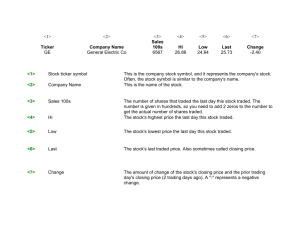

12 Equity Research Nabors Industries Ltd. [NYSE: NBR]

advertisement

Nabors Industries Ltd. May 25, 2012 Spring Equity Research Nabors Industries Ltd. As the world’s largest land drilling contractor, Nabors Industries Ltd. (Nabors or the Company) owns a fleet of approximately 500 land drilling rigs and 750 land workover and servicing wells. Their land operations are supplemented by their offshore rigs, which include 39 platform rigs, 12 jack ups and 4 barge drilling rigs in the United States and multiple international markets. In addition, Nabors also provides hydraulic fracturing, cementing, nitrogen and acid pressure pumping services. Nabors also manufactures top drives and drilling instrumentation systems and provides comprehensive transportation, engineering and facilities maintenance services around the world. Investment Thesis Despite facing a challenging natural gas market in North America, Nabors Industries continues to demonstrate incredibly strong revenue growth, which came in at 31% higher year over year for the first quarter 2012. Mr. Petrello, the Company’s new CEO, is also a potential catalyst for growth. His commitment to restructure the organization around their core strengths, drilling and production, confirms management’s renewed focus. In addition to strong fundamentals, trading nearly fifty percent below its 52-week average makes Nabors Industries a strong buy with a price target of $26.82. 12 Nabors Industries Ltd. [NYSE: NBR] Rating: BUY Price (as of May 25): $13.82 Price Target: $26.82 % Upside: 94% Sector: Energy Industry: Energy Equipment & Services Sub Industry: Oil & Gas Drilling Market Data 52-Week Range: 11.05 – 28.50 Market Cap. (B): 4.06 D. Shares Out. (M): 290.3 Avg. Daily Volume: 7,349,440 Beta: 2.32 Dividend Yield: 0% Financial Snapshot USD (mm) 2010 2011 2012E 2013E Revenue 4.29 6.35 6.88 7.82 EPS .30 .77 2.28 2.49 Consensus 2.20 2.55 Analyst: Julie M. Heigel Heigel.193@osu.edu (330) 388-7902 1 Nabors Industries Ltd. May 25, 2012 Table of Contents Company overview ............................................................................................................................. 3 BUSINESS SEGMENTS.........................................................................................................................3 BUSINESS STRATEGY AND VALUE DRIVERS.................................................................................5 Investment thesis ................................................................................................................................. 7 MACRO ENVIRONMENT ....................................................................................................................7 SECTOR ANALYSIS .............................................................................................................................9 FINANCIAL ANALYSIS ..................................................................................................................... 12 VALUATION ANALYSIS ................................................................................................................... 13 RISKS AND CONSIDERATIONS........................................................................................................... 14 conclusions .............................................................................................................................................15 APPENDIX A .................................................................................................................................................16 List of Figures: Figure 1: Actively Marketed Rigs by Region.................................................................................................3 Figure 2: 2011 Revenue by Segment.............................................................................................................4 Figure 3: 2011 Contract Drilling Composition..............................................................................................4 Figure 4: 2012 Q1 Revenue by Business Line ...............................................................................................5 Figure 5: 2012 Q1 Revenue by Segment .......................................................................................................5 Figure 6: Q1 Rig Years 2012 vs. 2011...........................................................................................................6 Figure 7: Growth Scenarios for Global Energy Demand ...............................................................................7 Figure 8: U.S. Crude Oil Inventory ..............................................................................................................8 Figure 9: World Oil Supply Capacity Growth ..............................................................................................8 Figure 10: Historical Crude Oil Front Month Future Prices ..........................................................................9 Figure 11: Natural Gas Spot Price (Henry Hub) ..........................................................................................9 Figure 12: Crude Oil Spot Price (Brent) .......................................................................................................9 Figure 13: Energy 1-year Performance Relative to S&P 500 ........................................................................ 