Talking Point Schroders Chinese challenges and rate risks

advertisement

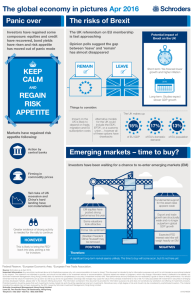

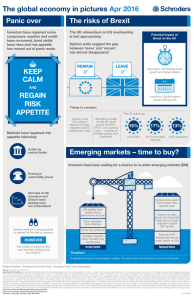

October 2015 Schroders Talking Point Chinese challenges and rate risks Peter Harrison, Head of Investment and Keith Wade, Chief Economist & Strategist We think the concerns that prompted recent market volatility have been overplayed. Over the medium-term, the prospects for global growth remain reasonable. While a slowing emerging world (particularly China) may cause global growth to weaken, the developed world is still growing well. Lower oil prices seem to be feeding through into stronger consumer spending, especially in the US, Europe and UK while real wages are rising in some parts too. Investors need to look at the pockets of value arising as a result of the selloff in emerging markets and commodity prices. High-yielding stocks are one area of the market which have become quite depressed, and the value style of investing has been out of favour. We think you’ll start to see a return to those types of themes. In terms of asset allocation, we are waiting to upgrade emerging markets. The problems facing the emerging world are well known and that in the next few months, investors should consider re-orientating themselves back towards this area of the market. Chinese authorities regaining grip on economy One of the main factors behind the summer’s equity market selloff was investor concern that the Chinese authorities had lost their ability to stabilise the economy and markets. However, since then, policymakers have made it clear that they do not plan to devalue the yuan significantly. A fiscal package has also subsequently been announced. The authorities are regaining their grip on the economy again and people are beginning to feel a little more comfortable that policymakers will be able to stimulate growth. However, if the Chinese economy were to experience a “hard landing”, we could see a global recession as well as a potential currency war. For such a scenario, investors could choose lower risk fixed income and dollar assets. That said, the trade-weighted dollar is already nearly at an all-time high, which indicates investors are hiding out there already. The world’s major policymakers appear to be working together in a covert form of “international cooperation” by avoiding policy action that would significantly disrupt markets. For example, the Chinese authorities have not devalued the yuan, the Bank of Japan has not boosted its quantitative and qualitative easing (QQE) programme and the Federal Reserve (Fed) did not raise interest rates as had been expected in September. Not the right environment for US rate rises The decision to further postpone the first US interest rate rise was due to a lack of conviction that inflation can get back to the Fed’s target of 2%. Headwinds from weaker emerging markets and a strong dollar have had a deflationary effect on the economy, even though the domestic economy is performing well with a tightening labour market. Wages are not rising yet but we expect them to start to do so soon. We think the next rate rise is probably not on the cards until March next year. In the near term the US economy will continue to grow but not by enough to push up inflation. SchrodersTalking Point Page 2 A stabilisation in Chinese growth and some stronger wage growth in the US are the likely triggers for an eventual rate rise. If we see some signs that wages are picking up, the Fed will feel more comfortable raising rates. The lack of liquidity As a result of interest rate rises, liquidity issues are back in the spotlight. In late August there was a substantial selloff in some really big ETFs and some ETF providers were talked talking about a crack in markets. This could be a ‘canary in the coalmine’. If liquid instruments are not working at a time when they should, that is a big warning sign that things are not right. The low interest rate environment is only going to exacerbate the situation because investors will continue to look for yield in alternative, income-generating assets. Very often, investors have to sacrifice liquidity in the search for yield. Opportunity amid the volatility While the deterioration in liquidity is a concern, as is the prospect of a “hard landing” for the Chinese economy, the volatile market environment is something investors should welcome, as it could present opportunities to add quality to their portfolios. Important Information Any security(s) mentioned above is for illustrative purpose only, not a recommendation to invest or divest. This document is intended to be for information purposes only and it is not intended as promotional material in any respect. The views and opinions contained herein are those of the author(s), and do not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. The material is not intended to provide, and should not be relied on for investment advice or recommendation. Opinions stated are matters of judgment, which may change. Information herein is believed to be reliable, but Schroder Investment Management (Hong Kong) Limited does not warrant its completeness or accuracy. Investment involves risks. Past performance and any forecasts are not necessarily a guide to future or likely performance. You should remember that the value of investments can go down as well as up and is not guaranteed. Exchange rate changes may cause the value of the overseas investments to rise or fall. For risks associated with investment in securities in emerging and less developed markets, please refer to the relevant offering document. The information contained in this document is provided for information purpose only and does not constitute any solicitation and offering of investment products. Potential investors should be aware that such investments involve market risk and should be regarded as long-term investments. Derivatives carry a high degree of risk and should only be considered by sophisticated investors. This material, including the website, has not been reviewed by the SFC. Issued by Schroder Investment Management (Hong Kong) Limited. Schroder Investment Management (Hong Kong) Limited Level 33, Two Pacific Place, 88 Queensway, Hong Kong Telephone +852 2521 1633 Fax +852 2530 9095