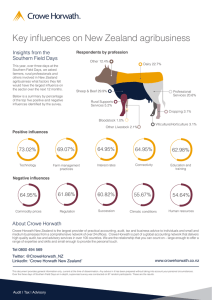

APS 210 - Quantitative requirements table

advertisement

APS 210 - Quantitative requirements table Element of risk MHL Regime Key matters to consider Minimum holdings For MLH, an ADI is required to maintain a portfolio of ‘specific liquid assets’ of 9% of its liabilities. APRA may require an ADI to hold a higher specified amount of liquid assets Total liabilities defined as total on-balance sheet liabilities plus irrevocable commitments Specified liquid assets Must be free from encumbrances, and includes: Notes and coins Some Government securities Bank bills, certificates of deposits and debt securities issued by ADIs Deposits (at call, and any other deposits readily convertible into cash within two business days) held with other ADIs, net of placements by other ADIs Any other securities approved by APRA For a deposit with another ADI to be deemed to be readily convertible to cash within two business days and qualify as an MLH asset, the ADI depositor needs to have unequivocal and documented contractual right to break that deposit at its sole discretion 1 Element of risk MHL Regime Key matters to consider Operational capacity For MLH, an ADI must ensure it has operational capacity to liquidate any securities held as liquid assets within two business days. APRA expects that an ADI will have appropriate operational access to more than one mode of access to the market, which may include the following means: Direct clean sale Repo to a third party Broker-intermediated clean sale or repo to a third party Repo with the RBA ADIs are expected to ensure that they have appropriate operational access to market liquidity, and periodically test this access Ensure that period testing does not ‘taint’ the investment portfolio of the ADI (likely to be classified as ‘held to maturity’) from a financial reporting perspective under the accounting standards (AASB 139 Financial Instruments: Recognition and Measurement) Liquid asset diversification For MLH, ADIs are expected to ensure that their liquid asset portfolios are appropriately diversified Diversification should be considered along product, issue and counterparty lines In considering an ADI’s liquid asset diversification, APRA would not expect to see holdings of lower-rate debt securities that are concentrated on either an individual name or aggregate basis ‘Going concern’ scenario An MLH ADI is also required to complete the ‘going concern’ scenario in APS 210 Going concern scenario requires an ADI to model the expected behaviour of cash flows in the ordinary course of business for a future period at least equal to 15 months 2 Support At Crowe Horwath we have the expertise and specialists who can support you in applying or understanding these revised liquidity standards. If you have any questions feel free to contact Brad Bohun, Anne Lockwood, David Munday or Pippa Hobson. Brad Bohun Partner - Audit and Assurance +61 2 6021 1111 brad.bohun@crowehorwath.com.au Anne Lockwood Partner - Audit and Assurance +61 3 9258 6802 anne.lockwood@crowehorwath.com.au David Munday Partner - Audit and Assurance +61 3 9258 9564 david.munday@crowehorwath.com.au Pippa Hobson Partner - Audit and Assurance +61 8 9488 1140 pippa.hobson@crowehorwath.com.au This document provides general information only, current at the time of production. Any advice in it has been prepared without taking into account your objectives, financial situation or needs. You should seek professional advice before acting on any material. Liability limited by a scheme approved under Professional Standards Legislation (other than for the acts or omissions of financial services licensees) in each State or Territory other than Tasmania. Crowe Horwath (Aust) Pty Ltd is a member of Crowe Horwath International, a Swiss verein. Each member firm of Crowe Horwath is a separate and independent legal entity. Crowe Horwath (Aust) Pty Ltd and its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath or any other member of Crowe Horwath and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath or any other Crowe Horwath member. Any general advice in this newsletter is provided by: Crowe Horwath (Aust) Pty Ltd ABN 84 006 466 351 and Australian Credit Licence No. 389054; Crowe Horwath Financial Advice Pty Ltd ABN 51 060 092 631 AFSL No. 238244; Crowe Horwath Corporate Finance (Aust) Ltd ABN 95 001 508 363 AFSL No. 239170; Crowe Horwath Insurance Brokers Pty Ltd ABN 17 139 730 528 AFSL No. 342526; Crowe Horwath Property Securities Ltd ABN 91 010 208 107 AFSL No. 247427. You should obtain and consider the Product Disclosure Statement for the financial products mentioned before making a decision to acquire the product. While all reasonable care is taken in the preparation of this newsletter, to the extent allowed by legislation Crowe Horwath accept no liability whatsoever for reliance on it. 3