10 Figure 14: Baker Hughes Rig Count vs. Oil & Gas Drilling......................................................................... 11 Figure 15: Key Financial Ratios for Nabors Industries Ltd. ........................................................................ 12 List of Tables: Table 1: Operating Segment Restructuring ...................................................................................................4 Table 2: Energy Sub-Industry Relative Performance ................................................................................... 11 Table 3: Nabors Industries Valuation – Relative to S&P 500 ....................................................................... 13 Table 4: Nabors Industries Valuation – Relative to Industry........................................................................ 13 Table 5: Nabors Industries Valuation – Absolute ....................................................................................... 14 APPENDIX A Exhibit A-1: DCF...................................................................................................................................... 17 Exhibit A-2: Implied Equity Sensitivity Analysis .......................................................................... 17 Exhibit A-3: Income Statement Forecasts ..................................................................................... 18 Exhibit A-4: Nabors Industries Balance Sheet............................................................................... 19 2 Nabors Industries Ltd. May 25, 2012 Company overview Nabors Industries began operations in 1987 under the current management team as a contract land drilling service provider on the North Slope of Alaska, Western Canada and in the Rocky Mountain region of the United States. The Company has since then expanded both their service offerings and also their geographical presence. Nabors actively markets a fleet of 500 land drilling rigs in the U.S. Lower 48 States, Alaska, Latin America, the Far East, Middle East, Commonwealth of Independent States and Africa. All 750 workover and well-servicing rigs are located in the US Lower 48 States and Canada. The Company’s offshore drilling operations is comprised of 39 platform rigs, 12 jack ups and 4 barge drilling rigs. Approximately 50% of these rigs are actively marketed in the US Gulf of Mexico, with the remainder primarily positioned in the Middle East.1 Figure 1: Actively Marketed Rigs by Region 900 Workover 750 Offshore 600 Onshore 450 300 150 0 United States Canada Middle East/Africa Latin America Far East Source: Nabors Industries Online – Investor Relations BUSINESS SEGMENTS Under the leadership of new CEO Anthony Petrello, Nabors is streamlining operations in the formation of two business division: Drilling and Rig Services, which will include all of the Company’s drilling and rigrelated operations; and Completion and Production Services, which will consist of well servicing and coil tubing rigs, and fluids management and pressure pumping services. The Company began reporting results based on these two divisions as of the first quarter of 2012. Prior to this restructuring, Nabors reported operating revenue by Contract Drilling, Pressure Pumping, Oil and Gas, and Other Operating Segments. Contract Drilling included all drilling, workover and well-serving operations, on land and offshore. The Pressure Pumping operations previously encompassed hydraulic fracturing and downhole surveying services, and Oil and Gas comprised the Company’s oil and gas exploration and production operations. Lastly, segments engaged in drilling technology and top drive manufacturing, directional drilling and rig instrumentation software were included under Other Operating Segments. 