragraph 11.07 in Chapter 11 of “Guide on Financial Management in EDB”, Heads of divisions/sections and government schools are required to forward requests for payment to Finance Division promptly. The Guide on Financial Management in EDB can be found in the following link: EDB Intranet Information Directory H. Finance 8.Financial and Accounting Guidelines and Procedures Guide on Financial Management c) According to F&AR 335(2), expenditure properly chargeable to the account of a given financial year must as far as possible be met within that year. A copy of F&AR is attached below for reference. Financial and Accounting Regulations.doc Question 3: Can schools settle payments with other funding/ grants first and transfer back money with the JCLWLF because the extra funding will only be released to schools by March/ April 2016? Answer: During the transitional period when the allocation/disbursement of JCLWLF is not yet made available to schools, schools may adopt the following payment methods and settlement payments with other grants is not suggested as each grant has its own ambit: a) Schools may submit the payment request to the BA Section for direct settlement even though the allocation is not yet made available to schools. 2 b) For urgent payments, schools may settle the payments through sub-imprest accounts first through submission of G.F. 51 and then submit the G.F. 48 for topping up sub-imprest accounts. It is understood that the sub-imprest accounts would soon be subject to retirement for close of financial year 2015-16 in March 2016. In this case, schools may also choose to settle the payment through their non-government fund bank accounts first (e.g. ECA fund bank accounts) and then claim reimbursement through GFMIS AP module by submitting memos certified by principals with supporting documents (e.g. payment slips) to BA section. The forms G.F. 48 and G.F. 51 are attached as below for reference please. GF51.pdf GF 48.pdf Question 4: As the current payment arrangement would involve prepayment by parents first and parents would need to claim back money related to activities of JCLWLF, what is the arrangement for settlement to parents? Answer: Schools have the following methods for making reimbursement to parents: a) Normally, memos certified by the Principals with supporting documents (e.g. acknowledgement receipt signed by the claimant and the Principal) would need to be submitted to BA section for reimbursement to parents. The BA Section would either issue cheques to parents or arrange for auto-bank in. For the payment method of auto-bank in, parents are required to fill in form GF 179A (“Authority for payment to a bank”) to provide bank account information. The form G.F. 179A is attached below for reference please. GF179A.pdf b) For the rare cases where parents do not process any bank accounts, schools can make reimbursement to parents through their own sub-imprest accounts first by drawing cash to parents at or below $5K for each transaction (i.e. through submission of G.F. 51 with the parents as the claimants and the certification by the Principal). For topping up of the schools’ sub-imprest accounts, claim form G.F. 48 should be submitted to BA section. Question 5: Can schools subsidize the same student for the same program in different times (when there is still unspent allocation of the funding)? Answer: Subject officers should be in the position to determine the ambit of the JCLWLF. Finance Division has no objection if the subject officers determine that it is appropriate for schools to subsidize the same students for different activities in different times under JCLWLF. 3 Question 6: What is the grant allocation/disbursement pattern of JCLWLF under the new arrangement? Answer: Under the new arrangement, JCLWLF will be allocated / disbursed as grants to schools under school year basis. Claw back or lapse of grants would also be calculated on a school year basis. As such, the new arrangement would be similar to previous arrangement (i.e. schools would spend the funding in a school year basis and the amount will lapse/be clawed back upon the close of a school year). Question 7: Will schools’ workload increase dramatically as they have to prepare invoice supporting for claiming from the Government? Answer: The schools’ workload should be similar to the previous practice. Previously, for maintaining proper internal controls, schools should have procedures in place that proper accounting records are kept for payment through the non-government bank accounts. Under the new arrangement, the schools will request the same types of supporting documents (e.g. invoices) from the applicants for payment through the Government. Question 8: What is the way of settlement if the invoices comprise of activities of JCLWLF and others which part of invoices requires settlement through other non-government bank accounts? Answer: If schools settle part of the invoices through other non-government bank accounts (i.e. they are not related to JCLWLF) and the remaining part of the invoices by JCLWLF, schools can choose either one of the following two payment methods: a) Ask the suppliers to split the invoices so that the invoices related to JCLWLF are submitted to the BA Section for direct settlement. b) If the splitting of invoices is not possible, schools should mark clearly in the invoices the amounts of invoices that have already been settled by other non-government fund bank accounts and submit these invoices together with the supporting documents to the BA Section so that the BA section can settle the remaining amounts of the invoices to suppliers directly. The schools should observe Appendix 11.3 of Guide on Financial Management of EDB for processing the payments. 4