Chapter 9 Cost Volume Profit

advertisement

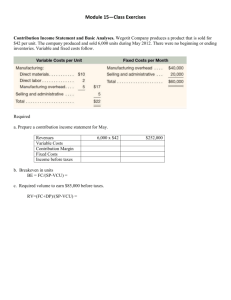

Chapter 9 Cost Volume Profit Variable definitions (notation) X – number of units USP – Unit Selling Price UVC – Unit Variable Cost UCM – Unit Contribution Margin FC – Fixed Cost TR – Total Revenue = USP * X TC – Total Costs VC – Total Variable Costs = UVC * X CMR – Contribution Margin Ratio (a.k.a. Contribution Margin Percentage) BEP – Break Even Point TOI – Target Operating Income TNI – Target Net Income t – tax rate Basic assumptions: 1) 2) 3) TC = FC + UVC * X TC and TR are linear in X Single product assumption Definitions CM CMR UCM Break-Even Point Target Net Income and taxes Miscellaneous other CVP issues Decision making Operating leverage Margin of safety Sales Mix Contribution Margin versus Gross Margin Appendix – CVP under uncertainty Example 1 ECAT manufactures printed circuit boards, which sell for $4 per board. They have variable costs of $2 for each board produced (including materials and variable overhead costs) and fixed costs of $100,000 per month. Currently they are selling 60,000 boards per month. a. b. c. d. e. What is ECAT’s break-even in units? What is their break-even in dollars? What is their current operating income (before taxes)? How many boards must they sell in order to earn $100,000 before taxes? How many boards must they sell in order to earn $90,000 after taxes? Suppose ECAT is selling 60,000 units and that the selling price is fixed at $4. What unit variable cost must they achieve in order to earn operating income of $35,000? Example 2 Suppose ECAT can spend $10,000 on advertising and increase sales by 10% (above the 60,000 level). a. Should ECAT purchase the advertising? b. What is the minimum increase in sales to make this investment worthwhile? Example 3 Suppose that ECAT can reduce the selling price by 10% and increase sales by 10,000 units. Should they reduce the selling price? Example 4 Suppose ECAT can choose from the following two operating cost structures: UVC1 = $1 FC1 = $100,000 UVC2 = $3 FC2 = $30,000 If the USP is $4, what is the optimal structure at various levels of activity and sales? Example 5 Suppose that ECAT makes two products PB1 and PB2. They have selling prices of $4 and $6 per board respectively and unit variable costs of $1 and $2 respectively. For every 10 units of PB1 that ECAT sells, they sell 6 units of PB2. How many units of PB1 and PB2 must ECAT sell in order to break-even? Example 6 Watco sells electric motors. The unit variable cost of each motor is $45. The unit selling price of each motor is $70. The fixed costs are $450,000. Watco is currently selling 20,000 electric motors. What is their break-even point in units? In dollar sales? FC 450,000 = = 18,000 UCM 25 = 18, 000 * 70 = $1, 260, 000 X BE = TRBE Should they buy advertising for $100,000 in order to increase sales by 10%? Increase in sales is 2,000 units. That has a CM of 2,000 * 25 = $50,000. Since this is less than the cost of $100,000, they should not buy the advertising. What is the minimum percentage increase in sales that would be required in order to make the advertising worthwhile? Increase in sales is D units (I just made up the D) which provides D*25 in contribution margin. That must at least cover $100,000, so D must be at least 4,000 units. 4,000 = 20% . 20,000 Suppose that Watco can buy a machine that costs $200,000 and decrease unit variable costs to $30. What is the minimum number of units that Watco must sell in order to make this investment worthwhile? Current profit is $50,000. New UCM = $40. New FC = $650,000. $40 * X − $650, 000 = $50, 000 $700, 000 X= = 17, 500 units $40 Suppose Watco can decrease selling price by 10% and increase unit sales by 20%, should they reduce their selling price? New USP = $63. New UCM = 18. New X is 24,000. 18*24,000 - $450,000 = ( $18,000 ) , so clearly they should not do so.