1 Nabors Industries Online – About Nabors http://www.nabors.com/Public/index.asp 3 Nabors Industries Ltd. May 25, 2012 The Company reported total revenue of $6.12 billion in 2011, an increase of an impressive 47% over 2010. As depicted below in Figure 2, Contract Drilling contributed almost 70% of total revenue or approximately $4.4 billion. Of this $4.4 billion, the Company’s US Lower 48 Land Drilling operations added $1.7 billion, with the second largest component of revenue derived from US Land Well-servicing operations2. Moving forward it is important for investors to note the drastic shift in how revenue by operating segment will be reported. Under the restructuring, these lines of business will be reported under either Drilling and Rig Services of Completion and Production Services as detailed below in Table 1. Figure 2: 2011 Revenue by Segment 1% Figure 3: 2011 Contract Drilling Composition Contract Drilling 11% Pressure Pumping 19% Oil and Gas 69% U.S. Land U.S. Well-servicing 25% 39% Alaska 13% Other 3% 16% 4% U.S. Offshore Canada International Source: Nabors 2011 10-K Table 1: Operating Segment Restructuring Drilling and Rig Services Completion and Production Services Land Drilling Fluids and Manufacturing and Disposal Understanding this restructuring is critical to understanding reported revenue moving forward. Workover and well-services which formerly comprised nearly 30% of Contract Drilling will now be Offshore Drilling Coiled Tubing reported under Completion and Rig Equipment Workover and well-services Production Services. Likewise, Specialty Rigs Fluid Storage drilling software technology will Directional Drilling Fluids and Materials now be reported under Drilling and Transportation Rig Services instead of Other Drilling Software Operating Segments. Investors Technology need to be cognizant of these changes when comparing trends moving forward. Nabors reported revenue for the first three months ended March 31, 2012 as compared to first three months ended March 31, 2011 under the newly structured segments as depicted in Figure 4 and Figure 5 below.3 2 3 Nabors Industries Ltd. 2011 Annual Report Nabors Industries Ltd. 2012 Q1 Report 4 Nabors Industries Ltd. May 25, 2012 Figure 4: 2012 Q1 Revenue by Business Line 600,000 500,000 400,000 300,000 200,000 100,000 0 (100,000) 2012 2011 Source: Nabors 2012 Q1 10-Q BUSINESS STRATEGY AND Value drivers Commitment to Technology Moving forward, Nabors Industries plans to rejuvenate their focus on technology-intensive services through their wholly-owned subsidiary, Carnig Drilling Technology, Ltd.. Carnig Drilling Technology has contributed several groundbreaking technologies, which includes ROCKIT and REVIT drilling systems. This state-of-the-art engineering allows Nabors’ customers to utilize a stateof-the-art directional steering control system which effectively orients the tool face when slide drilling.4 According to the Director of Corporate Development, Denny Smith, at the UBS Global Oil and Gas Conference on May 22, over 35% of services and rentals revenue in 2011 came from new products, technologies and services introduced the past three years such as ROCKIT and REVIT. In a competitive industry driven by cutthroat bidding for contracts, available innovative technology can provide a significant advantage. 4 Figure 5: 2012 Q1 Revenue by Segment Drilling and Rig Services Completion and Production Services Source: Nabors 2012 Q1 10-Q Nabors Industries Online – Carnig Drilling Technology, Ltd. 5 Nabors Industries Ltd. May 25, 2012 Young and Productive Rig Fleet By year-end 2012, Nabors will have built 152 new rigs and performed 28 major upgrades on existing rigs since 2005.5 These upgrades and new builds indicate that nearly one-third of Nabors fleet is either new or improved and therefore in a position to command higher day rates than their competitors. This is reflected in their rig year count as depicted in Figure 6 below. A rig year is a measure of the number of equivalent rigs operating during a given Figure 6: Q1 Rig Years period. It is calculated as the number of 2012 vs. 2011 days rigs that are operating divided by the 500.00 number of days in the period.6 If a rig is International 400.00 down for maintenance, it is not operating. However because Nabors has such a new 300.00 Canada fleet, this maintenance is not necessary. An 200.00 increase in the number of rig years of a fleet Alaska leads to the ability to command higher day 100.00 rates and also improve utilization of the rigs. U.S. Offshore 0.00 This youthful fleet will be a key asset for 2012 2011 Nabors in the North American market. Large oil and gas conglomerates have their choice of contractors in the over saturated North American markets and therefore having an effective and efficient rig fleet differentiates them from their competition. Extensive Existing Contracts A surplus in supply of natural gas has led to depressed gas prices and therefore a challenging environment for many oil firms operating in the United States. Nabors Industries however has weathered this storm better than its competitors thanks to its extensive backlog of pressure pumping contracts extending well into 2013.7 In addition to this