Chronicles VI

advertisement

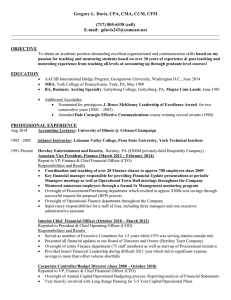

CHRONICLES VI: HOW MANY ACCOUNTANTS DOES IT TAKE TO MANAGE GRANTS & CONTRACTS? The CFO released his office’s 2006/2007 costs for Grants and Contracts (G&C) Institutional Support (defined as accounting, contracts, human resources, general oversight, checks and balances) to the PBAC meeting recently. His numbers highlight the need for an independent audit/investigation at SSU; they are unsubstantiated and do not match the IDC income generated for FY 2006-2007. The numbers also prove the Chronicles’ assertion that A&F has post-award delegated authority and is responsible for monitoring grants and contracts, including those of CIHS. The Costs are Unsubstantiated Chancellor’s Office Executive Order 753 mandates that indirect costs shall be allocated to auxiliary programs according to a Cost Allocation Plan that is rewritten annually, preferably prior to, but not later than the period covered. The cost allocations must be adequately supported by documentation that could be independently verified, signed by the CFO, and monitored during the course of the year (CO Report Number 05-13, May 19, 2006). For more on EO753 and Cost Allocation Plans, see Chronicles III: Indirect Costs (IDC) or Follow the Money. The CFO lists a total of 34 A&F personnel (equaling nearly 16 FTEs) who are said to provide Institutional Support to G&C for a cost of $1,148,520. Of these, 2.05 are senior administrators making over $100,000 a year, including Larry Schlereth (10%) and Letitia Coate (15%); 3.17 are senior management earning between $80 and $100,000 a year; 5.5 are specialists earning between $40, and $80,000; and 5.1 are technicians making below $40,000. Most are accountants and financial specialists. We believe that this number is significantly inflated and that a fair tally of A&F’s actual level of effort would equal about 7 FTEs and a cost of under $600,000. The costs prove A&F is responsible for grant oversight Any remaining questions regarding A&F’s responsibility in the operation of CIHS should be put to rest by these numbers. This is a huge team and as CIHS generated around 70% of the business on campus, this team had plenty of resources to oversee their financial and human resources areas. The CFO and AVP took a percent of their own salaries from this budget and cannot now claim they had no responsibilities. Note, not one penny went to Academic Affairs to provide oversight, in spite of the many personnel in the Schools heavily involved in day-to-day grant administration work. Questions that need answers Why do some names have “delegated authority” and others not, particularly Letitia Coate and Larry Schlereth? Campus Policy designates them as the holders of post-award delegated authority. Where is the detailed cost accounting plan required by EO753? Why were the labor/cost distributions upon which the percents are based not provided? If there are no supporting data, will A&F submit to auditors looking into this? A real audit would require interviewing each of the people to substantiate that they spent the amount of time indicated working on grants and contracts as well as interviewing the end-users in G&C regarding the services they received from the named individuals. Job descriptions for the positions and work products in support of the claims should also be requested. The funds should have been used to reimburse the General Fund. Where is the documentation that this occurred and to what use were the funds reallocated? Why does money go to these 34 positions within A&F without any funds distributed to the schools and programs that actually receive and administer the grant and contract programs? A&F made a presentation recently to the Senate in which it was stated that there were no paid positions in the Academic Foundation. The work to manage Foundation is done by A&F using general fund monies. EO753 states that all auxiliaries must be treated in a similar fashion. Why does the Foundation get a free ride, while Grants and Contracts gets a bill for $3 million plus? The $1,712,989 (see CFO spreadsheet) to A&F for EO753 Institutional Support is only the beginning, however. The Special Projects Summary for 06-07 shows IDC in the neighborhood of $3.5 million. This leaves around $1.8 million not accounted for by the CFO’s spreadsheet. Where is a detailed accounting of that money? Where is the accounting for 05-06, the pivotal year when over $500,000 in administrative funding was withheld from CIHS, precipitating the mess in which we find ourselves now? The Real Question Either A&F charged staff to the grants because they are responsible for grant oversight OR A&F has used IDC to free up staff costs that would otherwise be charged to the general fund. If A&F used the grant funds to free up general fund money, where did that money go? Why didn’t it go to instruction?