backlog, Nabors also signed nine new long-term contracts for new-builds in the first quarter of 2012.8 Strategic Realignment After experiencing several quarters of declining revenue in the oil and gas exploration and production operations, Anthony Petrello has decided to liquidate their oil and gas positions and strategically realign with their core business segments, Contract Drilling and Completion and Production Services. Management is committed to selling as much as $800 million of oil and natural gas assets and business units this year. Several oil and gas sales have already been completed totaling approximately $150 million. Other assets totaling approximately $500 million are in the pipeline for execution later this year.9 In addition to streamlining operations, Petrello has committed to using these funds to restore financial flexibility by paying down existing debt balances. Highlighted at the UBS Global Oil and Gas Conference earlier this week, Nabors announced a targeted net debt to capitalization reduction from 42% 5 Denny Smith, UBS Global Oil and Gas Conference (Nabors Industries Publication) Nabors Industries Online – Glossary of Drilling Terms 7 Anthony Petrello, Q1 2012 Conference Call 8 Bret Jenson, Nabors Becomes Latest Oil Services Firm to Blow Through Estimates, (Seeking Alpha) 9 Denny Smith, UBS Global Oil and Gas Conference (Nabors Industries Publication) 6 6 Nabors Industries Ltd. May 25, 2012 to 25% by 2013. Improved financial flexibility will allow the Company to capitalize on better technologyintensive investment opportunities moving forward. International Opportunities Nabors has established a sizeable presence in the Middle East, which I believe to be a primary driver for future growth in their international portfolio. The international unit posted income of $21.1 million for the first quarter of 2012, which was higher than management’s expectations. This was due primary to the early startup of high-spec platform rig offshore India. Management anticipates several other similar projects to commence in the region within the coming months. Growing revenue and improved margins in the international markets, especially the Middle East, will have a positive effect in the near future for Nabors. Investment thesis Macroeconomic analysis The energy sector as a whole is heavily influenced by the supply and demand of oil and natural gas in the market. Figure 7: Growth Scenarios for Global Energy Demand Demand It is the general consensus that long-term energy consumption and demand is estimated to grow at a steady rate. Figure 7 depicts a 12% increase in global energy demand between 2015 and 2020. This growth in demand assumes pre-crisis GDP conditions, no new energy regulation and the assumption that electric vehicles make up 14% of all vehicles sold by 2020. Modifying the assumptions to account for a severe downturn, new EU regulations and the assumption that electric vehicles make up 50% of sales, demand is still strong at 11.7% growth between 2015 and 202010. Given the magnitude of the Euro crisis, a “doubledip” global economic crisis is still possible which would impact global demand. Regardless of economic conditions however, long-term demand will remain strong. It is worthy to note however that approximately 90% of this demand will come from non-OECD11, which are primarily undeveloped countries. This trend is also depicted in Figure 7. Above: Pre-Crisis Below: Severe Downturn Source: McKinsey Quarterly 10 McKinsey Quarterly, Exploring Global Energy Demand, June 2009 http://www.mckinseyquarterly.com/Exploring_global_energy_demand_2369 11 OECD – Organisation of Economic Co-operation and Development 7 Nabors Industries Ltd. Supply May 25, 2012 Figure 8: U.S. Crude Oil Inventory Global supply of oil and gas is determined by a variety of factors including market prices, upstream activity, rates of proven oilfield decline and an unlimited amount of geopolitical reasons. However a simple snapshot of world oil inventories and capacity lend a solid foundation for analyzing current and future oil supplies. Although inventory levels are not a good indicator of future supplies of oil, it does provide a good idea of how well current supply is meeting current demand. As you can see in Figure 8, inventory levels have dropped slightly which indicates that demand has been growing faster than supply so far in 2012. In addition to current inventory levels, it is also useful to analyze future capacity to determine whether or not there is opportunity for growth to meet the growing demands. The International Energy Agency has predicted global oil supply capacity to increase to 100.6 mb/d by 2016, a net increase averaging +1.1 mb/d annually12. The majority of non-OPEC supply growth is derived from Brazil, Canada, Kazakhstan and Columbia. Source: Thomson Reuters Baseline Figure 9: World Oil Supply Capacity Growth Oil and Gas Prices Natural gas and oil prices as discussed are primarily determined by supply and demand in the market. Until early 2000, the price of oil was relatively stable around $20 per barrel. Beginning around 2003, the market began to see a stable increase in oil prices followed by a drastic run up in 2008 just before the Source: International Energy Agency great recession. As seen in Figure 12 below, oil prices fell from $140 per barrel to about $40 per barrel in less than 6 months. Brent Crude is currently trading at $105 per barrel; however the U.S. benchmark crude – West Texas Intermediate is trading as low as $90 per barrel. Brent was a $26 premium over WTI 6 months ago and is now only a $15 premium. Following this trend, I believe this spread will narrow as both spot prices trade between $95-100 per barrel for the remainder of the year. That being said, although price of oil has begun to fall largely in response to decreased worries over tension in the Middle East, I expect it to remain volatile and increase in the long run. As with most contango markets, consumers drive the price of futures higher than the spot price in an attempt to hedge 12 International Energy Agency. (2011). Medium-Term Oil & Gas Markets 8 Nabors Industries Ltd. May 25, 2012 against the risk of higher spot prices13. This is the current case for WTI, however Brent has exhibited a state known as backwardation. As the spread between the two spots narrow, Brent will become less backwardated and WTI will flatten out. This relationship is show in Figure 10. As depicted in Figure 11, natural gas is trading at an all-time low, around $2.50 million British thermal units (Btu). This is a result of an unseasonably warm winter and the increased number of oil and gas companies partaking in fracking. In my opinion the natural gas spot price has seen its bottom and I expect an increase by December. Figure 10: Historical Crude Oil Front Month Future Prices Figure 11: Natural Gas Spot Price (Henry Hub) Source: International Energy Agency Figure 12: Crude Oil Spot Price (Brent) Source: Thomson Reuters Baseline 13 Layard-Liesching, Ronald. (2012). Investing in Commodities, Derivative and Alternative Investments. CFA Curriculum Level I 9 Nabors Industries Ltd. May 25, 2012 Sector analysis The Energy sector is the 6th largest sector of the S&P 500 with a market capitalization of approximately $1.3 trillion14 in market capitalization. Year–to-date it is the S&P 500’s worst performing sector with a return of -5.82%. Quarter-to-date it is the S&P 500’s second worst performing sector with a return of 8.04%. Financials is the Index’s worst performer. Energy is the second worst performing and second best performing sector for 3-year and 5-year performance respectively. A chart depicting the sector’s 1year price performance relative to the overall S&P can be seen in Figure 13 below. Figure 13: Energy 1-year Performance Relative to S&P 500 Source: Thomson Reuters Baseline Source: Thomson Reuters Baseline The Energy sector is divided into two industries, Energy Equipment & Services, and Oil, Gas & Consumable fuels. Energy Equipment & Services is further divided into two sub-industries; Oil & Gas Equipment Services which is composed mostly of large oilfield services firms, and Oil & Gas Drilling. Oil, Gas & Consumable Fuels is organized by five sub-industries; Coal and Consumable Fuels, Oil & Gas Exploration and Production, Oil & Gas Integrated, Oil & Gas Refining and Marketing, and Oil & Gas Storage. Over the past 10 years, the Energy sector has dominated every other sector in the S&P 500 by a significant amount. The Energy sector has demonstrated an absolute return of 124% for the past 10years where as the second best performing sector in the S&P 500, Information Technology, has returned less than half of that at 57%15. Much of this outperformance can be explained by the run-up in oil prices just before the great recession. It is therefore beneficial to look at an industry and subindustry breakdown of the sector. As you can see in Table 2 below, only one sub-industry has recorded positive gains year-to-date. Oil & Gas Drilling, in which Nabors participates, has recorded year-to-date losses of -8%. This makes it the third best performing sub-industry within the sector. However it is also the second worst performing sub-industry for 10-year performance with a return of 12%. This is because unlike Oil & 14 Standards and Poor Performance Data – Online http://www.standardandpoors.com/indices/sp500/en/us/?indexId=spusa-500-usduf--p-us-l-15 Thomson Reuters Basline 10 Nabors Industries Ltd. May 25, 2012 Gas Exploration and Production and Oil & Gas Equipment/Services, Oil & Gas Drilling was affected less by the run-up in oil prices in 2008. This is depicted in their standard deviation of .195, the second lowest behind Oil & Gas Storage. Table 2: Energy Sub-Industry Relative Performance Industry Sub-Industry Energy Equipment & Services Oil, Gas & Consumable Fuels Oil & Gas Equipment/Services Oil & Gas Drilling Coal & Consumable Fuels Oil & Gas Exploration & Production Oil & Gas Integrated Oil & Gas Refining & Marketing Oil & Gas Storage Baseline Symbol OGEQP YTD 1-Year 10-Year -11% -24% 117% Std. Dev. .779 OGDRL COCOF -8% -33% -27% -60% 12% 60% .195 .629 OGEXP -12% -21% 186% 1.17 OGINT OGREF -11% 7% -6% -6% 99% 56% .621 .327 OGSTO 0% 22% -4% .140 Source: Thomson Reuters Baseline Baker Hughes Rig Count Figure 14: Baker Hughes Rig Count vs. Oil & Gas Drilling Baker Hughes has issued rotary rig counts for North America since 1944 and global rig counts since 1975. The North American rig count is released every Friday at noon central time, and the global rig count is released on the fifth working day of each month. The rig count is an extremely important leading indicator of demand for products used in the oil and gas industry. For this reason, the Baker Hughes rig count exhibits a high correlation with the energy sector and more specific to Nabors, to the Oil & Gas Rig counts generally rise following increased spending on exploration and Source: Thomson Reuters Baseline development by large integrated oil firms. Integrated oil firms typically only increase their spending on exploration when prices of oil and natural gas are expected to rise. Therefore by extension, the rig count reflects stability in energy prices. As of May, the U.S. rig count was down 3 from April and up 136 rigs from last year. As of April, the international rig count was down 14 from March and up 49 rigs from April of 2011. 11 Nabors Industries Ltd. Financial analysis May 25, 2012 Figure 15: Key Financial Ratios for Nabors Industries Ltd. Discounted Cash Flow Model As seen in Exhibit A-1 of Appendix A, assuming a terminal discount rate of 11.50% and a terminal future cash flow growth rate of 2.00% for Nabors Industries forecasts a target price of $23.36. This offers a 69% upside from the trading price of $13.82 at the close of trading May 25th, 2012. This valuation is backed by strong revenue growth through 2014, recovering operating margins and management’s commitment to improve the Company’s solvency. Revenue growth Nabors Industries surpassed consensus revenue estimates by nearly $40 million for the first quarter 2012. This is an increase of 31% year over year. Gains in revenue represent solid performance in all segments of the North American market and although Source: Thomson Reuters Baseline lower, better than expected performance from international operations. Nabors has seen double-digit year-over-year growth in revenue for the past five quarters16. As seen in Figure 15, sales per share are at a 10-year high. The DCF included in this analysis assumes conservative revenue growth of 8.4%, 13.67% and 14.94% for the years 2012, 2013 and 2014 respectively. Equipped with an extensive backlog of contracts, Nabors is positioned well to weather the poor natural gas environment in 2012. Operating Margins Operating margin was 14.8% for the first quarter 2012, a 2.1% improvement from the first quarter 201117. As seen in Figure 15, this is close to the 10-year median of 15.5%. It is my belief that this operating margin will continue to improve as international margins expand. For this reason, I have included operating margins of roughly 21% for the next three years in my discounted cash flow analysis. Solvency In addition to strong revenue and improved operating margin, Nabors under the new leadership of Anthony Petrello is committed to deleveraging the balance sheet and improving the Company’s financial flexibility. Low levels of leverage allowed Nabors to capitalize on several valuable investment opportunities between 2000 and 2008. These opportunities became increasingly limited as the Company added more debt to their balance sheet. This increased leverage can be seen in the bottom panel of Figure 16 17 Wall Street Cheat Sheet, Nabors Industries Ltd. Earnings, April 24, 2012 The Motley Fool, Nabors Industries Crushes Earnings Estimates 12 Nabors Industries Ltd. May 25, 2012 15 above. Nabors target total debt by year-end 2012 was $4,900 million. This goal was already achieved after the first quarter with reported total debt of $4,773 million. Management has targeted long term total debt of $3,500 million by year-end 2013, a net debt reduction from 42% to 25%18 Valuation analysis Nabors Industries is undervalued and currently trading near its ten-year lows relative to the S&P 500, Industry, and historical absolute values. Although a portion of the discounted multiples can be attributed to increased uncertainty in geopolitical risk, the majority of the discount can be explained by the overreaction the market has had in response to the declining natural gas market in North America and European debt crisis. As discussed in the financial analysis segment, with the help of new CEO Anthony Petrello Nabors Industries has outperformed nearly all of analyst’s expectations. Even after confirming impressive revenue growth and even more impressive profits at the end of third quarter 2012, Nabors remains at a significant discount relative to several measures. For this reason, the discount to Nabors appears to be unwarranted. 18 Table 3: Nabors Industries Valuation – Relative to S&P 500 Relative to S&P500 High Low Median Current P/Trailing E 3.7 .28 1.1 0.59 P/Forward E 2.2 0.36 0.99 0.52 P/B 1.3 0.3 0.8 0.4 P/S 3.3 0.5 1.6 0.5 P/CF 2.1 0.2 0.8 0.3 Source: Thomson Reuters Baseline Table 4: Nabors Industries Valuation – Relative to Industry Relative to Industry High Low Median Current P/Trailing E 3.1 0.47 0.89 0.61 P/Forward E 2.3 0.58 0.89 0.66 P/B 2.2 0.4 0.8 0.7 P/S 1.2 0.3 0.7 0.4 P/CF 1.6 0.5 0.9 0.5 Source: Thomson Reuters Baseline Denny Smith, UBS Global Oil and Gas Conference (Nabors Industries Publication) 13 Nabors Industries Ltd. May 25, 2012 Table 5: Nabors Industries Valuation – Absolute Absolute Valuation High Low Median Current Target Multiple Target E, S, B /Share Target Price P/Forward E 37.6 4.8 14.9 6.3 12.4 2.28 28.18 P/S 4.9 0.5 2.1 0.6 1.7 23.6 40.11 P/B 3.7 0.6 2.4 0.8 1.95 17.72 34.55 P/EBITDA 15.98 1.81 7.41 2.11 6.0 4.35 26.15 P/CF 21.6 1.8 8.1 2.8 6.5 5.7 37.15 Source: Thomson Reuters Baseline Risks and considerations Sustained Decline in Oil and Natural Gas Prices The amount of spending on exploration and production is the largest driver of revenue for Nabors Industries. If there is a sustained decrease in oil and natural gas prices, there will also be a sustained decrease in spending by oil exploration and production companies, which would cut revenue drastically. Geopolitical Risk The challenge of managing geopolitical risk in the energy sector is always prevalent. As mentioned in the macroeconomic analysis, the bulk of growth in both demand and supply will come from non-OECD countries. The majority of these countries are considered developing markets and therefore cultural, infrastructure, security and new technology challenges must be confronted19. In addition to these challenges, some of these countries face a highly uncertain political environment. Nabors derives a significant portion of their business from global markets and needs to continue to be cognizant of these risks. Environmental Regulation Nabors Industries is subject to various federal, state and local laws regarding environmental regulations. The breadth of environmental regulation within the United States and globally has expanded recently and this trend is expected to continue. Most relevant, the United States has been reviewing at the request of the Occupational Safety and Health Administration and the Mine Safety and Health Administration the safety concerns related to hydraulic fracturing, or fracking. A push to bolster oversight on fracking could potentially be detrimentally to the Company’s pressure pumping operations. 19 pwc, Managing Geopolitical Risk - Online 14 Nabors Industries Ltd. May 25, 2012 Conclusion Nabors Industries is a Buy with a price target of $27. This price was derived as a function of implied equity from the discounted cash flow and also price targets indicated from the absolute valuation analysis. Specifically, the final price target is calculated as 65% of the implied equity value from the discounted cash flow model, and 7% of the implied equity value from each of the absolute valuation price targets calculated in Table 4. This significant upside is due primary to the noteworthy growth in both revenues and operating margins. This upside coupled with an overall undervalued position, makes Nabors Industries a strong buy. Implied Value DCF Implied Value* Valuation Implied Value* Current Price: $13.82 Expected Upside: 94% Discount Rate: 11.50% Terminal Growth: 2.5% $26.82 $23.36 $32.03 *DCF Implied value weighted 65% *P/Forward E, P/S, P/B, P/EBITDA, P/CF weighted 7% each Analyst Certification I, Julie Heigel, hereby certify that the views expressed in this research report accurately reflect my personal views about the subject companies and their underlying securities. 15 Nabors Industries Ltd. May 25, 2012 Appendix a 16 Nabors Industries Ltd. May 25, 2012 EXHIBIT A-1: DCF EXHIBIT a-2: Implied Equity sensitivity analysis 17 Nabors Industries Ltd. May 25, 2012 EXHIBIT a-3: Income statement forecasts 18 Nabors Industries Ltd. May 25, 2012 EXHIBIT a-4: Nabors Industries Balance sheet 19